Advertisement

Ningxia Zhongke Biotechnology Co., Ltd (SHSE:600165) Shares Slammed 30% But Getting In Cheap Might Be Difficult Regardless

The Ningxia Zhongke Biotechnology Co., Ltd (SHSE:600165) share price has fared very poorly over the last month, falling by a substantial 30%. For any long-term shareholders, the last month ends a year to forget by locking in a 54% share price decline.

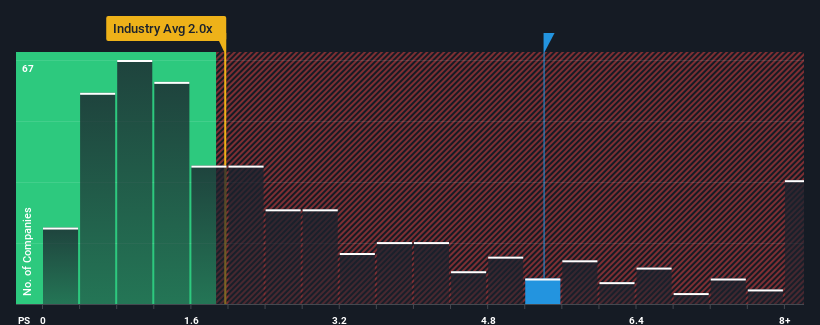

In spite of the heavy fall in price, you could still be forgiven for thinking Ningxia Zhongke Biotechnology is a stock to steer clear of with a price-to-sales ratios (or "P/S") of 5.4x, considering almost half the companies in China's Chemicals industry have P/S ratios below 2x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

See our latest analysis for Ningxia Zhongke Biotechnology

How Has Ningxia Zhongke Biotechnology Performed Recently?

As an illustration, revenue has deteriorated at Ningxia Zhongke Biotechnology over the last year, which is not ideal at all. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

Although there are no analyst estimates available for Ningxia Zhongke Biotechnology, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Ningxia Zhongke Biotechnology?

In order to justify its P/S ratio, Ningxia Zhongke Biotechnology would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 66%. Still, the latest three year period has seen an excellent 161% overall rise in revenue, in spite of its unsatisfying short-term performance. So we can start by confirming that the company has generally done a very good job of growing revenue over that time, even though it had some hiccups along the way.

When compared to the industry's one-year growth forecast of 21%, the most recent medium-term revenue trajectory is noticeably more alluring

With this in consideration, it's not hard to understand why Ningxia Zhongke Biotechnology's P/S is high relative to its industry peers. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What Does Ningxia Zhongke Biotechnology's P/S Mean For Investors?

Even after such a strong price drop, Ningxia Zhongke Biotechnology's P/S still exceeds the industry median significantly. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It's no surprise that Ningxia Zhongke Biotechnology can support its high P/S given the strong revenue growth its experienced over the last three-year is superior to the current industry outlook. Right now shareholders are comfortable with the P/S as they are quite confident revenue aren't under threat. Barring any significant changes to the company's ability to make money, the share price should continue to be propped up.

Having said that, be aware Ningxia Zhongke Biotechnology is showing 3 warning signs in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on Ningxia Zhongke Biotechnology, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Ningxia Zhongke Biotechnology might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600165

Ningxia Zhongke Biotechnology

Produces and sells coal-based activated carbon and lauric acid products.

Very low with worrying balance sheet.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor