Advertisement

- China

- /

- Metals and Mining

- /

- SHSE:600126

Does Hang Zhou Iron & SteelLtd (SHSE:600126) Have A Healthy Balance Sheet?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies Hang Zhou Iron & Steel Co.,Ltd. (SHSE:600126) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Hang Zhou Iron & SteelLtd

What Is Hang Zhou Iron & SteelLtd's Net Debt?

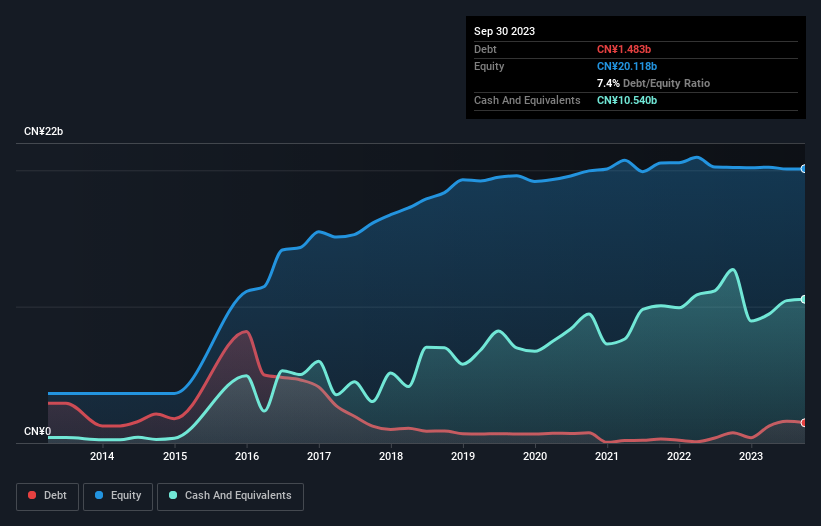

The image below, which you can click on for greater detail, shows that at September 2023 Hang Zhou Iron & SteelLtd had debt of CN¥1.48b, up from CN¥755.0m in one year. However, it does have CN¥10.5b in cash offsetting this, leading to net cash of CN¥9.06b.

How Healthy Is Hang Zhou Iron & SteelLtd's Balance Sheet?

According to the last reported balance sheet, Hang Zhou Iron & SteelLtd had liabilities of CN¥12.4b due within 12 months, and liabilities of CN¥380.4m due beyond 12 months. On the other hand, it had cash of CN¥10.5b and CN¥2.79b worth of receivables due within a year. So it can boast CN¥509.3m more liquid assets than total liabilities.

This surplus suggests that Hang Zhou Iron & SteelLtd has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Hang Zhou Iron & SteelLtd has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Hang Zhou Iron & SteelLtd will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Hang Zhou Iron & SteelLtd had a loss before interest and tax, and actually shrunk its revenue by 2.0%, to CN¥46b. We would much prefer see growth.

So How Risky Is Hang Zhou Iron & SteelLtd?

Although Hang Zhou Iron & SteelLtd had an earnings before interest and tax (EBIT) loss over the last twelve months, it made a statutory profit of CN¥69m. So taking that on face value, and considering the cash, we don't think its very risky in the near term. With mediocre revenue growth in the last year, we're don't find the investment opportunity particularly compelling. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 4 warning signs with Hang Zhou Iron & SteelLtd (at least 3 which are potentially serious) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Hang Zhou Iron & SteelLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600126

Hang Zhou Iron & SteelLtd

Primarily manufactures and sells steel products in China.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|17.7% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|11.0% undervalued

CH

Community Contributor