Investors bid Hubei Biocause Pharmaceutical (SZSE:000627) up CN¥1.2b despite increasing losses YoY, taking one-year return to 47%

Hubei Biocause Pharmaceutical Co., Ltd. (SZSE:000627) shareholders have seen the share price descend 20% over the month. But that doesn't change the reality that over twelve months the stock has done really well. Looking at the full year, the company has easily bested an index fund by gaining 47%.

The past week has proven to be lucrative for Hubei Biocause Pharmaceutical investors, so let's see if fundamentals drove the company's one-year performance.

View our latest analysis for Hubei Biocause Pharmaceutical

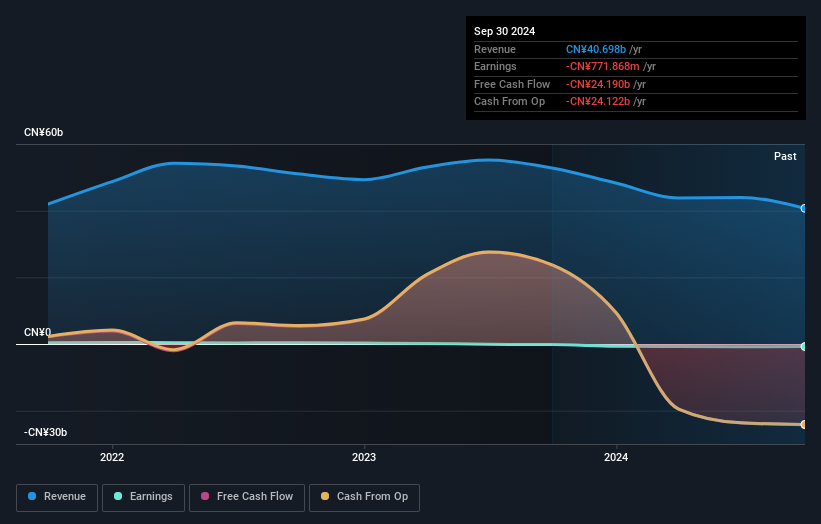

Given that Hubei Biocause Pharmaceutical didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. When a company doesn't make profits, we'd generally hope to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one would hope for good top-line growth to make up for the lack of earnings.

In the last year Hubei Biocause Pharmaceutical saw its revenue shrink by 23%. Despite the lack of revenue growth, the stock has returned a solid 47% the last twelve months. To us that means that there isn't a lot of correlation between the past revenue performance and the share price, but a closer look at analyst forecasts and the bottom line may well explain a lot.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

This free interactive report on Hubei Biocause Pharmaceutical's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

We're pleased to report that Hubei Biocause Pharmaceutical shareholders have received a total shareholder return of 47% over one year. That certainly beats the loss of about 7% per year over the last half decade. The long term loss makes us cautious, but the short term TSR gain certainly hints at a brighter future. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Take risks, for example - Hubei Biocause Pharmaceutical has 2 warning signs we think you should be aware of.

We will like Hubei Biocause Pharmaceutical better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Chinese exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hubei Biocause Pharmaceutical might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000627

Hubei Biocause Pharmaceutical

Primarily provides life and motor insurance products in China.

Slightly overvalued with imperfect balance sheet.

Market Insights

Community Narratives