Advertisement

- China

- /

- Healthcare Services

- /

- SZSE:301239

After Leaping 25% Chengdu Bright Eye Hospital Group Co., Ltd. (SZSE:301239) Shares Are Not Flying Under The Radar

Despite an already strong run, Chengdu Bright Eye Hospital Group Co., Ltd. (SZSE:301239) shares have been powering on, with a gain of 25% in the last thirty days. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 48% in the last twelve months.

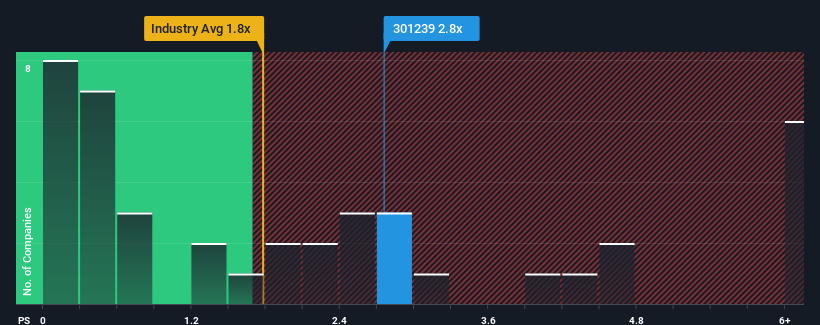

Since its price has surged higher, given close to half the companies operating in China's Healthcare industry have price-to-sales ratios (or "P/S") below 1.8x, you may consider Chengdu Bright Eye Hospital Group as a stock to potentially avoid with its 2.8x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for Chengdu Bright Eye Hospital Group

What Does Chengdu Bright Eye Hospital Group's P/S Mean For Shareholders?

With revenue growth that's superior to most other companies of late, Chengdu Bright Eye Hospital Group has been doing relatively well. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Chengdu Bright Eye Hospital Group.How Is Chengdu Bright Eye Hospital Group's Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as high as Chengdu Bright Eye Hospital Group's is when the company's growth is on track to outshine the industry.

Retrospectively, the last year delivered a decent 9.3% gain to the company's revenues. Pleasingly, revenue has also lifted 57% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 28% during the coming year according to the one analyst following the company. With the industry only predicted to deliver 14%, the company is positioned for a stronger revenue result.

In light of this, it's understandable that Chengdu Bright Eye Hospital Group's P/S sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Key Takeaway

Chengdu Bright Eye Hospital Group's P/S is on the rise since its shares have risen strongly. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Chengdu Bright Eye Hospital Group maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Healthcare industry, as expected. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Chengdu Bright Eye Hospital Group, and understanding them should be part of your investment process.

If you're unsure about the strength of Chengdu Bright Eye Hospital Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301239

Chengdu Bright Eye Hospital Group

A specialized chain medical institution company, engages in the provision of ophthalmic general medical services in China.

Reasonable growth potential with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor