Advertisement

- China

- /

- Medical Equipment

- /

- SZSE:300677

Intco Medical Technology (SZSE:300677) Seems To Use Debt Quite Sensibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Intco Medical Technology Co., Ltd. (SZSE:300677) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Intco Medical Technology

How Much Debt Does Intco Medical Technology Carry?

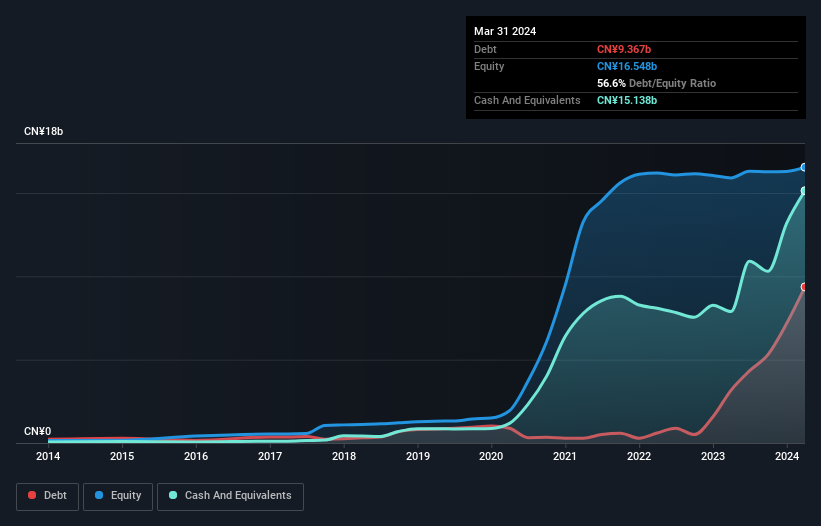

As you can see below, at the end of March 2024, Intco Medical Technology had CN¥9.37b of debt, up from CN¥3.16b a year ago. Click the image for more detail. But it also has CN¥15.1b in cash to offset that, meaning it has CN¥5.77b net cash.

A Look At Intco Medical Technology's Liabilities

According to the last reported balance sheet, Intco Medical Technology had liabilities of CN¥10.8b due within 12 months, and liabilities of CN¥2.12b due beyond 12 months. Offsetting these obligations, it had cash of CN¥15.1b as well as receivables valued at CN¥1.23b due within 12 months. So it actually has CN¥3.46b more liquid assets than total liabilities.

It's good to see that Intco Medical Technology has plenty of liquidity on its balance sheet, suggesting conservative management of liabilities. Given it has easily adequate short term liquidity, we don't think it will have any issues with its lenders. Simply put, the fact that Intco Medical Technology has more cash than debt is arguably a good indication that it can manage its debt safely.

It was also good to see that despite losing money on the EBIT line last year, Intco Medical Technology turned things around in the last 12 months, delivering and EBIT of CN¥109m. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Intco Medical Technology can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Intco Medical Technology has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. During the last year, Intco Medical Technology burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Intco Medical Technology has net cash of CN¥5.77b, as well as more liquid assets than liabilities. So we don't have any problem with Intco Medical Technology's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for Intco Medical Technology you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300677

Intco Medical Technology

Engages in the research and development, production, and marketing of medical consumables, health care equipment, and physiotherapy care products that are used in medical and elderly care institutions, household daily use, and other related industries in China and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|35.6% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|35.2% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|30.0% undervalued

EV

Community Contributor