- Singapore

- /

- Oil and Gas

- /

- SGX:RE4

Top Growth Companies With Insider Ownership January 2025

Reviewed by Simply Wall St

As global markets continue to navigate political developments and economic shifts, U.S. stocks have been buoyed by optimism around potential trade deals and advancements in artificial intelligence. With growth stocks outperforming their value counterparts for the first time this year, investors are increasingly focused on companies that not only show robust expansion but also have significant insider ownership, suggesting confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Lavvi Empreendimentos Imobiliários (BOVESPA:LAVV3) | 17.3% | 20.5% |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.5% | 38.9% |

| On Holding (NYSE:ONON) | 19.1% | 29.7% |

| Pharma Mar (BME:PHM) | 11.9% | 55.1% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

Below we spotlight a couple of our favorites from our exclusive screener.

Eastnine (OM:EAST)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Eastnine AB (publ) is a real estate investment firm with a market cap of SEK4.72 billion.

Operations: The firm's revenue segments include €3.65 million from properties in Latvia, €10.49 million from properties in Poland, and €23.94 million from properties in Lithuania.

Insider Ownership: 18%

Revenue Growth Forecast: 24% p.a.

Eastnine exhibits strong growth potential with forecasted earnings and revenue increases of 62.9% and 24% annually, respectively, outpacing the Swedish market. Insider confidence is evident as more shares have been bought than sold recently. However, debt coverage by operating cash flow remains a concern, and its return on equity is projected to be low at 5.7%. Recent strategic expansions include acquiring Warsaw Unit for EUR 280 million, enhancing property management profits by 18%.

- Navigate through the intricacies of Eastnine with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Eastnine shares in the market.

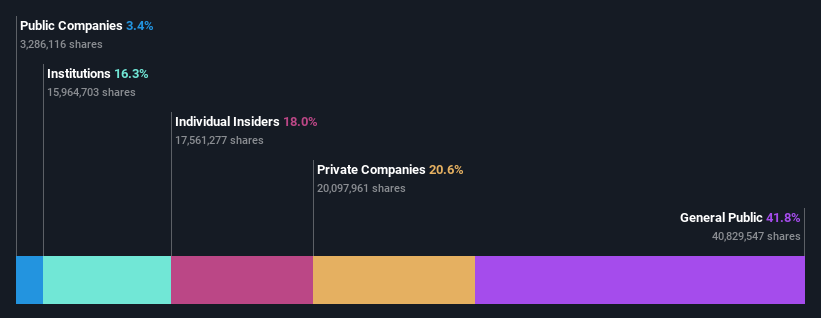

Geo Energy Resources (SGX:RE4)

Simply Wall St Growth Rating: ★★★★★★

Overview: Geo Energy Resources Limited is an investment holding company involved in the mining, production, and trading of coal with a market capitalization of SGD399.23 million.

Operations: Geo Energy Resources Limited generates revenue through its activities in coal mining, production, and trading.

Insider Ownership: 33.5%

Revenue Growth Forecast: 43.3% p.a.

Geo Energy Resources is poised for significant growth, with revenue and earnings expected to increase by 43.3% and 72% annually, respectively, surpassing market averages. The company trades at a substantial discount to its estimated fair value. Despite a dividend yield of 6.92%, it's not well covered by free cash flow. Recent developments include the construction of an Integrated Infrastructure in Indonesia, aiming to enhance logistical efficiency and diversify revenue streams toward becoming a billion-dollar energy group.

- Delve into the full analysis future growth report here for a deeper understanding of Geo Energy Resources.

- According our valuation report, there's an indication that Geo Energy Resources' share price might be on the cheaper side.

Guangzhou Wondfo BiotechLtd (SZSE:300482)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Guangzhou Wondfo Biotech Co., Ltd, with a market cap of CN¥10.65 billion, specializes in the research, development, production, and sale of point-of-care testing products and rapid diagnosis solutions for chronic disease management in China.

Operations: The company's revenue primarily comes from its diagnostic kits and equipment segment, which generated CN¥2.94 billion.

Insider Ownership: 31.1%

Revenue Growth Forecast: 21.1% p.a.

Guangzhou Wondfo Biotech shows promising growth prospects, with earnings and revenue expected to grow at 27.17% and 21.1% annually, outpacing the broader Chinese market. The stock trades at a favorable price-to-earnings ratio of 20.3x compared to the market average of 34.7x, indicating good relative value. However, its dividend yield of 1.8% is not well-supported by free cash flow, and Return on Equity is projected to be modest at 13.9%.

- Dive into the specifics of Guangzhou Wondfo BiotechLtd here with our thorough growth forecast report.

- Our expertly prepared valuation report Guangzhou Wondfo BiotechLtd implies its share price may be lower than expected.

Key Takeaways

- Discover the full array of 1477 Fast Growing Companies With High Insider Ownership right here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SGX:RE4

Geo Energy Resources

An investment holding company, engages in the mining, production, and trading of coal.

Exceptional growth potential and undervalued.

Similar Companies

Market Insights

Community Narratives