- China

- /

- Medical Equipment

- /

- SHSE:688329

Lacklustre Performance Is Driving Suzhou Iron Technology CO.,LTD's (SHSE:688329) 26% Price Drop

Suzhou Iron Technology CO.,LTD (SHSE:688329) shareholders won't be pleased to see that the share price has had a very rough month, dropping 26% and undoing the prior period's positive performance. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 46% share price drop.

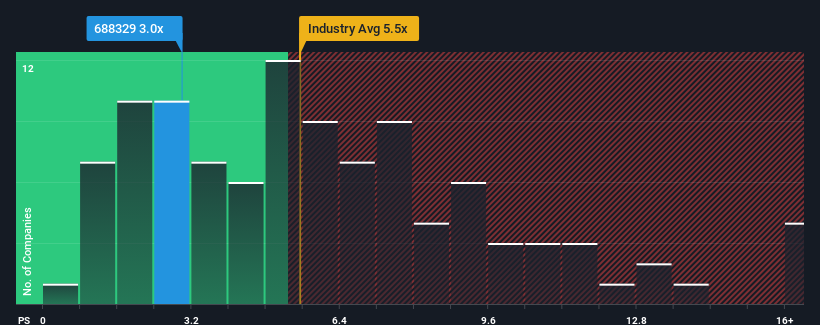

After such a large drop in price, Suzhou Iron TechnologyLTD may be sending bullish signals at the moment with its price-to-sales (or "P/S") ratio of 3x, since almost half of all companies in the Medical Equipment industry in China have P/S ratios greater than 5.5x and even P/S higher than 9x are not unusual. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

Check out our latest analysis for Suzhou Iron TechnologyLTD

What Does Suzhou Iron TechnologyLTD's Recent Performance Look Like?

As an illustration, revenue has deteriorated at Suzhou Iron TechnologyLTD over the last year, which is not ideal at all. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

Although there are no analyst estimates available for Suzhou Iron TechnologyLTD, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Any Revenue Growth Forecasted For Suzhou Iron TechnologyLTD?

There's an inherent assumption that a company should underperform the industry for P/S ratios like Suzhou Iron TechnologyLTD's to be considered reasonable.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 26%. The last three years don't look nice either as the company has shrunk revenue by 10% in aggregate. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

In contrast to the company, the rest of the industry is expected to grow by 25% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

With this in mind, we understand why Suzhou Iron TechnologyLTD's P/S is lower than most of its industry peers. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

What We Can Learn From Suzhou Iron TechnologyLTD's P/S?

Suzhou Iron TechnologyLTD's recently weak share price has pulled its P/S back below other Medical Equipment companies. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

It's no surprise that Suzhou Iron TechnologyLTD maintains its low P/S off the back of its sliding revenue over the medium-term. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Given the current circumstances, it seems unlikely that the share price will experience any significant movement in either direction in the near future if recent medium-term revenue trends persist.

It is also worth noting that we have found 2 warning signs for Suzhou Iron TechnologyLTD (1 is concerning!) that you need to take into consideration.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:688329

Suzhou Iron TechnologyLTD

Engages in the provision of intelligent medical material management solutions in China and internationally.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives