Advertisement

Revenue Miss: Zhengzhou Qianweiyangchu Food Co., Ltd. Fell 6.9% Short Of Analyst Revenue Estimates And Analysts Have Been Revising Their Models

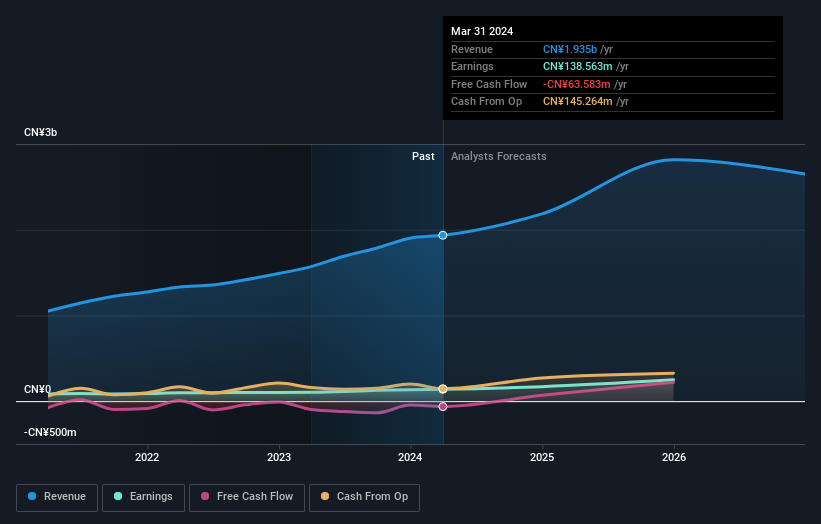

Zhengzhou Qianweiyangchu Food Co., Ltd. (SZSE:001215) last week reported its latest quarterly results, which makes it a good time for investors to dive in and see if the business is performing in line with expectations. Results look mixed - while revenue fell marginally short of analyst estimates at CN¥463m, statutory earnings were in line with expectations, at CN¥1.56 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Zhengzhou Qianweiyangchu Food after the latest results.

View our latest analysis for Zhengzhou Qianweiyangchu Food

Taking into account the latest results, the consensus forecast from Zhengzhou Qianweiyangchu Food's 13 analysts is for revenues of CN¥2.18b in 2024. This reflects a decent 13% improvement in revenue compared to the last 12 months. Per-share earnings are expected to soar 57% to CN¥2.19. In the lead-up to this report, the analysts had been modelling revenues of CN¥2.36b and earnings per share (EPS) of CN¥2.25 in 2024. It's pretty clear that pessimism has reared its head after the latest results, leading to a weaker revenue outlook and a small dip in earnings per share estimates.

The consensus price target fell 10% to CN¥61.07, with the weaker earnings outlook clearly leading valuation estimates. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Zhengzhou Qianweiyangchu Food, with the most bullish analyst valuing it at CN¥81.05 and the most bearish at CN¥42.00 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We can infer from the latest estimates that forecasts expect a continuation of Zhengzhou Qianweiyangchu Food'shistorical trends, as the 18% annualised revenue growth to the end of 2024 is roughly in line with the 20% annual growth over the past three years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 12% annually. So it's pretty clear that Zhengzhou Qianweiyangchu Food is forecast to grow substantially faster than its industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Zhengzhou Qianweiyangchu Food. Regrettably, they also downgraded their revenue estimates, but the latest forecasts still imply the business will grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Zhengzhou Qianweiyangchu Food's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Zhengzhou Qianweiyangchu Food. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple Zhengzhou Qianweiyangchu Food analysts - going out to 2026, and you can see them free on our platform here.

It is also worth noting that we have found 1 warning sign for Zhengzhou Qianweiyangchu Food that you need to take into consideration.

Valuation is complex, but we're here to simplify it.

Discover if Zhengzhou Qianweiyangchu Food might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:001215

Zhengzhou Qianweiyangchu Food

Primarily engages in the provision of customized and standardized prefabricated semi-finished products for catering companies, group meals, hotels, and banquets in China.

Flawless balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor