Take Care Before Diving Into The Deep End On Hunan New Wellful Co.,Ltd. (SHSE:600975)

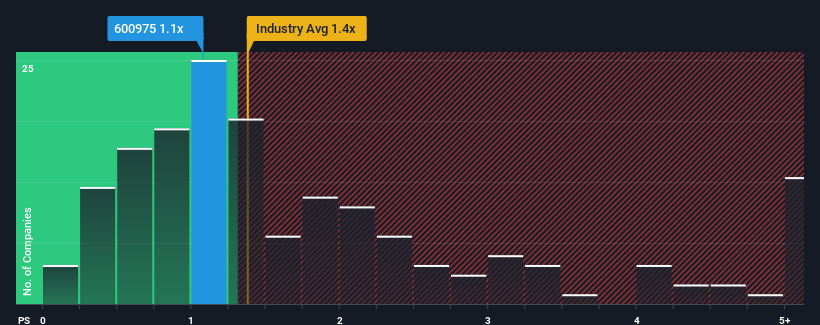

There wouldn't be many who think Hunan New Wellful Co.,Ltd.'s (SHSE:600975) price-to-sales (or "P/S") ratio of 1.1x is worth a mention when the median P/S for the Food industry in China is similar at about 1.4x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Hunan New WellfulLtd

What Does Hunan New WellfulLtd's Recent Performance Look Like?

With revenue growth that's superior to most other companies of late, Hunan New WellfulLtd has been doing relatively well. Perhaps the market is expecting this level of performance to taper off, keeping the P/S from soaring. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Hunan New WellfulLtd.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Hunan New WellfulLtd's to be considered reasonable.

Taking a look back first, we see that the company managed to grow revenues by a handy 5.4% last year. This was backed up an excellent period prior to see revenue up by 129% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenues over that time.

Turning to the outlook, the next year should generate growth of 63% as estimated by the five analysts watching the company. Meanwhile, the rest of the industry is forecast to only expand by 16%, which is noticeably less attractive.

In light of this, it's curious that Hunan New WellfulLtd's P/S sits in line with the majority of other companies. Apparently some shareholders are skeptical of the forecasts and have been accepting lower selling prices.

The Final Word

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Hunan New WellfulLtd currently trades on a lower than expected P/S since its forecasted revenue growth is higher than the wider industry. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future revenue could see some volatility.

A lot of potential risks can sit within a company's balance sheet. You can assess many of the main risks through our free balance sheet analysis for Hunan New WellfulLtd with six simple checks.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Hunan New WellfulLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600975

Hunan New WellfulLtd

Primarily engages in the breeding and supplying of pigs.

Undervalued with acceptable track record.

Market Insights

Community Narratives