- China

- /

- Capital Markets

- /

- SZSE:300059

East Money Information Co.,Ltd.'s (SZSE:300059) Share Price Could Signal Some Risk

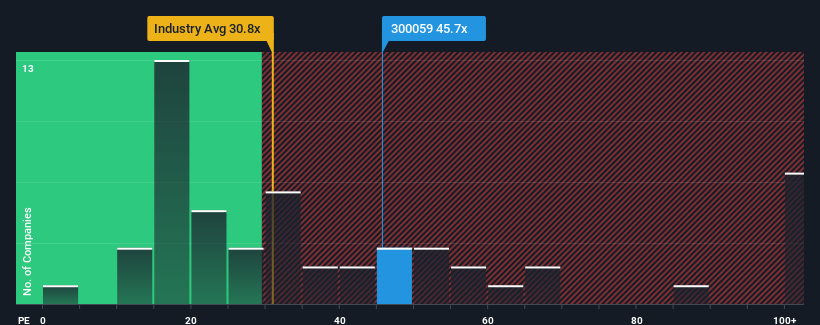

East Money Information Co.,Ltd.'s (SZSE:300059) price-to-earnings (or "P/E") ratio of 45.7x might make it look like a sell right now compared to the market in China, where around half of the companies have P/E ratios below 37x and even P/E's below 20x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

The recently shrinking earnings for East Money InformationLtd have been in line with the market. It might be that many expect the company's earnings to strengthen positively despite the tough market conditions, which has kept the P/E from falling. If not, then existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for East Money InformationLtd

Is There Enough Growth For East Money InformationLtd?

There's an inherent assumption that a company should outperform the market for P/E ratios like East Money InformationLtd's to be considered reasonable.

Retrospectively, the last year delivered virtually the same number to the company's bottom line as the year before. Likewise, not much has changed from three years ago as earnings have been stuck during that whole time. Therefore, it's fair to say that earnings growth has definitely eluded the company recently.

Shifting to the future, estimates from the analysts covering the company suggest earnings should grow by 18% over the next year. With the market predicted to deliver 37% growth , the company is positioned for a weaker earnings result.

In light of this, it's alarming that East Money InformationLtd's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of East Money InformationLtd's analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. When we see a weak earnings outlook with slower than market growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

A lot of potential risks can sit within a company's balance sheet. Take a look at our free balance sheet analysis for East Money InformationLtd with six simple checks on some of these key factors.

You might be able to find a better investment than East Money InformationLtd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if East Money InformationLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300059

East Money InformationLtd

Provides Internet-based financial information, data, and other services in China.

Adequate balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives