Advertisement

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that BTG Hotels (Group) Co., Ltd. (SHSE:600258) does use debt in its business. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for BTG Hotels (Group)

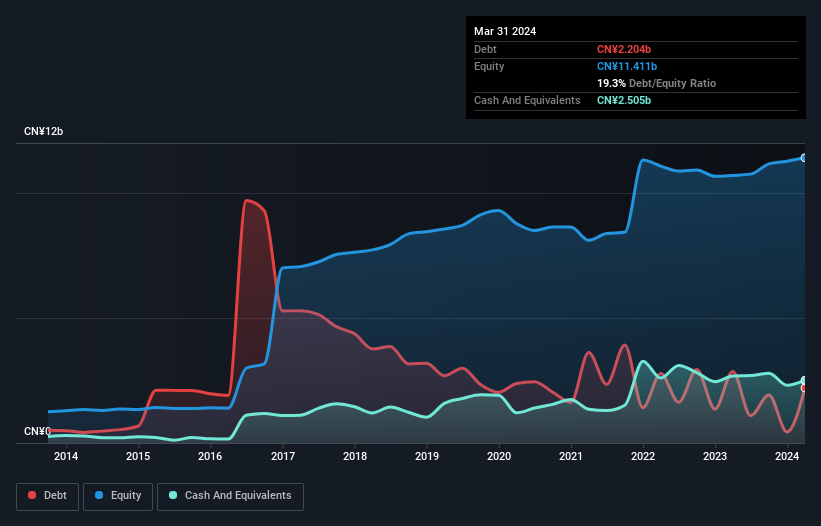

What Is BTG Hotels (Group)'s Net Debt?

The image below, which you can click on for greater detail, shows that BTG Hotels (Group) had debt of CN¥2.20b at the end of March 2024, a reduction from CN¥2.86b over a year. However, it does have CN¥2.51b in cash offsetting this, leading to net cash of CN¥301.0m.

A Look At BTG Hotels (Group)'s Liabilities

We can see from the most recent balance sheet that BTG Hotels (Group) had liabilities of CN¥4.65b falling due within a year, and liabilities of CN¥9.61b due beyond that. Offsetting these obligations, it had cash of CN¥2.51b as well as receivables valued at CN¥591.1m due within 12 months. So it has liabilities totalling CN¥11.2b more than its cash and near-term receivables, combined.

This deficit is considerable relative to its market capitalization of CN¥13.6b, so it does suggest shareholders should keep an eye on BTG Hotels (Group)'s use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution. While it does have liabilities worth noting, BTG Hotels (Group) also has more cash than debt, so we're pretty confident it can manage its debt safely.

Notably, BTG Hotels (Group)'s EBIT launched higher than Elon Musk, gaining a whopping 856% on last year. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if BTG Hotels (Group) can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. While BTG Hotels (Group) has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Happily for any shareholders, BTG Hotels (Group) actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing Up

Although BTG Hotels (Group)'s balance sheet isn't particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of CN¥301.0m. The cherry on top was that in converted 302% of that EBIT to free cash flow, bringing in CN¥3.1b. So we are not troubled with BTG Hotels (Group)'s debt use. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. We've identified 1 warning sign with BTG Hotels (Group) , and understanding them should be part of your investment process.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if BTG Hotels (Group) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600258

BTG Hotels (Group)

Engages in the operation and management of hotels in the People’s Republic of China.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor