- China

- /

- Food and Staples Retail

- /

- SZSE:301078

Kidswant Children Products Co.,Ltd. (SZSE:301078) Looks Just Right With A 30% Price Jump

Kidswant Children Products Co.,Ltd. (SZSE:301078) shares have continued their recent momentum with a 30% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 61% in the last year.

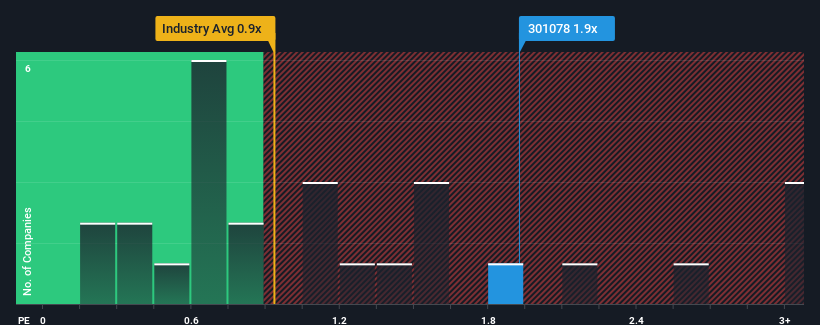

Following the firm bounce in price, when almost half of the companies in China's Consumer Retailing industry have price-to-sales ratios (or "P/S") below 0.9x, you may consider Kidswant Children ProductsLtd as a stock probably not worth researching with its 1.9x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Kidswant Children ProductsLtd

What Does Kidswant Children ProductsLtd's P/S Mean For Shareholders?

Kidswant Children ProductsLtd certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Kidswant Children ProductsLtd will help you uncover what's on the horizon.How Is Kidswant Children ProductsLtd's Revenue Growth Trending?

Kidswant Children ProductsLtd's P/S ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 8.5% last year. However, due to its less than impressive performance prior to this period, revenue growth is practically non-existent over the last three years overall. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next year should generate growth of 14% as estimated by the six analysts watching the company. That's shaping up to be materially higher than the 12% growth forecast for the broader industry.

With this in mind, it's not hard to understand why Kidswant Children ProductsLtd's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On Kidswant Children ProductsLtd's P/S

The large bounce in Kidswant Children ProductsLtd's shares has lifted the company's P/S handsomely. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into Kidswant Children ProductsLtd shows that its P/S ratio remains high on the merit of its strong future revenues. At this stage investors feel the potential for a deterioration in revenues is quite remote, justifying the elevated P/S ratio. Unless these conditions change, they will continue to provide strong support to the share price.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Kidswant Children ProductsLtd (1 can't be ignored!) that you should be aware of before investing here.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if Kidswant Children ProductsLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301078

Kidswant Children ProductsLtd

Engages in the retail of maternal, infant, and child products in China.

Excellent balance sheet with moderate growth potential.