Advertisement

- China

- /

- Consumer Durables

- /

- SZSE:301113

More Unpleasant Surprises Could Be In Store For Zhejiang Yayi Metal Technology Co.,Ltd's (SZSE:301113) Shares After Tumbling 26%

Unfortunately for some shareholders, the Zhejiang Yayi Metal Technology Co.,Ltd (SZSE:301113) share price has dived 26% in the last thirty days, prolonging recent pain. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 28% share price drop.

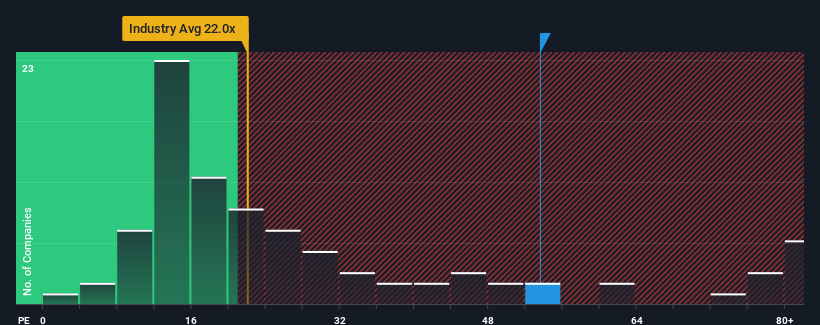

Although its price has dipped substantially, Zhejiang Yayi Metal TechnologyLtd's price-to-earnings (or "P/E") ratio of 53.6x might still make it look like a strong sell right now compared to the market in China, where around half of the companies have P/E ratios below 30x and even P/E's below 18x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For instance, Zhejiang Yayi Metal TechnologyLtd's receding earnings in recent times would have to be some food for thought. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

Check out our latest analysis for Zhejiang Yayi Metal TechnologyLtd

Does Growth Match The High P/E?

Zhejiang Yayi Metal TechnologyLtd's P/E ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 60%. This means it has also seen a slide in earnings over the longer-term as EPS is down 70% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

In contrast to the company, the rest of the market is expected to grow by 41% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

In light of this, it's alarming that Zhejiang Yayi Metal TechnologyLtd's P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Final Word

A significant share price dive has done very little to deflate Zhejiang Yayi Metal TechnologyLtd's very lofty P/E. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Zhejiang Yayi Metal TechnologyLtd currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these prices as being reasonable.

Plus, you should also learn about these 3 warning signs we've spotted with Zhejiang Yayi Metal TechnologyLtd (including 2 which can't be ignored).

Of course, you might find a fantastic investment by looking at a few good candidates. So take a peek at this free list of companies with a strong growth track record, trading on a low P/E.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Yayi Metal TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:301113

Zhejiang Yayi Metal TechnologyLtd

ZheJiang Yayi Metal Technology Co.,Ltd engages in the research and development, production, processing, and sale of outdoor braziers and gas stoves in the United States, Canada, and internationally.

Flawless balance sheet slight.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|4.3% undervalued

RO

Community Contributor