- China

- /

- Professional Services

- /

- SZSE:300989

LAY-OUT Planning Consultants Co. Ltd.'s (SZSE:300989) Shares Climb 54% But Its Business Is Yet to Catch Up

LAY-OUT Planning Consultants Co. Ltd. (SZSE:300989) shares have had a really impressive month, gaining 54% after a shaky period beforehand. The last 30 days bring the annual gain to a very sharp 43%.

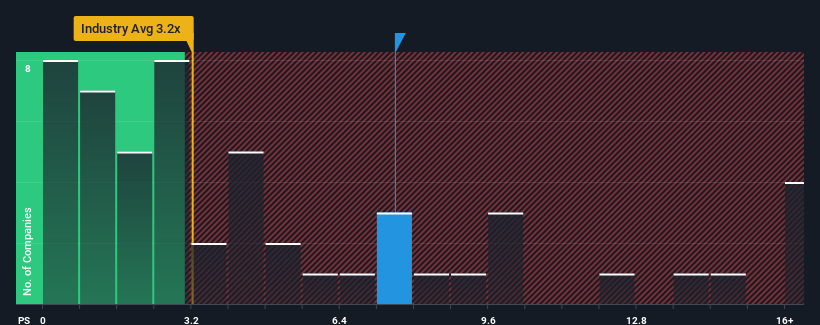

After such a large jump in price, given around half the companies in China's Professional Services industry have price-to-sales ratios (or "P/S") below 3.2x, you may consider LAY-OUT Planning Consultants as a stock to avoid entirely with its 7.6x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

Check out our latest analysis for LAY-OUT Planning Consultants

How LAY-OUT Planning Consultants Has Been Performing

For instance, LAY-OUT Planning Consultants' receding revenue in recent times would have to be some food for thought. One possibility is that the P/S is high because investors think the company will still do enough to outperform the broader industry in the near future. If not, then existing shareholders may be quite nervous about the viability of the share price.

Although there are no analyst estimates available for LAY-OUT Planning Consultants, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Do Revenue Forecasts Match The High P/S Ratio?

In order to justify its P/S ratio, LAY-OUT Planning Consultants would need to produce outstanding growth that's well in excess of the industry.

Retrospectively, the last year delivered a frustrating 4.4% decrease to the company's top line. That put a dampener on the good run it was having over the longer-term as its three-year revenue growth is still a noteworthy 13% in total. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been mostly respectable for the company.

Comparing that to the industry, which is predicted to deliver 89% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this in mind, we find it worrying that LAY-OUT Planning Consultants' P/S exceeds that of its industry peers. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Bottom Line On LAY-OUT Planning Consultants' P/S

Shares in LAY-OUT Planning Consultants have seen a strong upwards swing lately, which has really helped boost its P/S figure. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

The fact that LAY-OUT Planning Consultants currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

Before you take the next step, you should know about the 4 warning signs for LAY-OUT Planning Consultants (2 can't be ignored!) that we have uncovered.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300989

LAY-OUT Planning Consultants

Operates as a planning and engineering business in China, Pakistan, and Nigeria.

Flawless balance sheet minimal.

Market Insights

Community Narratives