- China

- /

- Commercial Services

- /

- SZSE:002599

Investors Don't See Light At End Of Beijing Shengtong Printing Co., Ltd's (SZSE:002599) Tunnel And Push Stock Down 32%

Beijing Shengtong Printing Co., Ltd (SZSE:002599) shares have had a horrible month, losing 32% after a relatively good period beforehand. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 17% share price drop.

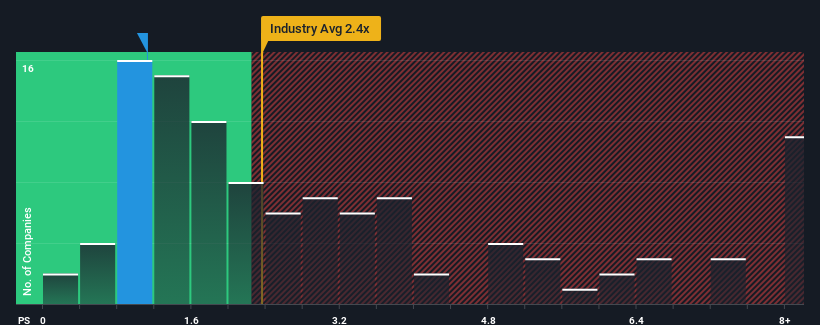

Following the heavy fall in price, Beijing Shengtong Printing's price-to-sales (or "P/S") ratio of 1.1x might make it look like a buy right now compared to the Commercial Services industry in China, where around half of the companies have P/S ratios above 2.4x and even P/S above 5x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Beijing Shengtong Printing

What Does Beijing Shengtong Printing's P/S Mean For Shareholders?

Beijing Shengtong Printing could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

Want the full picture on analyst estimates for the company? Then our free report on Beijing Shengtong Printing will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The Low P/S?

The only time you'd be truly comfortable seeing a P/S as low as Beijing Shengtong Printing's is when the company's growth is on track to lag the industry.

Retrospectively, the last year delivered a decent 3.5% gain to the company's revenues. Revenue has also lifted 17% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has actually done a good job of growing revenue over that time.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue should grow by 17% over the next year. With the industry predicted to deliver 27% growth, the company is positioned for a weaker revenue result.

In light of this, it's understandable that Beijing Shengtong Printing's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Beijing Shengtong Printing's P/S has taken a dip along with its share price. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

As we suspected, our examination of Beijing Shengtong Printing's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

You should always think about risks. Case in point, we've spotted 1 warning sign for Beijing Shengtong Printing you should be aware of.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Shengtong Printing might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002599

Beijing Shengtong Printing

Provides printing services for publication industries in China.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives