- China

- /

- Commercial Services

- /

- SZSE:002229

Hongbo Co.,Ltd.'s (SZSE:002229) 29% Dip Still Leaving Some Shareholders Feeling Restless Over Its P/SRatio

Hongbo Co.,Ltd. (SZSE:002229) shares have had a horrible month, losing 29% after a relatively good period beforehand. The last month has meant the stock is now only up 5.5% during the last year.

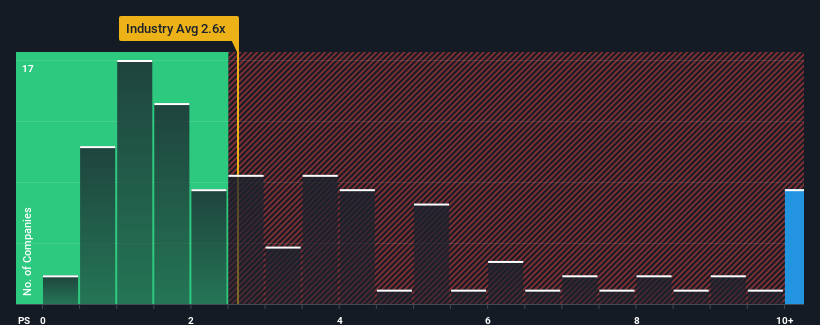

Even after such a large drop in price, given around half the companies in China's Commercial Services industry have price-to-sales ratios (or "P/S") below 2.6x, you may still consider HongboLtd as a stock to avoid entirely with its 14.6x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

See our latest analysis for HongboLtd

What Does HongboLtd's Recent Performance Look Like?

Revenue has risen firmly for HongboLtd recently, which is pleasing to see. Perhaps the market is expecting this decent revenue performance to beat out the industry over the near term, which has kept the P/S propped up. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on HongboLtd will help you shine a light on its historical performance.What Are Revenue Growth Metrics Telling Us About The High P/S?

HongboLtd's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered a decent 11% gain to the company's revenues. The latest three year period has also seen a 13% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Comparing that to the industry, which is predicted to deliver 31% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this information, we find it concerning that HongboLtd is trading at a P/S higher than the industry. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What We Can Learn From HongboLtd's P/S?

A significant share price dive has done very little to deflate HongboLtd's very lofty P/S. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our examination of HongboLtd revealed its poor three-year revenue trends aren't detracting from the P/S as much as we though, given they look worse than current industry expectations. Right now we aren't comfortable with the high P/S as this revenue performance isn't likely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with HongboLtd (at least 1 which doesn't sit too well with us), and understanding them should be part of your investment process.

If you're unsure about the strength of HongboLtd's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if HongboLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002229

HongboLtd

Engages in the security printing business in China and internationally.

Excellent balance sheet very low.

Market Insights

Community Narratives