Advertisement

- Italy

- /

- Aerospace & Defense

- /

- BIT:AVIO

Three Undiscovered Gems to Enhance Your Portfolio

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate a landscape of cooling inflation and robust bank earnings, major indices like the S&P MidCap 400 and Russell 2000 have shown notable gains, reflecting a positive sentiment towards smaller-cap stocks. In this environment, identifying promising but lesser-known companies can be an effective strategy for investors looking to diversify their portfolios and capitalize on emerging opportunities.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| Resource Alam Indonesia | 2.66% | 30.36% | 43.87% | ★★★★★★ |

| Macnica Galaxy | 52.99% | 8.23% | 18.45% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Voltamp Energy SAOG | 35.98% | -1.56% | 50.16% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tait Marketing & Distribution | 0.75% | 7.36% | 18.40% | ★★★★★★ |

| Sundart Holdings | 0.92% | -2.32% | -3.94% | ★★★★★★ |

| Eclatorq Technology | 37.47% | 8.43% | 18.41% | ★★★★★☆ |

| Billion Industrial Holdings | 3.63% | 18.00% | -11.38% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

Avio (BIT:AVIO)

Simply Wall St Value Rating: ★★★★☆☆

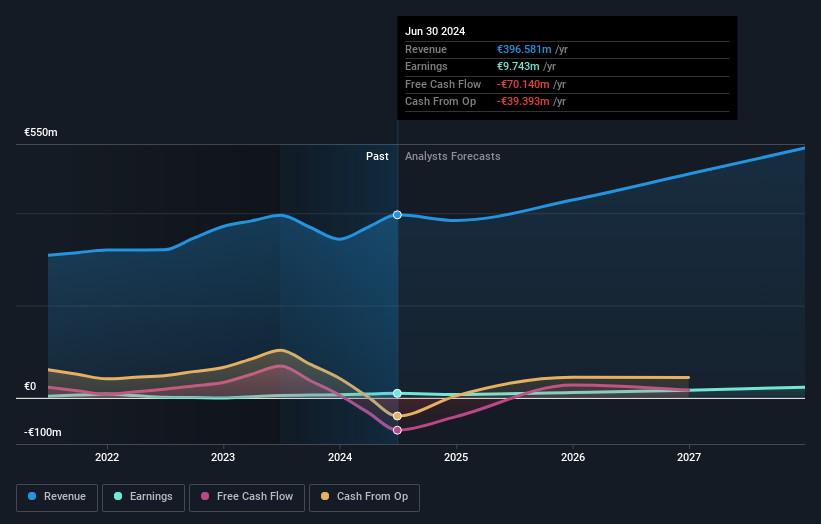

Overview: Avio S.p.A. is an Italian company that, through its subsidiaries, specializes in designing, developing, producing, and integrating space launchers both domestically and internationally with a market capitalization of approximately €392.67 million.

Operations: Avio generates revenue primarily from its Space Business segment, amounting to €396.58 million.

Avio, a player in the Aerospace & Defense sector, has shown impressive growth with earnings surging 82.5% over the past year, far outpacing its industry peers at 22.5%. The company's financial health appears robust as it holds more cash than total debt and has successfully lowered its debt to equity ratio from 23.3% to a mere 2.6% over five years. Despite not being free cash flow positive recently, Avio's profitability ensures that cash runway isn't an immediate concern. Looking ahead, earnings are projected to grow annually by 27%, suggesting continued momentum for this dynamic entity.

- Delve into the full analysis health report here for a deeper understanding of Avio.

Explore historical data to track Avio's performance over time in our Past section.

Science Environmental Protection (SHSE:688480)

Simply Wall St Value Rating: ★★★★★☆

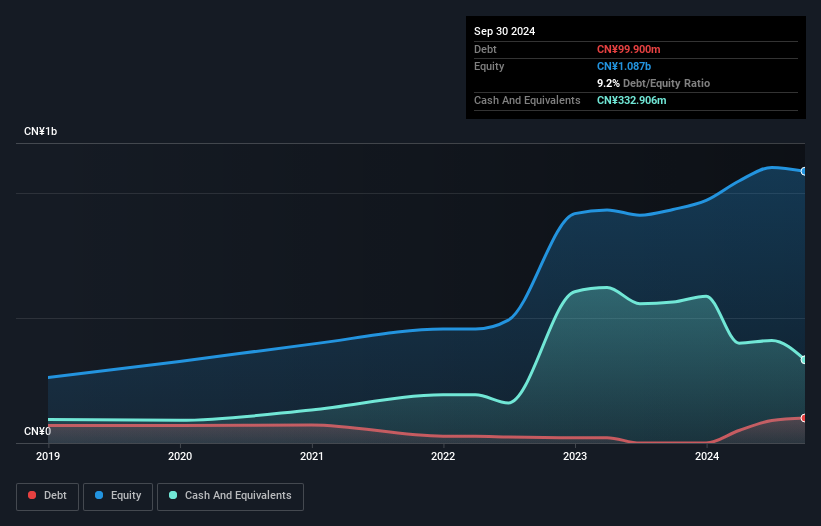

Overview: Science Environmental Protection Co., Ltd. operates in the environmental protection industry and has a market cap of approximately CN¥2.68 billion.

Operations: The company generates revenue primarily through its environmental protection services, with a focus on cost-effective operations. It has reported a net profit margin of 12.5%, indicating efficient management of expenses relative to its income.

Science Environmental Protection, a smaller entity within its sector, has shown impressive financial momentum. Over the past year, earnings surged by 152.8%, outpacing the Commercial Services industry's modest 1.7% growth rate. This performance is underscored by a net income of CNY 143 million for the first nine months of 2024, up from CNY 54 million in the prior year. The company's price-to-earnings ratio stands attractively at 15x against the broader CN market's average of 34.9x, indicating potential undervaluation relative to peers and industry standards. Additionally, its debt-to-equity ratio improved significantly over five years from 22.6% to just 9.2%.

- Navigate through the intricacies of Science Environmental Protection with our comprehensive health report here.

Understand Science Environmental Protection's track record by examining our Past report.

KH Neochem (TSE:4189)

Simply Wall St Value Rating: ★★★★★★

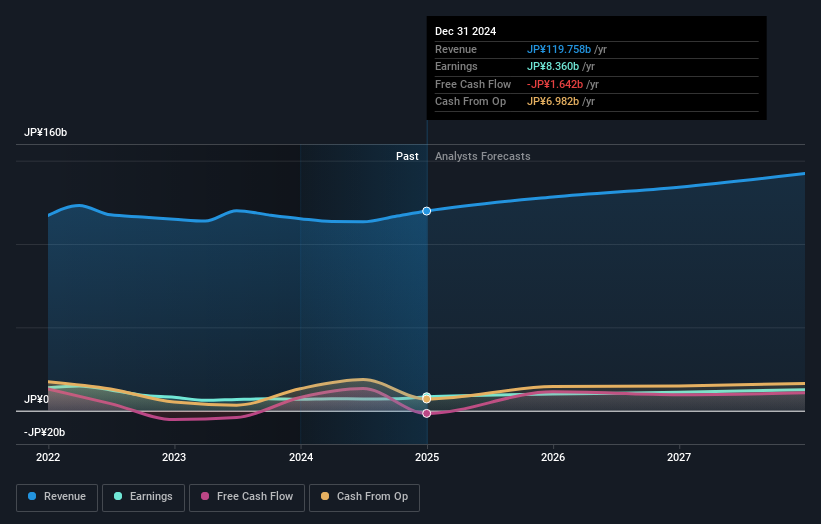

Overview: KH Neochem Co., Ltd. is engaged in the research, manufacturing, and sales of petrochemical products both in Japan and internationally, with a market cap of ¥76.73 billion.

Operations: KH Neochem generates revenue primarily from its Chemical Business segment, which reported ¥116.52 billion. The company's financial performance is highlighted by a focus on this core segment, contributing significantly to its overall market presence.

KH Neochem stands out in the chemicals sector with its high-quality earnings and satisfactory net debt to equity ratio of 17.3%. Over five years, the company's debt to equity ratio has improved significantly from 46.9% to 23.4%, reflecting prudent financial management. Although recent earnings growth faced a setback at -0.6%, it remains well-positioned for future expansion with forecasts suggesting a 14% annual increase in earnings. Trading at nearly 67% below estimated fair value, KH Neochem offers intriguing investment potential, further bolstered by a recent ¥5 billion bond issuance aimed at strengthening its financial position and supporting strategic initiatives through fixed-income offerings.

- Take a closer look at KH Neochem's potential here in our health report.

Evaluate KH Neochem's historical performance by accessing our past performance report.

Taking Advantage

- Take a closer look at our Undiscovered Gems With Strong Fundamentals list of 4663 companies by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:AVIO

Avio

Through its subsidiaries, designs, develops, produces, and integrates space launchers in Italy and internationally.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.9% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.1% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|36.0% overvalued

DA

Community Contributor