Advertisement

- China

- /

- Commercial Services

- /

- SHSE:605069

Beijing ZEHO Waterfront Ecological Environment Treatment Co., Ltd.'s (SHSE:605069) Popularity With Investors Is Under Threat From Overpricing

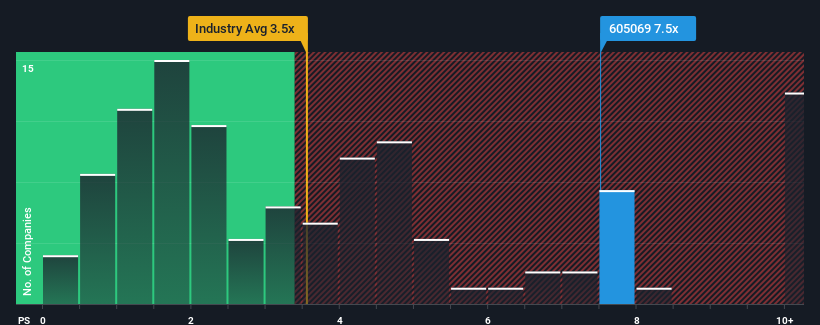

When close to half the companies in the Commercial Services industry in China have price-to-sales ratios (or "P/S") below 3.5x, you may consider Beijing ZEHO Waterfront Ecological Environment Treatment Co., Ltd. (SHSE:605069) as a stock to avoid entirely with its 7.5x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Beijing ZEHO Waterfront Ecological Environment Treatment

How Beijing ZEHO Waterfront Ecological Environment Treatment Has Been Performing

Recent times have been quite advantageous for Beijing ZEHO Waterfront Ecological Environment Treatment as its revenue has been rising very briskly. Perhaps the market is expecting future revenue performance to outperform the wider market, which has seemingly got people interested in the stock. If not, then existing shareholders might be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Beijing ZEHO Waterfront Ecological Environment Treatment will help you shine a light on its historical performance.Do Revenue Forecasts Match The High P/S Ratio?

Beijing ZEHO Waterfront Ecological Environment Treatment's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Taking a look back first, we see that the company grew revenue by an impressive 77% last year. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 79% overall. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

In contrast to the company, the rest of the industry is expected to grow by 33% over the next year, which really puts the company's recent medium-term revenue decline into perspective.

In light of this, it's alarming that Beijing ZEHO Waterfront Ecological Environment Treatment's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Bottom Line On Beijing ZEHO Waterfront Ecological Environment Treatment's P/S

While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Our examination of Beijing ZEHO Waterfront Ecological Environment Treatment revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. If recent medium-term revenue trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for Beijing ZEHO Waterfront Ecological Environment Treatment (1 shouldn't be ignored) you should be aware of.

If you're unsure about the strength of Beijing ZEHO Waterfront Ecological Environment Treatment's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Beijing ZEHO Waterfront Ecological Environment Treatment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:605069

Beijing ZEHO Waterfront Ecological Environment Treatment

Beijing ZEHO Waterfront Ecological Environment Treatment Co., Ltd.

Mediocre balance sheet very low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor