There Are Reasons To Feel Uneasy About Luoyang Xinqianglian Slewing Bearing's (SZSE:300850) Returns On Capital

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at Luoyang Xinqianglian Slewing Bearing (SZSE:300850), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Luoyang Xinqianglian Slewing Bearing is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

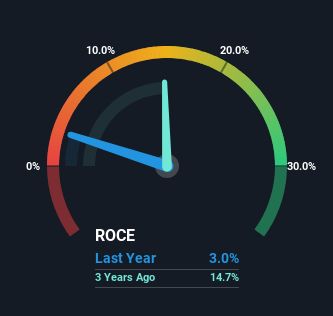

0.03 = CN¥228m ÷ (CN¥9.8b - CN¥2.1b) (Based on the trailing twelve months to September 2024).

Thus, Luoyang Xinqianglian Slewing Bearing has an ROCE of 3.0%. Ultimately, that's a low return and it under-performs the Machinery industry average of 5.2%.

View our latest analysis for Luoyang Xinqianglian Slewing Bearing

In the above chart we have measured Luoyang Xinqianglian Slewing Bearing's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free analyst report for Luoyang Xinqianglian Slewing Bearing .

So How Is Luoyang Xinqianglian Slewing Bearing's ROCE Trending?

We weren't thrilled with the trend because Luoyang Xinqianglian Slewing Bearing's ROCE has reduced by 84% over the last five years, while the business employed 1,101% more capital. Usually this isn't ideal, but given Luoyang Xinqianglian Slewing Bearing conducted a capital raising before their most recent earnings announcement, that would've likely contributed, at least partially, to the increased capital employed figure. It's unlikely that all of the funds raised have been put to work yet, so as a consequence Luoyang Xinqianglian Slewing Bearing might not have received a full period of earnings contribution from it.

On a side note, Luoyang Xinqianglian Slewing Bearing has done well to pay down its current liabilities to 22% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

The Key Takeaway

To conclude, we've found that Luoyang Xinqianglian Slewing Bearing is reinvesting in the business, but returns have been falling. It seems that investors have little hope of these trends getting any better and that may have partly contributed to the stock collapsing 81% in the last three years. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

If you'd like to know about the risks facing Luoyang Xinqianglian Slewing Bearing, we've discovered 1 warning sign that you should be aware of.

While Luoyang Xinqianglian Slewing Bearing isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300850

Luoyang Xinqianglian Slewing Bearing

Luoyang Xinqianglian Slewing Bearing Co., Ltd.

Reasonable growth potential with adequate balance sheet.

Market Insights

Community Narratives