Advertisement

- China

- /

- Electrical

- /

- SZSE:300833

Be Wary Of Guangzhou Haoyang ElectronicLtd (SZSE:300833) And Its Returns On Capital

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. In light of that, when we looked at Guangzhou Haoyang ElectronicLtd (SZSE:300833) and its ROCE trend, we weren't exactly thrilled.

Return On Capital Employed (ROCE): What Is It?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. To calculate this metric for Guangzhou Haoyang ElectronicLtd, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

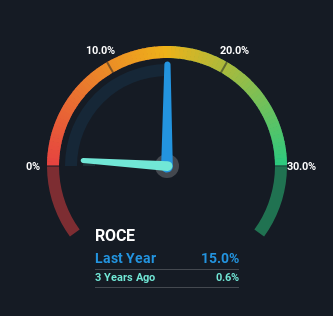

0.15 = CN¥373m ÷ (CN¥2.7b - CN¥223m) (Based on the trailing twelve months to March 2024).

Therefore, Guangzhou Haoyang ElectronicLtd has an ROCE of 15%. In absolute terms, that's a satisfactory return, but compared to the Electrical industry average of 6.0% it's much better.

See our latest analysis for Guangzhou Haoyang ElectronicLtd

Above you can see how the current ROCE for Guangzhou Haoyang ElectronicLtd compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Guangzhou Haoyang ElectronicLtd for free.

What Does the ROCE Trend For Guangzhou Haoyang ElectronicLtd Tell Us?

On the surface, the trend of ROCE at Guangzhou Haoyang ElectronicLtd doesn't inspire confidence. To be more specific, ROCE has fallen from 30% over the last five years. However it looks like Guangzhou Haoyang ElectronicLtd might be reinvesting for long term growth because while capital employed has increased, the company's sales haven't changed much in the last 12 months. It's worth keeping an eye on the company's earnings from here on to see if these investments do end up contributing to the bottom line.

On a side note, Guangzhou Haoyang ElectronicLtd has done well to pay down its current liabilities to 8.3% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

The Key Takeaway

To conclude, we've found that Guangzhou Haoyang ElectronicLtd is reinvesting in the business, but returns have been falling. Since the stock has gained an impressive 63% over the last three years, investors must think there's better things to come. However, unless these underlying trends turn more positive, we wouldn't get our hopes up too high.

If you'd like to know more about Guangzhou Haoyang ElectronicLtd, we've spotted 2 warning signs, and 1 of them can't be ignored.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300833

Guangzhou Haoyang ElectronicLtd

Engages in the research and development, production engineering, manufacture, sale, and service of professional stage, TV, concert, theatre and architectural lighting products worldwide.

Excellent balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|28.9% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|46.3% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor