- China

- /

- Electrical

- /

- SZSE:300709

Jiangsu Gian Technology Co., Ltd.'s (SZSE:300709) P/S Is Still On The Mark Following 47% Share Price Bounce

Jiangsu Gian Technology Co., Ltd. (SZSE:300709) shares have continued their recent momentum with a 47% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 97% in the last year.

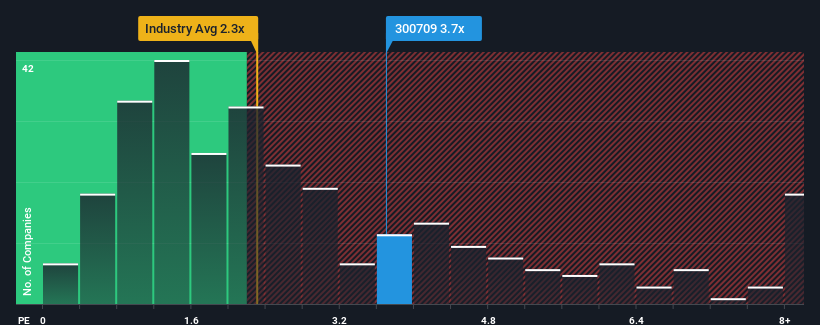

After such a large jump in price, when almost half of the companies in China's Electrical industry have price-to-sales ratios (or "P/S") below 2.3x, you may consider Jiangsu Gian Technology as a stock probably not worth researching with its 3.7x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's as high as it is.

Check out our latest analysis for Jiangsu Gian Technology

How Has Jiangsu Gian Technology Performed Recently?

Jiangsu Gian Technology certainly has been doing a good job lately as it's been growing revenue more than most other companies. It seems that many are expecting the strong revenue performance to persist, which has raised the P/S. If not, then existing shareholders might be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Jiangsu Gian Technology.How Is Jiangsu Gian Technology's Revenue Growth Trending?

In order to justify its P/S ratio, Jiangsu Gian Technology would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 5.5% last year. The solid recent performance means it was also able to grow revenue by 25% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Shifting to the future, estimates from the three analysts covering the company suggest revenue should grow by 32% over the next year. That's shaping up to be materially higher than the 23% growth forecast for the broader industry.

With this in mind, it's not hard to understand why Jiangsu Gian Technology's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Key Takeaway

Jiangsu Gian Technology's P/S is on the rise since its shares have risen strongly. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Jiangsu Gian Technology maintains its high P/S on the strength of its forecasted revenue growth being higher than the the rest of the Electrical industry, as expected. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

You always need to take note of risks, for example - Jiangsu Gian Technology has 1 warning sign we think you should be aware of.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade Jiangsu Gian Technology, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300709

Jiangsu Gian Technology

Manufactures and sells metal injection molding products in China and internationally.

High growth potential with excellent balance sheet.

Market Insights

Community Narratives