Advertisement

Jianglong Shipbuilding Co., Ltd.'s (SZSE:300589) P/S Is Still On The Mark Following 26% Share Price Bounce

Jianglong Shipbuilding Co., Ltd. (SZSE:300589) shareholders are no doubt pleased to see that the share price has bounced 26% in the last month, although it is still struggling to make up recently lost ground. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 19% over that time.

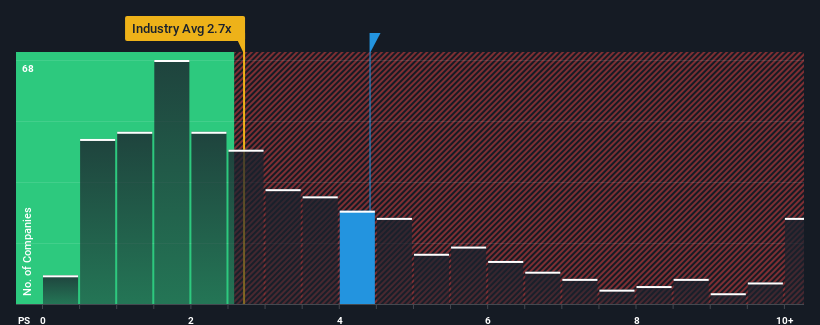

Following the firm bounce in price, you could be forgiven for thinking Jianglong Shipbuilding is a stock not worth researching with a price-to-sales ratios (or "P/S") of 4.4x, considering almost half the companies in China's Machinery industry have P/S ratios below 2.7x. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Jianglong Shipbuilding

How Jianglong Shipbuilding Has Been Performing

Jianglong Shipbuilding certainly has been doing a good job lately as it's been growing revenue more than most other companies. The P/S is probably high because investors think this strong revenue performance will continue. If not, then existing shareholders might be a little nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Jianglong Shipbuilding.How Is Jianglong Shipbuilding's Revenue Growth Trending?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Jianglong Shipbuilding's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 36% last year. The strong recent performance means it was also able to grow revenue by 83% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Shifting to the future, estimates from the sole analyst covering the company suggest revenue should grow by 62% over the next year. Meanwhile, the rest of the industry is forecast to only expand by 27%, which is noticeably less attractive.

With this in mind, it's not hard to understand why Jianglong Shipbuilding's P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Final Word

The large bounce in Jianglong Shipbuilding's shares has lifted the company's P/S handsomely. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our look into Jianglong Shipbuilding shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Jianglong Shipbuilding you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300589

Jianglong Shipbuilding

Engages in the design and construction of customized commercial and defense vessels in China and internationally.

Adequate balance sheet with moderate growth potential.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor