Advertisement

Lacklustre Performance Is Driving Guangzhou Goaland Energy Conservation Tech. Co., Ltd.'s (SZSE:300499) 31% Price Drop

The Guangzhou Goaland Energy Conservation Tech. Co., Ltd. (SZSE:300499) share price has fared very poorly over the last month, falling by a substantial 31%. Instead of being rewarded, shareholders who have already held through the last twelve months are now sitting on a 45% share price drop.

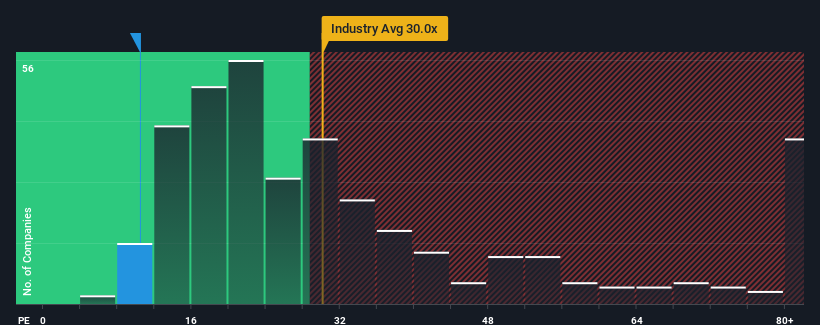

Although its price has dipped substantially, Guangzhou Goaland Energy Conservation Tech may still be sending very bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 10.5x, since almost half of all companies in China have P/E ratios greater than 30x and even P/E's higher than 54x are not unusual. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

Recent times have been advantageous for Guangzhou Goaland Energy Conservation Tech as its earnings have been rising faster than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Guangzhou Goaland Energy Conservation Tech

Is There Any Growth For Guangzhou Goaland Energy Conservation Tech?

Guangzhou Goaland Energy Conservation Tech's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Retrospectively, the last year delivered an exceptional 373% gain to the company's bottom line. The strong recent performance means it was also able to grow EPS by 319% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to slump, contracting by 42% during the coming year according to the only analyst following the company. Meanwhile, the broader market is forecast to expand by 36%, which paints a poor picture.

With this information, we are not surprised that Guangzhou Goaland Energy Conservation Tech is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

The Final Word

Shares in Guangzhou Goaland Energy Conservation Tech have plummeted and its P/E is now low enough to touch the ground. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Guangzhou Goaland Energy Conservation Tech's analyst forecasts revealed that its outlook for shrinking earnings is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about these 4 warning signs we've spotted with Guangzhou Goaland Energy Conservation Tech (including 2 which are a bit concerning).

If these risks are making you reconsider your opinion on Guangzhou Goaland Energy Conservation Tech, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300499

Guangzhou Goaland Energy Conservation Tech

Guangzhou Goaland Energy Conservation Tech.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor