Advertisement

Be Wary Of Nanjing Baose (SZSE:300402) And Its Returns On Capital

Finding a business that has the potential to grow substantially is not easy, but it is possible if we look at a few key financial metrics. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. Although, when we looked at Nanjing Baose (SZSE:300402), it didn't seem to tick all of these boxes.

Return On Capital Employed (ROCE): What Is It?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on Nanjing Baose is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.041 = CN¥65m ÷ (CN¥2.6b - CN¥998m) (Based on the trailing twelve months to March 2024).

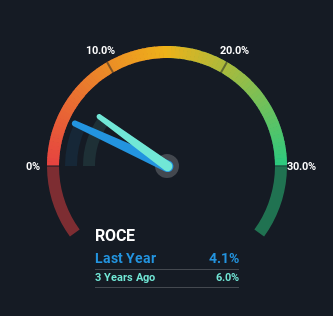

Therefore, Nanjing Baose has an ROCE of 4.1%. In absolute terms, that's a low return and it also under-performs the Machinery industry average of 5.6%.

See our latest analysis for Nanjing Baose

Historical performance is a great place to start when researching a stock so above you can see the gauge for Nanjing Baose's ROCE against it's prior returns. If you'd like to look at how Nanjing Baose has performed in the past in other metrics, you can view this free graph of Nanjing Baose's past earnings, revenue and cash flow.

How Are Returns Trending?

The trend of ROCE doesn't look fantastic because it's fallen from 6.5% five years ago, while the business's capital employed increased by 143%. However, some of the increase in capital employed could be attributed to the recent capital raising that's been completed prior to their latest reporting period, so keep that in mind when looking at the ROCE decrease. The funds raised likely haven't been put to work yet so it's worth watching what happens in the future with Nanjing Baose's earnings and if they change as a result from the capital raise.

On a side note, Nanjing Baose has done well to pay down its current liabilities to 39% of total assets. So we could link some of this to the decrease in ROCE. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Some would claim this reduces the business' efficiency at generating ROCE since it is now funding more of the operations with its own money.

Our Take On Nanjing Baose's ROCE

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for Nanjing Baose. Furthermore the stock has climbed 62% over the last five years, it would appear that investors are upbeat about the future. So while investors seem to be recognizing these promising trends, we would look further into this stock to make sure the other metrics justify the positive view.

If you want to continue researching Nanjing Baose, you might be interested to know about the 2 warning signs that our analysis has discovered.

While Nanjing Baose may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

Valuation is complex, but we're here to simplify it.

Discover if Nanjing Baose might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300402

Nanjing Baose

Engages in the research and development, design, manufacture, and installation of special material pressure vessels and pipe fittings of titanium, zirconium, nickel, tantalum, copper, and stainless steel primarily in China.

Flawless balance sheet with proven track record.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor