Some Confidence Is Lacking In SanFeng Intelligent Equipment Group Co., Ltd.'s (SZSE:300276) P/S

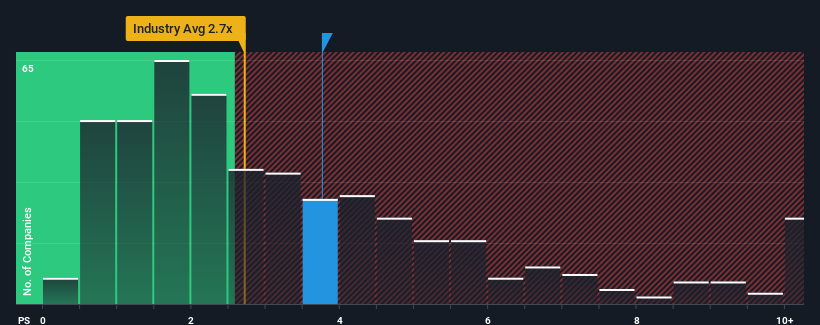

SanFeng Intelligent Equipment Group Co., Ltd.'s (SZSE:300276) price-to-sales (or "P/S") ratio of 3.8x may not look like an appealing investment opportunity when you consider close to half the companies in the Machinery industry in China have P/S ratios below 2.7x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for SanFeng Intelligent Equipment Group

What Does SanFeng Intelligent Equipment Group's P/S Mean For Shareholders?

The revenue growth achieved at SanFeng Intelligent Equipment Group over the last year would be more than acceptable for most companies. It might be that many expect the respectable revenue performance to beat most other companies over the coming period, which has increased investors’ willingness to pay up for the stock. However, if this isn't the case, investors might get caught out paying too much for the stock.

Although there are no analyst estimates available for SanFeng Intelligent Equipment Group, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For SanFeng Intelligent Equipment Group?

The only time you'd be truly comfortable seeing a P/S as high as SanFeng Intelligent Equipment Group's is when the company's growth is on track to outshine the industry.

Taking a look back first, we see that the company managed to grow revenues by a handy 13% last year. Ultimately though, it couldn't turn around the poor performance of the prior period, with revenue shrinking 3.9% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Comparing that to the industry, which is predicted to deliver 28% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's alarming that SanFeng Intelligent Equipment Group's P/S sits above the majority of other companies. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the recent negative growth rates.

The Bottom Line On SanFeng Intelligent Equipment Group's P/S

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of SanFeng Intelligent Equipment Group revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. When we see revenue heading backwards and underperforming the industry forecasts, we feel the possibility of the share price declining is very real, bringing the P/S back into the realm of reasonability. Should recent medium-term revenue trends persist, it would pose a significant risk to existing shareholders' investments and prospective investors will have a hard time accepting the current value of the stock.

It is also worth noting that we have found 1 warning sign for SanFeng Intelligent Equipment Group that you need to take into consideration.

If these risks are making you reconsider your opinion on SanFeng Intelligent Equipment Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300276

SanFeng Intelligent Equipment Group

SanFeng Intelligent Equipment Group Co., Ltd.

Adequate balance sheet with acceptable track record.

Market Insights

Community Narratives