SanFeng Intelligent Equipment Group Co., Ltd.'s (SZSE:300276) Business Is Trailing The Industry But Its Shares Aren't

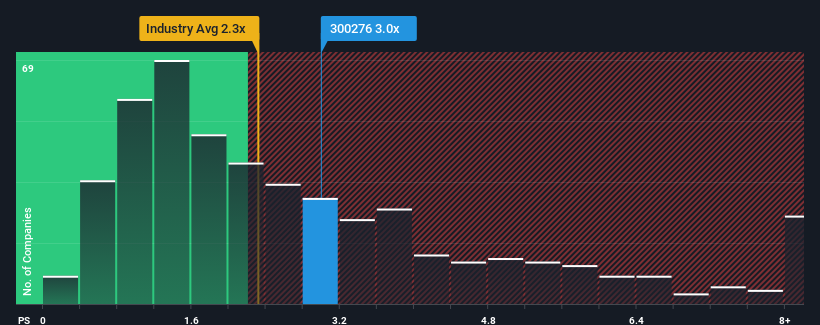

When you see that almost half of the companies in the Machinery industry in China have price-to-sales ratios (or "P/S") below 2.3x, SanFeng Intelligent Equipment Group Co., Ltd. (SZSE:300276) looks to be giving off some sell signals with its 3x P/S ratio. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for SanFeng Intelligent Equipment Group

What Does SanFeng Intelligent Equipment Group's P/S Mean For Shareholders?

SanFeng Intelligent Equipment Group has been doing a good job lately as it's been growing revenue at a solid pace. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on SanFeng Intelligent Equipment Group will help you shine a light on its historical performance.How Is SanFeng Intelligent Equipment Group's Revenue Growth Trending?

In order to justify its P/S ratio, SanFeng Intelligent Equipment Group would need to produce impressive growth in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 23% last year. The strong recent performance means it was also able to grow revenue by 61% in total over the last three years. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 22% shows it's noticeably less attractive.

With this in mind, we find it worrying that SanFeng Intelligent Equipment Group's P/S exceeds that of its industry peers. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

The fact that SanFeng Intelligent Equipment Group currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we observe slower-than-industry revenue growth alongside a high P/S ratio, we assume there to be a significant risk of the share price decreasing, which would result in a lower P/S ratio. Unless the recent medium-term conditions improve markedly, it's very challenging to accept these the share price as being reasonable.

Having said that, be aware SanFeng Intelligent Equipment Group is showing 1 warning sign in our investment analysis, you should know about.

If these risks are making you reconsider your opinion on SanFeng Intelligent Equipment Group, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300276

SanFeng Intelligent Equipment Group

SanFeng Intelligent Equipment Group Co., Ltd.

Adequate balance sheet with acceptable track record.

Market Insights

Community Narratives