Advertisement

- China

- /

- Electrical

- /

- SZSE:300001

Qingdao TGOOD Electric Co., Ltd. (SZSE:300001) Looks Just Right With A 41% Price Jump

Qingdao TGOOD Electric Co., Ltd. (SZSE:300001) shareholders would be excited to see that the share price has had a great month, posting a 41% gain and recovering from prior weakness. The last 30 days bring the annual gain to a very sharp 30%.

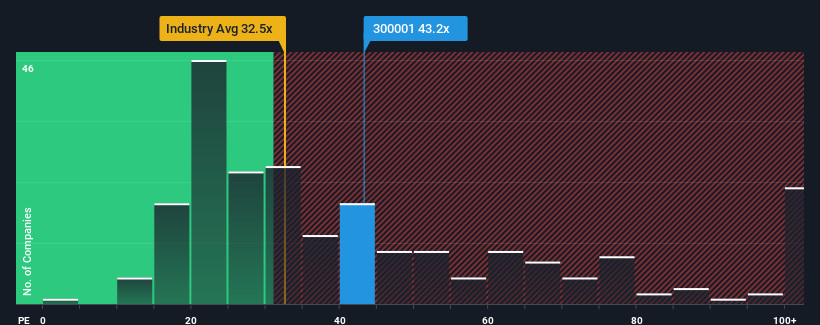

Following the firm bounce in price, Qingdao TGOOD Electric may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 43.2x, since almost half of all companies in China have P/E ratios under 33x and even P/E's lower than 20x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Qingdao TGOOD Electric certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. The P/E is probably high because investors think the company will continue to navigate the broader market headwinds better than most. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Qingdao TGOOD Electric

How Is Qingdao TGOOD Electric's Growth Trending?

There's an inherent assumption that a company should outperform the market for P/E ratios like Qingdao TGOOD Electric's to be considered reasonable.

Taking a look back first, we see that the company grew earnings per share by an impressive 88% last year. The latest three year period has also seen an excellent 197% overall rise in EPS, aided by its short-term performance. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Shifting to the future, estimates from the twelve analysts covering the company suggest earnings should grow by 28% per annum over the next three years. With the market only predicted to deliver 19% per annum, the company is positioned for a stronger earnings result.

With this information, we can see why Qingdao TGOOD Electric is trading at such a high P/E compared to the market. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Qingdao TGOOD Electric's P/E

Qingdao TGOOD Electric's P/E is getting right up there since its shares have risen strongly. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Qingdao TGOOD Electric's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. At this stage investors feel the potential for a deterioration in earnings isn't great enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

Many other vital risk factors can be found on the company's balance sheet. Take a look at our free balance sheet analysis for Qingdao TGOOD Electric with six simple checks on some of these key factors.

If you're unsure about the strength of Qingdao TGOOD Electric's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Qingdao TGOOD Electric might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:300001

Qingdao TGOOD Electric

Provides the electrical transmission and distribution solutions in China and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor