Zhejiang Taitan Co.,Ltd.'s (SZSE:003036) Stock Has Shown Weakness Lately But Financial Prospects Look Decent: Is The Market Wrong?

It is hard to get excited after looking at Zhejiang TaitanLtd's (SZSE:003036) recent performance, when its stock has declined 15% over the past week. However, the company's fundamentals look pretty decent, and long-term financials are usually aligned with future market price movements. Particularly, we will be paying attention to Zhejiang TaitanLtd's ROE today.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

View our latest analysis for Zhejiang TaitanLtd

How To Calculate Return On Equity?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Zhejiang TaitanLtd is:

6.5% = CN¥93m ÷ CN¥1.4b (Based on the trailing twelve months to September 2024).

The 'return' is the profit over the last twelve months. So, this means that for every CN¥1 of its shareholder's investments, the company generates a profit of CN¥0.06.

What Is The Relationship Between ROE And Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Zhejiang TaitanLtd's Earnings Growth And 6.5% ROE

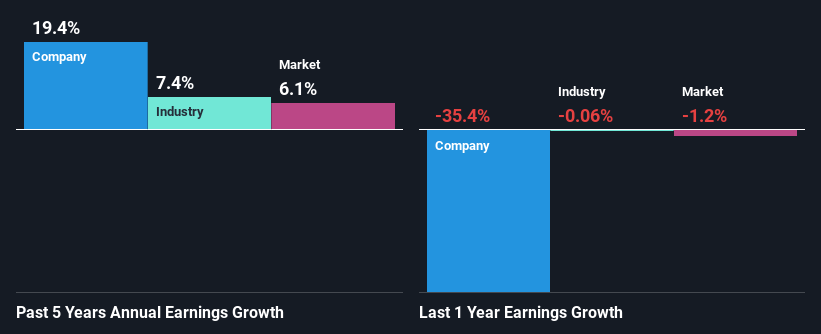

On the face of it, Zhejiang TaitanLtd's ROE is not much to talk about. Yet, a closer study shows that the company's ROE is similar to the industry average of 6.3%. On the other hand, Zhejiang TaitanLtd reported a moderate 19% net income growth over the past five years. Taking into consideration that the ROE is not particularly high, we reckon that there could also be other factors at play which could be influencing the company's growth. For instance, the company has a low payout ratio or is being managed efficiently.

Next, on comparing with the industry net income growth, we found that Zhejiang TaitanLtd's growth is quite high when compared to the industry average growth of 7.4% in the same period, which is great to see.

Earnings growth is an important metric to consider when valuing a stock. What investors need to determine next is if the expected earnings growth, or the lack of it, is already built into the share price. Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Zhejiang TaitanLtd's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Zhejiang TaitanLtd Efficiently Re-investing Its Profits?

Zhejiang TaitanLtd has a three-year median payout ratio of 26%, which implies that it retains the remaining 74% of its profits. This suggests that its dividend is well covered, and given the decent growth seen by the company, it looks like management is reinvesting its earnings efficiently.

Moreover, Zhejiang TaitanLtd is determined to keep sharing its profits with shareholders which we infer from its long history of four years of paying a dividend.

Conclusion

On the whole, we do feel that Zhejiang TaitanLtd has some positive attributes. Despite its low rate of return, the fact that the company reinvests a very high portion of its profits into its business, no doubt contributed to its high earnings growth. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. You can see the 3 risks we have identified for Zhejiang TaitanLtd by visiting our risks dashboard for free on our platform here.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang TaitanLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:003036

Zhejiang TaitanLtd

Engages in the research and development, manufacture, sale, and service of textile machinery in China and internationally.

Adequate balance sheet low.

Market Insights

Community Narratives