Shenzhen HEKEDA Precision Cleaning Equipment Co., Ltd.'s (SZSE:002816) Shares May Have Run Too Fast Too Soon

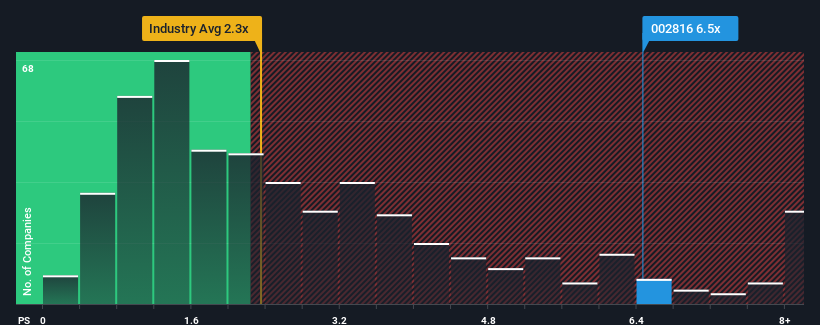

Shenzhen HEKEDA Precision Cleaning Equipment Co., Ltd.'s (SZSE:002816) price-to-sales (or "P/S") ratio of 6.5x may look like a poor investment opportunity when you consider close to half the companies in the Machinery industry in China have P/S ratios below 2.3x. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Shenzhen HEKEDA Precision Cleaning Equipment

How Shenzhen HEKEDA Precision Cleaning Equipment Has Been Performing

Shenzhen HEKEDA Precision Cleaning Equipment has been doing a good job lately as it's been growing revenue at a solid pace. One possibility is that the P/S ratio is high because investors think this respectable revenue growth will be enough to outperform the broader industry in the near future. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Shenzhen HEKEDA Precision Cleaning Equipment will help you shine a light on its historical performance.Is There Enough Revenue Growth Forecasted For Shenzhen HEKEDA Precision Cleaning Equipment?

In order to justify its P/S ratio, Shenzhen HEKEDA Precision Cleaning Equipment would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 19% last year. However, this wasn't enough as the latest three year period has seen the company endure a nasty 23% drop in revenue in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenues over that time.

Weighing that medium-term revenue trajectory against the broader industry's one-year forecast for expansion of 22% shows it's an unpleasant look.

In light of this, it's alarming that Shenzhen HEKEDA Precision Cleaning Equipment's P/S sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. Only the boldest would assume these prices are sustainable as a continuation of recent revenue trends is likely to weigh heavily on the share price eventually.

The Final Word

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Shenzhen HEKEDA Precision Cleaning Equipment revealed its shrinking revenue over the medium-term isn't resulting in a P/S as low as we expected, given the industry is set to grow. Right now we aren't comfortable with the high P/S as this revenue performance is highly unlikely to support such positive sentiment for long. Unless the recent medium-term conditions improve markedly, investors will have a hard time accepting the share price as fair value.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Shenzhen HEKEDA Precision Cleaning Equipment, and understanding them should be part of your investment process.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002816

Shenzhen HEKEDA Precision Cleaning Equipment

Shenzhen HEKEDA Precision Cleaning Equipment Co., Ltd.

Mediocre balance sheet low.

Market Insights

Community Narratives