Advertisement

- China

- /

- Construction

- /

- SZSE:002457

Ningxia Qinglong Pipes Industry Group Co., Ltd.'s (SZSE:002457) Shares Climb 38% But Its Business Is Yet to Catch Up

The Ningxia Qinglong Pipes Industry Group Co., Ltd. (SZSE:002457) share price has done very well over the last month, posting an excellent gain of 38%. Looking back a bit further, it's encouraging to see the stock is up 48% in the last year.

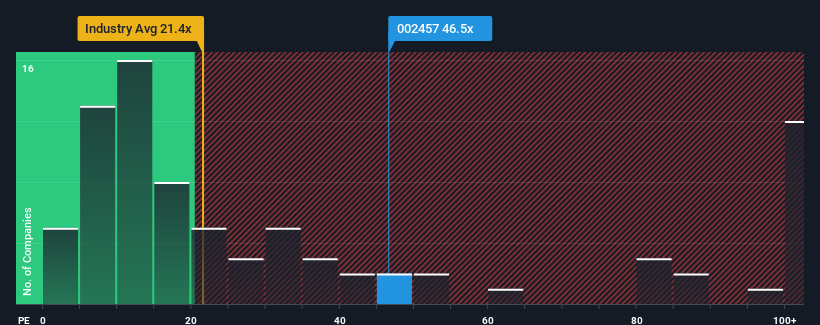

Since its price has surged higher, Ningxia Qinglong Pipes Industry Group may be sending bearish signals at the moment with its price-to-earnings (or "P/E") ratio of 46.5x, since almost half of all companies in China have P/E ratios under 32x and even P/E's lower than 19x are not unusual. However, the P/E might be high for a reason and it requires further investigation to determine if it's justified.

For example, consider that Ningxia Qinglong Pipes Industry Group's financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

Check out our latest analysis for Ningxia Qinglong Pipes Industry Group

What Are Growth Metrics Telling Us About The High P/E?

Ningxia Qinglong Pipes Industry Group's P/E ratio would be typical for a company that's expected to deliver solid growth, and importantly, perform better than the market.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 43%. This means it has also seen a slide in earnings over the longer-term as EPS is down 63% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Comparing that to the market, which is predicted to deliver 37% growth in the next 12 months, the company's downward momentum based on recent medium-term earnings results is a sobering picture.

In light of this, it's alarming that Ningxia Qinglong Pipes Industry Group's P/E sits above the majority of other companies. It seems most investors are ignoring the recent poor growth rate and are hoping for a turnaround in the company's business prospects. There's a very good chance existing shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the recent negative growth rates.

The Key Takeaway

The large bounce in Ningxia Qinglong Pipes Industry Group's shares has lifted the company's P/E to a fairly high level. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Ningxia Qinglong Pipes Industry Group currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. Right now we are increasingly uncomfortable with the high P/E as this earnings performance is highly unlikely to support such positive sentiment for long. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

Before you settle on your opinion, we've discovered 4 warning signs for Ningxia Qinglong Pipes Industry Group (1 makes us a bit uncomfortable!) that you should be aware of.

If you're unsure about the strength of Ningxia Qinglong Pipes Industry Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Qinglong Pipes Industry Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002457

Qinglong Pipes Industry Group

Engages in the research and development, production, and sale of water pipelines and related products in China.

Solid track record with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|31.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|53.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor