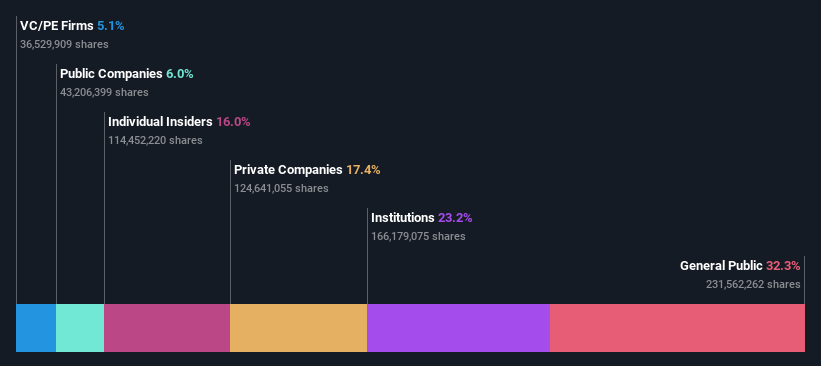

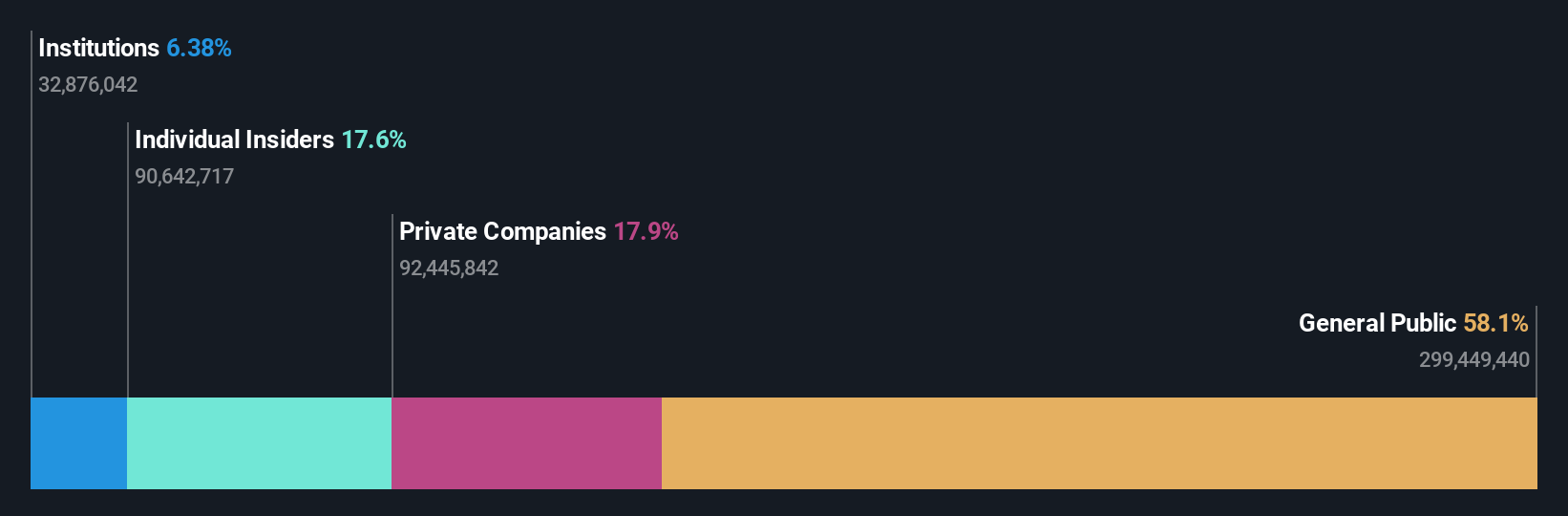

As global markets face challenges from trade policy uncertainties and inflation concerns, investors are increasingly looking toward Asia for growth opportunities. In this environment, companies with high insider ownership can be particularly appealing as they often signal strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| NEXTIN (KOSDAQ:A348210) | 12.4% | 27% |

| Laopu Gold (SEHK:6181) | 36.4% | 42.9% |

| Global Tax Free (KOSDAQ:A204620) | 20.4% | 89.3% |

| Schooinc (TSE:264A) | 21.6% | 68.9% |

| BIWIN Storage Technology (SHSE:688525) | 18.9% | 57.6% |

| Ascentage Pharma Group International (SEHK:6855) | 17.9% | 60.9% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 125.9% |

| Vuno (KOSDAQ:A338220) | 15.6% | 131% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

Here's a peek at a few of the choices from the screener.

Smoore International Holdings (SEHK:6969)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Smoore International Holdings Limited is an investment holding company that provides vaping technology solutions, with a market cap of HK$73.80 billion.

Operations: Smoore International Holdings Limited generates its revenue primarily from the provision of vaping technology solutions.

Insider Ownership: 39.1%

Revenue Growth Forecast: 13.3% p.a.

Smoore International Holdings is poised for significant growth, with earnings expected to rise 21.4% annually over the next three years, outpacing the Hong Kong market's 11.7%. Despite trading at 33.6% below its estimated fair value, its forecasted Return on Equity remains low at 8.5%. Revenue is projected to grow by 13.3% per year, faster than the market average but below high-growth thresholds. A recent shareholders meeting addressed share repurchase mandates and other governance matters.

- Click here to discover the nuances of Smoore International Holdings with our detailed analytical future growth report.

- The valuation report we've compiled suggests that Smoore International Holdings' current price could be inflated.

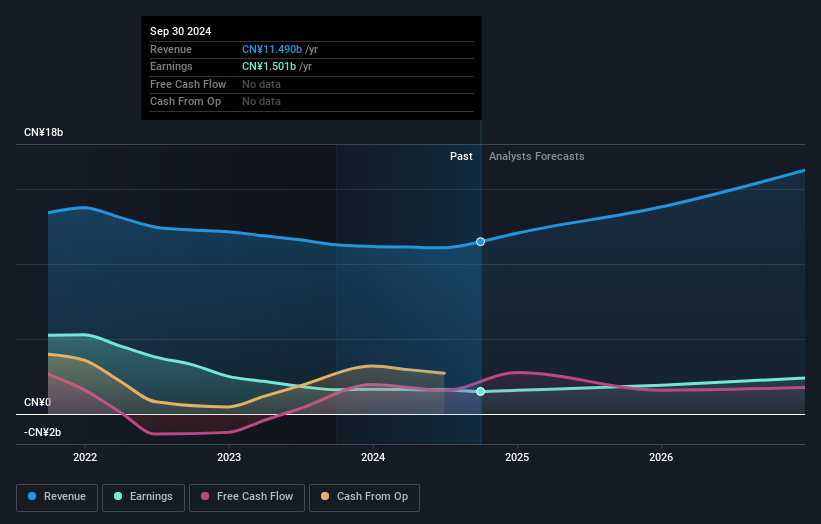

Ninebot (SHSE:689009)

Simply Wall St Growth Rating: ★★★★★★

Overview: Ninebot Limited is involved in the design, research and development, production, sale, and servicing of transportation and robot products globally, with a market cap of approximately CN¥43.31 billion.

Operations: Revenue Segments (in millions of CN¥):

Insider Ownership: 15.4%

Revenue Growth Forecast: 22.1% p.a.

Ninebot's earnings grew 81.9% last year, with revenue rising from CNY 10.22 billion to CNY 14.17 billion, and net income increasing to CNY 1.09 billion. Forecasts suggest annual earnings growth of 33.5%, surpassing China's market average of 25.5%, while revenue is expected to grow by 22.1% annually, outpacing the market's 13.3%. The company's Return on Equity is projected to reach a high level in three years, indicating strong potential for future profitability despite no recent insider trading activity reported.

- Navigate through the intricacies of Ninebot with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that Ninebot's share price might be on the expensive side.

Kehua Data (SZSE:002335)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kehua Data Co., Ltd. offers integrated solutions for power protection and energy conservation globally, with a market cap of CN¥23.37 billion.

Operations: Kehua Data's revenue primarily comes from its integrated solutions in power protection and energy conservation.

Insider Ownership: 21.5%

Revenue Growth Forecast: 18% p.a.

Kehua Data is anticipated to achieve annual earnings growth of 42.5%, exceeding the Chinese market's average of 25.5%. However, its revenue growth forecast of 18% lags behind the ideal threshold but still surpasses the market's 13.3%. Despite a low projected Return on Equity of 12.7% in three years and declining profit margins from last year, no significant insider trading activity has been reported recently, though share price volatility remains high.

- Get an in-depth perspective on Kehua Data's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, Kehua Data's share price might be too optimistic.

Next Steps

- Click through to start exploring the rest of the 640 Fast Growing Asian Companies With High Insider Ownership now.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Ninebot might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:689009

Ninebot

Engages in the design, research and development, production, sale, and servicing of transportation and robot products worldwide.

Exceptional growth potential with flawless balance sheet.