Dalian Huarui Heavy Industry Group Co., LTD.'s (SZSE:002204) Price Is Right But Growth Is Lacking After Shares Rocket 31%

The Dalian Huarui Heavy Industry Group Co., LTD. (SZSE:002204) share price has done very well over the last month, posting an excellent gain of 31%. Looking back a bit further, it's encouraging to see the stock is up 32% in the last year.

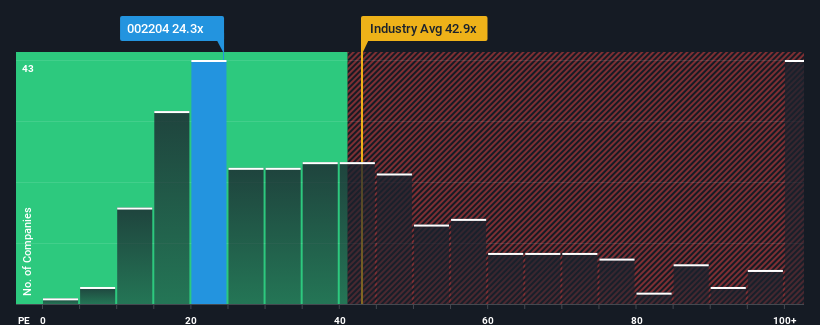

Although its price has surged higher, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 40x, you may still consider Dalian Huarui Heavy Industry Group as an attractive investment with its 24.3x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Dalian Huarui Heavy Industry Group certainly has been doing a good job lately as its earnings growth has been positive while most other companies have been seeing their earnings go backwards. One possibility is that the P/E is low because investors think the company's earnings are going to fall away like everyone else's soon. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

View our latest analysis for Dalian Huarui Heavy Industry Group

How Is Dalian Huarui Heavy Industry Group's Growth Trending?

Dalian Huarui Heavy Industry Group's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings growth, the company posted a terrific increase of 39%. The strong recent performance means it was also able to grow EPS by 339% in total over the last three years. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

Looking ahead now, EPS is anticipated to climb by 11% during the coming year according to the lone analyst following the company. Meanwhile, the rest of the market is forecast to expand by 37%, which is noticeably more attractive.

In light of this, it's understandable that Dalian Huarui Heavy Industry Group's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Final Word

Despite Dalian Huarui Heavy Industry Group's shares building up a head of steam, its P/E still lags most other companies. Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

We've established that Dalian Huarui Heavy Industry Group maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Don't forget that there may be other risks. For instance, we've identified 1 warning sign for Dalian Huarui Heavy Industry Group that you should be aware of.

If you're unsure about the strength of Dalian Huarui Heavy Industry Group's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002204

Dalian Huarui Heavy Industry Group

Dalian Huarui Heavy Industry Group Co., Ltd.

Proven track record with adequate balance sheet.

Market Insights

Community Narratives