3 Chinese Growth Stocks Insiders Own With Up To 53% Earnings Growth

Reviewed by Simply Wall St

Chinese stocks have recently faced declines due to weak inflation data, raising concerns about economic stability. Despite these challenges, growth companies with high insider ownership can offer unique opportunities for investors, as they often benefit from strong internal commitment and potential for significant earnings growth. In the current market environment, identifying stocks with robust insider ownership and promising earnings projections can be a strategic move. Here are three Chinese growth stocks that insiders own and that boast up to 53% earnings growth.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 18% | 28.7% |

| Jiayou International LogisticsLtd (SHSE:603871) | 22.6% | 24.6% |

| Western Regions Tourism DevelopmentLtd (SZSE:300859) | 13.9% | 39.2% |

| Arctech Solar Holding (SHSE:688408) | 38.6% | 29.9% |

| Quick Intelligent EquipmentLtd (SHSE:603203) | 34.4% | 33.1% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 67.5% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 41.7% |

| UTour Group (SZSE:002707) | 23% | 25.2% |

| BIWIN Storage Technology (SHSE:688525) | 18.8% | 116.8% |

| Offcn Education Technology (SZSE:002607) | 25.1% | 75.7% |

Let's explore several standout options from the results in the screener.

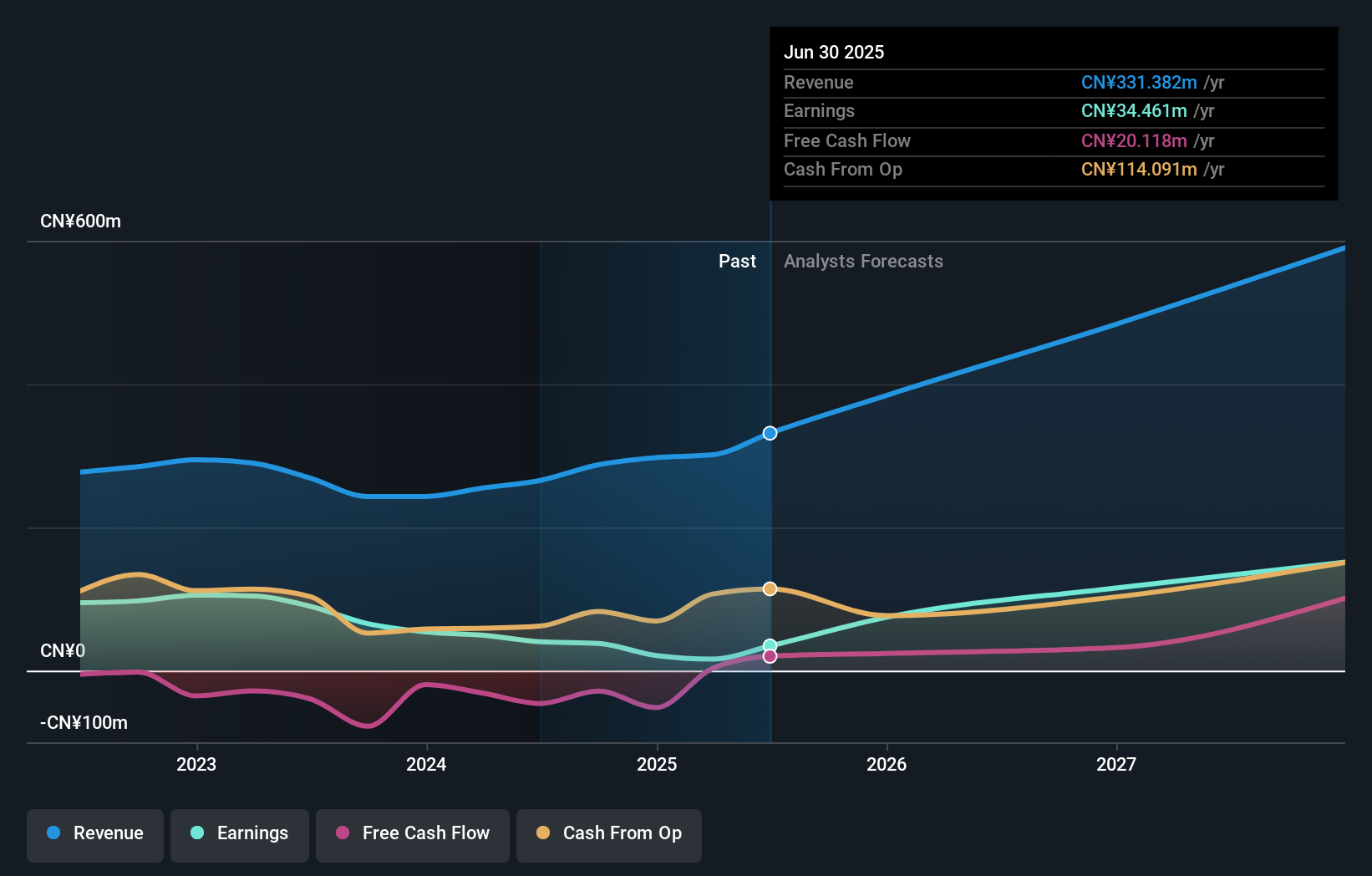

Shanghai OPM Biosciences (SHSE:688293)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai OPM Biosciences Co., Ltd. offers cell culture media and CDMO services both in China and internationally, with a market cap of CN¥3.10 billion.

Operations: The company's revenue segments include cell culture media and CDMO services provided both domestically and internationally.

Insider Ownership: 24.9%

Earnings Growth Forecast: 53.9% p.a.

Shanghai OPM Biosciences, with substantial insider ownership, is forecasted to see significant earnings growth of 53.9% annually over the next three years, outpacing the Chinese market's average. Despite a recent decline in profit margins to 15.2%, revenue for the first half of 2024 increased to CNY 143.61 million from CNY 121.25 million last year. The company has also completed share repurchases worth CNY 46.61 million, indicating confidence in its future prospects.

- Delve into the full analysis future growth report here for a deeper understanding of Shanghai OPM Biosciences.

- Insights from our recent valuation report point to the potential overvaluation of Shanghai OPM Biosciences shares in the market.

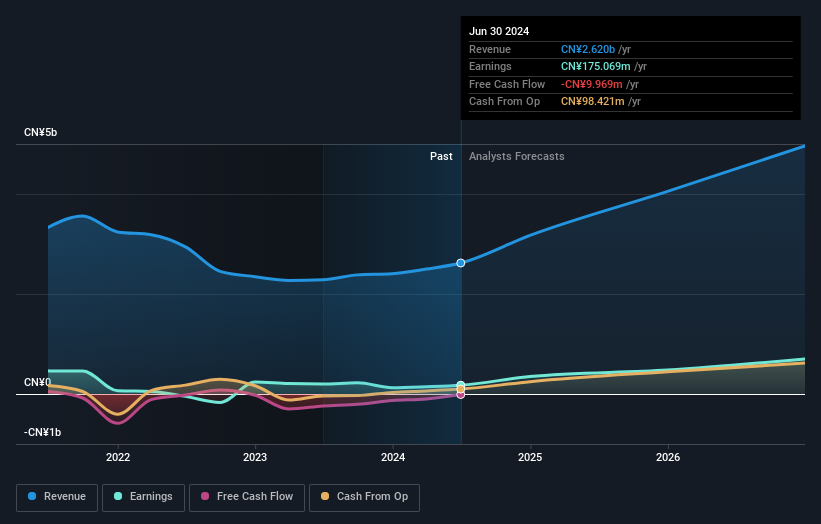

Weihai Guangtai Airport EquipmentLtd (SZSE:002111)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Weihai Guangtai Airport Equipment Co., Ltd manufactures and sells ground support and fire-fighting equipment in China and internationally, with a market cap of CN¥4.66 billion.

Operations: Weihai Guangtai Airport Equipment Co., Ltd's revenue segments include ground support equipment (CN¥1.68 billion) and fire-fighting equipment (CN¥0.92 billion).

Insider Ownership: 17.1%

Earnings Growth Forecast: 41.7% p.a.

Weihai Guangtai Airport Equipment Ltd. exhibits high insider ownership and is poised for substantial growth, with earnings forecasted to increase by 41.7% annually, outpacing the Chinese market average. Recent half-year results show revenue rising to CNY 1.28 billion from CNY 1.07 billion and net income doubling to CNY 107.39 million year-over-year, reflecting robust business performance despite a dividend that is not well-covered by earnings or free cash flows.

- Click here and access our complete growth analysis report to understand the dynamics of Weihai Guangtai Airport EquipmentLtd.

- Our expertly prepared valuation report Weihai Guangtai Airport EquipmentLtd implies its share price may be too high.

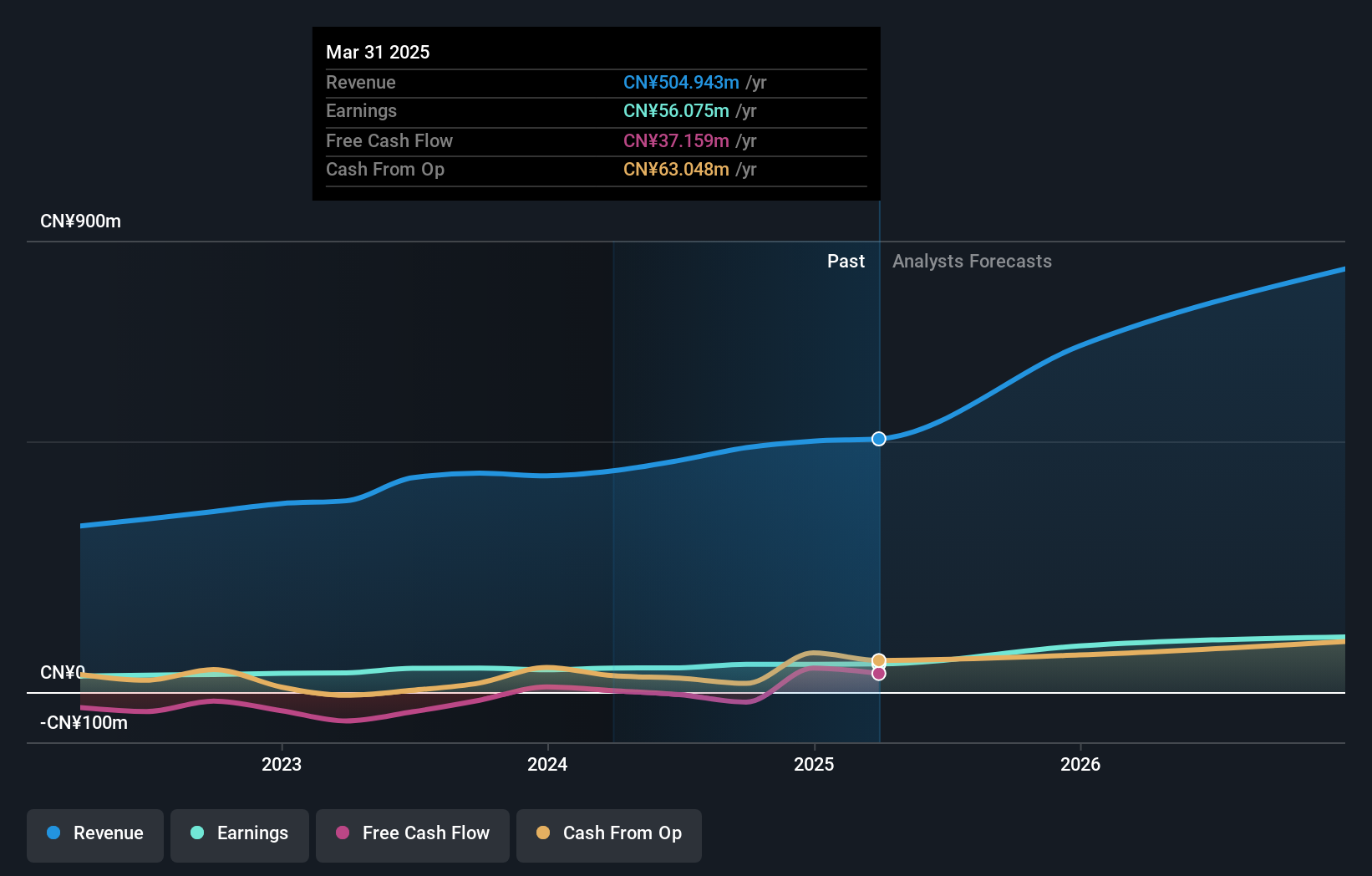

Chongqing Mas Sci.&Tech.Co.Ltd (SZSE:300275)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Chongqing Mas Sci.&Tech.Co.,Ltd. provides safety technology equipment and safety information services in China and has a market cap of CN¥3.17 billion.

Operations: Chongqing Mas Sci.&Tech.Co.Ltd's revenue segments include safety technology equipment and safety information services in China.

Insider Ownership: 21.8%

Earnings Growth Forecast: 30.5% p.a.

Chongqing Mas Sci.&Tech.Co.Ltd. demonstrates significant growth potential with earnings forecasted to grow 30.5% annually, surpassing the Chinese market average of 23%. Recent half-year results show revenue increasing to CNY 232.32 million from CNY 201.75 million year-over-year, and net income rising to CNY 32.21 million from CNY 28.35 million. The company also announced a private placement aiming to raise up to CNY 180 million, indicating strong insider confidence and future expansion plans.

- Click here to discover the nuances of Chongqing Mas Sci.&Tech.Co.Ltd with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Chongqing Mas Sci.&Tech.Co.Ltd is trading beyond its estimated value.

Taking Advantage

- Investigate our full lineup of 379 Fast Growing Chinese Companies With High Insider Ownership right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Weihai Guangtai Airport EquipmentLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002111

Weihai Guangtai Airport EquipmentLtd

Engages in manufacture and sale of ground support equipment and fire-fighting equipment in China and internationally.

High growth potential with adequate balance sheet.