- China

- /

- Construction

- /

- SZSE:000065

NORINCO International Cooperation Ltd. (SZSE:000065) Shares Fly 29% But Investors Aren't Buying For Growth

NORINCO International Cooperation Ltd. (SZSE:000065) shares have had a really impressive month, gaining 29% after a shaky period beforehand. Taking a wider view, although not as strong as the last month, the full year gain of 13% is also fairly reasonable.

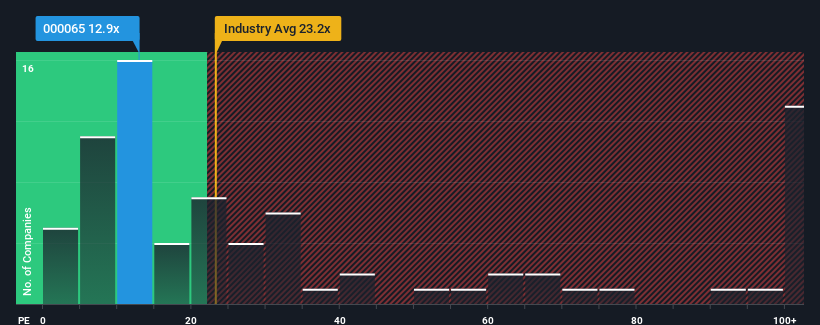

Although its price has surged higher, NORINCO International Cooperation's price-to-earnings (or "P/E") ratio of 12.9x might still make it look like a strong buy right now compared to the market in China, where around half of the companies have P/E ratios above 39x and even P/E's above 75x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

With its earnings growth in positive territory compared to the declining earnings of most other companies, NORINCO International Cooperation has been doing quite well of late. It might be that many expect the strong earnings performance to degrade substantially, possibly more than the market, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for NORINCO International Cooperation

What Are Growth Metrics Telling Us About The Low P/E?

There's an inherent assumption that a company should far underperform the market for P/E ratios like NORINCO International Cooperation's to be considered reasonable.

If we review the last year of earnings growth, the company posted a terrific increase of 25%. Although, its longer-term performance hasn't been as strong with three-year EPS growth being relatively non-existent overall. Therefore, it's fair to say that earnings growth has been inconsistent recently for the company.

Looking ahead now, EPS is anticipated to climb by 6.4% during the coming year according to the three analysts following the company. With the market predicted to deliver 37% growth , the company is positioned for a weaker earnings result.

In light of this, it's understandable that NORINCO International Cooperation's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

The Bottom Line On NORINCO International Cooperation's P/E

Shares in NORINCO International Cooperation are going to need a lot more upward momentum to get the company's P/E out of its slump. It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that NORINCO International Cooperation maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for NORINCO International Cooperation that you should be aware of.

If you're unsure about the strength of NORINCO International Cooperation's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if NORINCO International Cooperation might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:000065

NORINCO International Cooperation

Operates as an engineering contractor in Asia, Africa, the Middle East, and internationally.

Solid track record with adequate balance sheet and pays a dividend.

Market Insights

Community Narratives