- China

- /

- Electronic Equipment and Components

- /

- SZSE:002913

Top Growth Companies With Insider Ownership In December 2024

Reviewed by Simply Wall St

In a week marked by record highs for major U.S. stock indexes, growth stocks have notably outperformed their value counterparts, driven by strong performances in sectors like consumer discretionary and information technology. As investors navigate these buoyant market conditions, companies with high insider ownership can be particularly attractive due to the confidence insiders demonstrate in their business's potential for sustained growth.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.4% | 37.3% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 26.3% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.3% |

| Laopu Gold (SEHK:6181) | 36.4% | 34.2% |

| Medley (TSE:4480) | 34% | 31.7% |

| Plenti Group (ASX:PLT) | 12.8% | 120.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 131.1% |

| Fulin Precision (SZSE:300432) | 13.6% | 66.7% |

| HANA Micron (KOSDAQ:A067310) | 18.4% | 110.9% |

| Findi (ASX:FND) | 34.8% | 112.9% |

Here we highlight a subset of our preferred stocks from the screener.

P/F Bakkafrost (OB:BAKKA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: P/F Bakkafrost, along with its subsidiaries, is engaged in the production and sale of salmon products across North America, Western Europe, Eastern Europe, Asia, and other international markets; it has a market cap of NOK39.29 billion.

Operations: The company's revenue segments include Services (DKK 899.29 million), Sales and Other (DKK 10.27 billion), Farming Scotland (DKK 1.68 billion), Freshwater Scotland (DKK 119.99 million), Farming Faroe Islands (DKK 3.92 billion), Fishmeal, Oil and Feed (DKK 3.13 billion), and Freshwater Faroe Islands (DKK 686.59 million).

Insider Ownership: 13.3%

Revenue Growth Forecast: 15.4% p.a.

P/F Bakkafrost has experienced more insider buying than selling in the past three months, indicating potential confidence from insiders. Despite a recent quarterly net loss of DKK 113.72 million, the company’s earnings are expected to grow significantly at 63% annually over the next three years, outpacing market averages. However, its return on equity is projected to remain low at 15.2%. Revenue growth is forecasted at 15.4% annually, slower than desired for high-growth companies.

- Navigate through the intricacies of P/F Bakkafrost with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that P/F Bakkafrost is trading beyond its estimated value.

Dalian Haosen Intelligent Manufacturing (SHSE:688529)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dalian Haosen Intelligent Manufacturing Co., Ltd. operates in the intelligent manufacturing sector with a market cap of CN¥3.44 billion.

Operations: Dalian Haosen Intelligent Manufacturing Co., Ltd. generates its revenue from various segments within the intelligent manufacturing sector.

Insider Ownership: 23.8%

Revenue Growth Forecast: 17.3% p.a.

Dalian Haosen Intelligent Manufacturing's earnings are forecast to grow significantly at 87.12% annually, with the company expected to become profitable in three years, surpassing market averages. Revenue is projected to grow at 17.3% per year, faster than the Chinese market average of 13.7%. However, recent financial results show a decline in net income from CNY 101.76 million to CNY 7.68 million year-on-year, indicating potential challenges despite growth prospects.

- Unlock comprehensive insights into our analysis of Dalian Haosen Intelligent Manufacturing stock in this growth report.

- According our valuation report, there's an indication that Dalian Haosen Intelligent Manufacturing's share price might be on the expensive side.

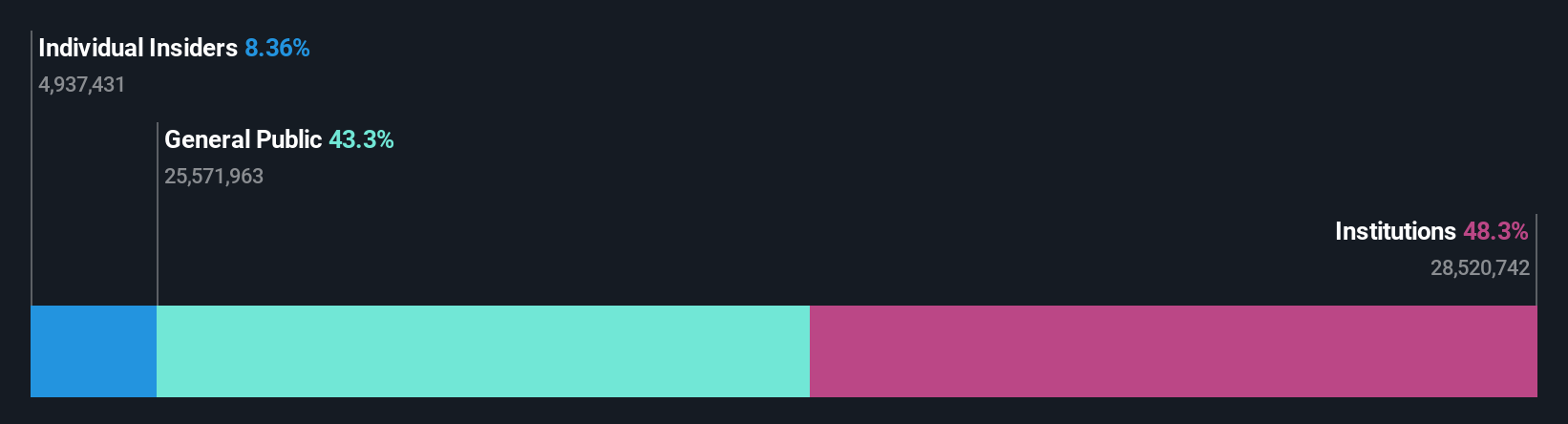

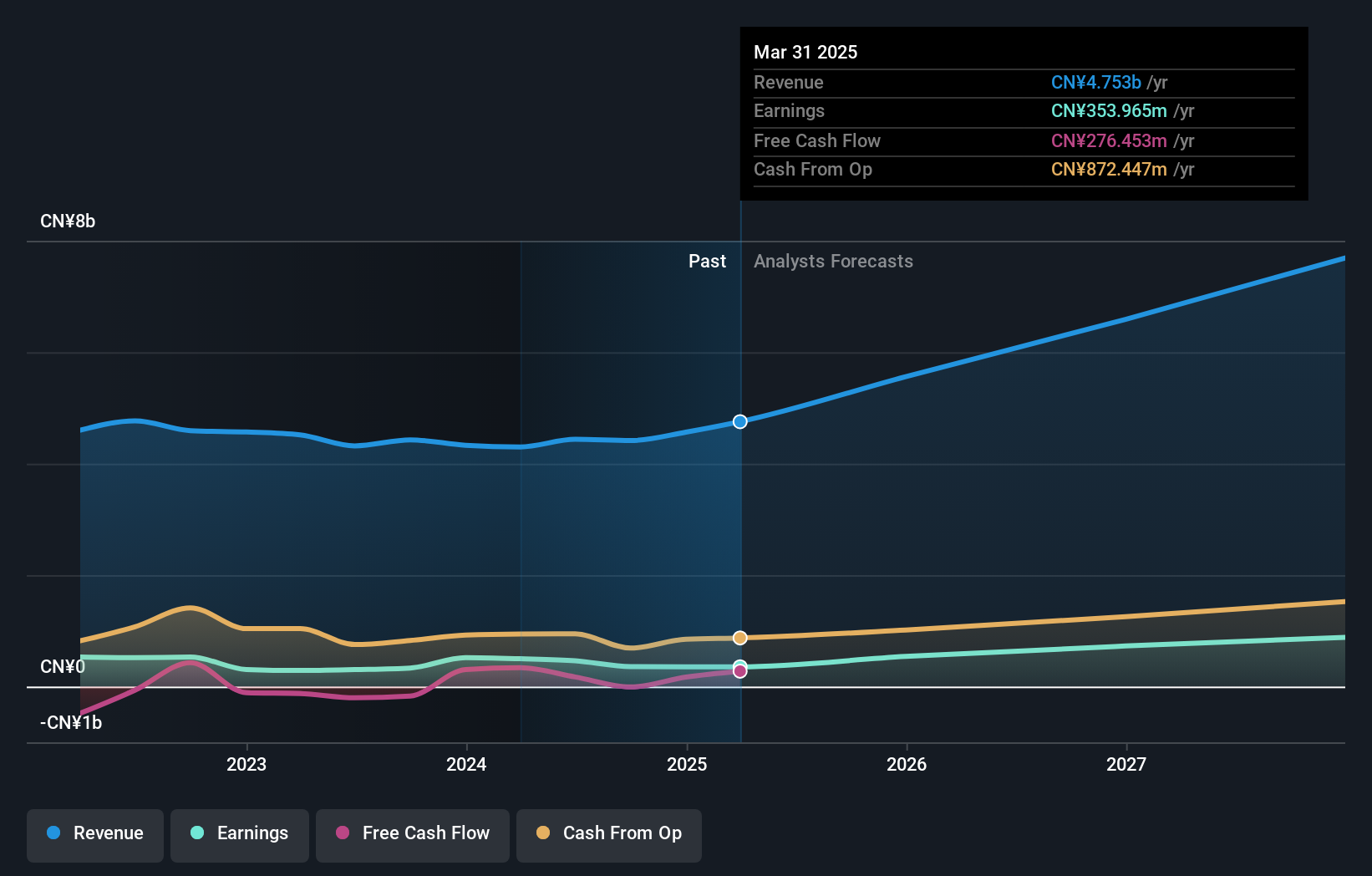

Aoshikang Technology (SZSE:002913)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Aoshikang Technology Co., Ltd. specializes in the research, development, production, and sale of printed circuit boards and has a market cap of CN¥7.98 billion.

Operations: The company's revenue is primarily derived from its printed circuit boards segment, totaling CN¥4.41 billion.

Insider Ownership: 22.7%

Revenue Growth Forecast: 19% p.a.

Aoshikang Technology's earnings are projected to grow significantly at 30.72% annually, outpacing the Chinese market average of 25.9%. Revenue is expected to increase by 19% per year, also surpassing the market growth rate of 13.7%. Despite a recent decline in net income from CNY 440.52 million to CNY 278.81 million, the company trades at a substantial discount to its estimated fair value and has not seen significant insider trading activity recently.

- Click here to discover the nuances of Aoshikang Technology with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Aoshikang Technology is priced lower than what may be justified by its financials.

Seize The Opportunity

- Click here to access our complete index of 1510 Fast Growing Companies With High Insider Ownership.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Aoshikang Technology, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002913

Aoshikang Technology

Engages in the research, development, production, and sale of printed circuit boards.

High growth potential with excellent balance sheet and pays a dividend.

Market Insights

Community Narratives