- Taiwan

- /

- Tech Hardware

- /

- TWSE:2356

3 Growth Companies With High Insider Ownership Growing Earnings Up To 34%

Reviewed by Simply Wall St

As global markets navigate a landscape of cooling inflation and strong bank earnings, the major U.S. stock indexes have rebounded, with value stocks recently outperforming growth shares. In this environment, identifying growth companies with high insider ownership can be particularly appealing as they often signal confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Propel Holdings (TSX:PRL) | 36.8% | 38.9% |

| CD Projekt (WSE:CDR) | 29.7% | 30.6% |

| On Holding (NYSE:ONON) | 19.1% | 29.8% |

| Pharma Mar (BME:PHM) | 11.9% | 56.1% |

| Kingstone Companies (NasdaqCM:KINS) | 20.8% | 24.9% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.3% |

| Elliptic Laboratories (OB:ELABS) | 26.8% | 121.1% |

| Findi (ASX:FND) | 35.8% | 110.7% |

Let's take a closer look at a couple of our picks from the screened companies.

Zhuzhou Huarui Precision Cutting ToolsLtd (SHSE:688059)

Simply Wall St Growth Rating: ★★★★☆☆

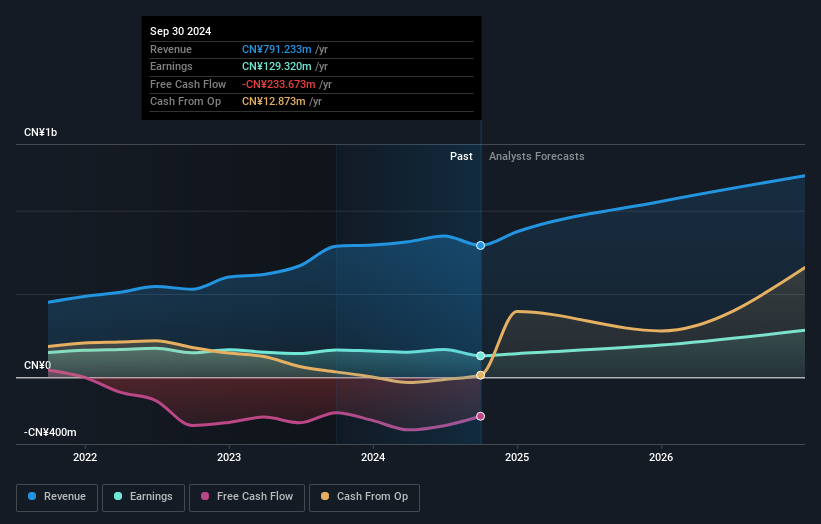

Overview: Zhuzhou Huarui Precision Cutting Tools Co., Ltd. specializes in the production of precision cutting tools and has a market cap of CN¥2.78 billion.

Operations: The company's revenue primarily comes from the Machinery & Industrial Equipment segment, which generated CN¥791.23 million.

Insider Ownership: 15.6%

Earnings Growth Forecast: 34.9% p.a.

Zhuzhou Huarui Precision Cutting Tools Ltd. demonstrates strong growth potential with earnings forecasted to increase significantly at 34.9% annually, outpacing the CN market's 25.2%. Despite a recent drop from the S&P Global BMI Index and declining net income (CNY 77.06 million vs CNY 105.64 million year-over-year), its price-to-earnings ratio of 22.8x suggests good value relative to peers, though debt coverage remains a concern due to insufficient operating cash flow support.

- Navigate through the intricacies of Zhuzhou Huarui Precision Cutting ToolsLtd with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that Zhuzhou Huarui Precision Cutting ToolsLtd's current price could be quite moderate.

PARK24 (TSE:4666)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PARK24 Co., Ltd. operates and manages parking facilities both in Japan and internationally, with a market cap of ¥337.52 billion.

Operations: The company's revenue segments include the Mobility Business generating ¥112.06 million, the Parking Lot Business in Japan contributing ¥182.30 million, and the Parking Lot Business Overseas adding ¥82.41 million.

Insider Ownership: 10.5%

Earnings Growth Forecast: 12.4% p.a.

PARK24 shows moderate growth potential with earnings expected to rise 12.37% annually, surpassing the JP market's average of 8.1%. Despite high debt levels, its return on equity is forecasted to reach a strong 29.5% in three years. Recent financials reveal increased sales of ¥370.91 billion and net income of ¥18.63 billion for fiscal year 2024, with significant dividend hikes planned for 2025, indicating confidence in future performance despite slower revenue growth projections at 6.7%.

- Click to explore a detailed breakdown of our findings in PARK24's earnings growth report.

- Our expertly prepared valuation report PARK24 implies its share price may be lower than expected.

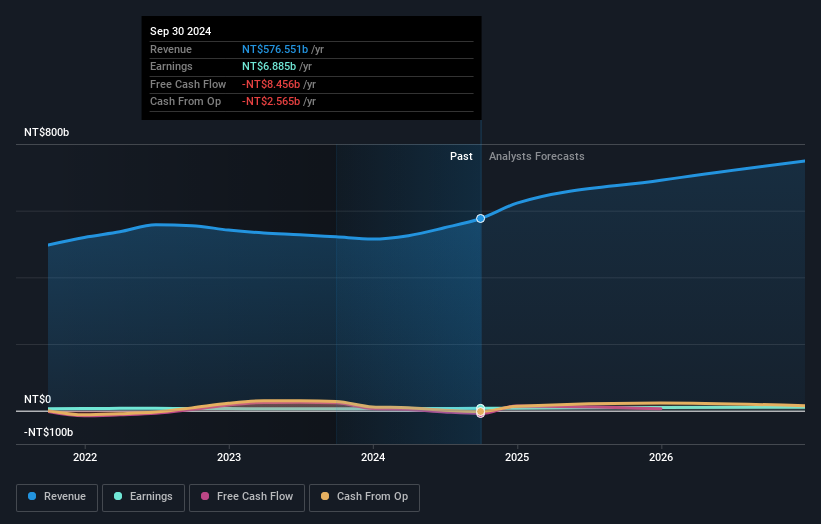

Inventec (TWSE:2356)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Inventec Corporation, along with its subsidiaries, is involved in the development, manufacturing, processing, and trading of computers and related products across Taiwan, the United States, Japan, Hong Kong, Macao, Mainland China, and globally; it has a market cap of approximately NT$179.02 billion.

Operations: The company generates revenue primarily from its Core Segment, which accounts for NT$571.40 billion.

Insider Ownership: 17.2%

Earnings Growth Forecast: 20.4% p.a.

Inventec's recent financial performance shows a solid growth trajectory, with earnings increasing by 24.3% over the past year and net income reaching TWD 1,997.69 million for Q3 2024. The company's earnings are projected to grow at an annual rate of 20.4%, outpacing the Taiwan market average of 17.3%. However, revenue growth is expected to be moderate at 11.3% annually, and debt coverage remains a concern due to insufficient operating cash flow support.

- Click here to discover the nuances of Inventec with our detailed analytical future growth report.

- Our valuation report here indicates Inventec may be overvalued.

Make It Happen

- Access the full spectrum of 1465 Fast Growing Companies With High Insider Ownership by clicking on this link.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Inventec, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2356

Inventec

Develops, manufactures, processes, and trades in computers and related products in Taiwan, the United States, Japan, Hong Kong, Macao, Mainland China, and internationally.

Mediocre balance sheet second-rate dividend payer.