We Ran A Stock Scan For Earnings Growth And Jiangsu Tongli Risheng Machinery (SHSE:605286) Passed With Ease

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Jiangsu Tongli Risheng Machinery (SHSE:605286). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Jiangsu Tongli Risheng Machinery with the means to add long-term value to shareholders.

See our latest analysis for Jiangsu Tongli Risheng Machinery

Jiangsu Tongli Risheng Machinery's Improving Profits

Even when EPS earnings per share (EPS) growth is unexceptional, company value can be created if this rate is sustained each year. So it's easy to see why many investors focus in on EPS growth. Jiangsu Tongli Risheng Machinery's EPS shot up from CN¥0.86 to CN¥1.23; a result that's bound to keep shareholders happy. That's a fantastic gain of 43%.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Our analysis has highlighted that Jiangsu Tongli Risheng Machinery's revenue from operations did not account for all of their revenue last year, so our analysis of its margins might not accurately reflect the underlying business. Despite the relatively flat revenue figures, shareholders will be pleased to see EBIT margins have grown from 6.8% to 11% in the last 12 months. That's a real positive.

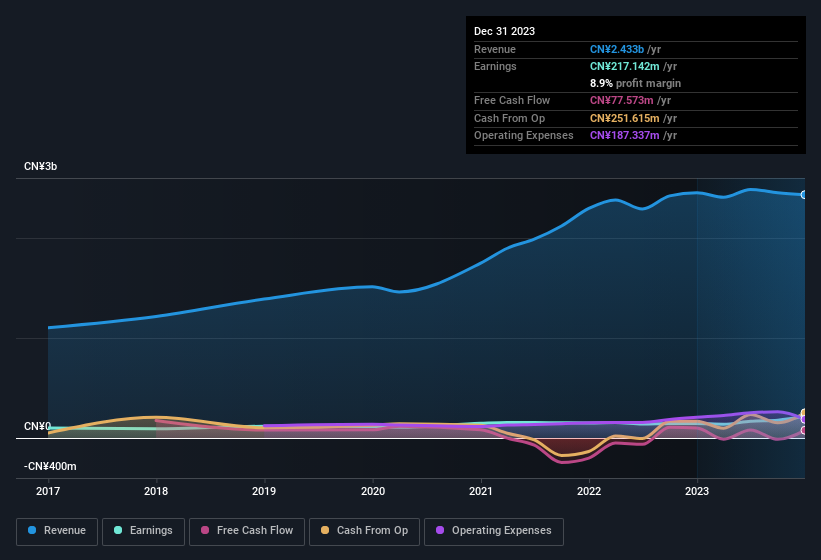

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

While it's always good to see growing profits, you should always remember that a weak balance sheet could come back to bite. So check Jiangsu Tongli Risheng Machinery's balance sheet strength, before getting too excited.

Are Jiangsu Tongli Risheng Machinery Insiders Aligned With All Shareholders?

Seeing insiders owning a large portion of the shares on issue is often a good sign. Their incentives will be aligned with the investors and there's less of a probability in a sudden sell-off that would impact the share price. So those who are interested in Jiangsu Tongli Risheng Machinery will be delighted to know that insiders have shown their belief, holding a large proportion of the company's shares. Indeed, with a collective holding of 66%, company insiders are in control and have plenty of capital behind the venture. This makes it apparent they will be incentivised to plan for the long term - a positive for shareholders with a sit and hold strategy. And their holding is extremely valuable at the current share price, totalling CN¥2.9b. That means they have plenty of their own capital riding on the performance of the business!

While it's always good to see some strong conviction in the company from insiders through heavy investment, it's also important for shareholders to ask if management compensation policies are reasonable. Well, based on the CEO pay, you'd argue that they are indeed. Our analysis has discovered that the median total compensation for the CEOs of companies like Jiangsu Tongli Risheng Machinery with market caps between CN¥1.4b and CN¥5.8b is about CN¥832k.

The Jiangsu Tongli Risheng Machinery CEO received CN¥590k in compensation for the year ending December 2022. That comes in below the average for similar sized companies and seems pretty reasonable. CEO remuneration levels are not the most important metric for investors, but when the pay is modest, that does support enhanced alignment between the CEO and the ordinary shareholders. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Is Jiangsu Tongli Risheng Machinery Worth Keeping An Eye On?

You can't deny that Jiangsu Tongli Risheng Machinery has grown its earnings per share at a very impressive rate. That's attractive. If you still have your doubts, remember too that company insiders have a considerable investment aligning themselves with the shareholders and CEO pay is quite modest compared to similarly sized companiess. Everyone has their own preferences when it comes to investing but it definitely makes Jiangsu Tongli Risheng Machinery look rather interesting indeed. However, before you get too excited we've discovered 1 warning sign for Jiangsu Tongli Risheng Machinery that you should be aware of.

While opting for stocks without growing earnings and absent insider buying can yield results, for investors valuing these key metrics, here is a carefully selected list of companies in CN with promising growth potential and insider confidence.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade Jiangsu Tongli Risheng Machinery, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:605286

Jiangsu Tongli Risheng Machinery

Jiangsu Tongli Risheng Machinery Co., Ltd.

Flawless balance sheet with proven track record.

Market Insights

Community Narratives