Advertisement

3 Global Growth Companies With High Insider Ownership And Up To 27% Revenue Growth

Simply Wall St

Reviewed by Simply Wall St

In the current global market landscape, characterized by economic uncertainty and inflation concerns, investors are navigating a challenging environment where U.S. stocks have been pressured by trade policy uncertainties and persistent inflation. Despite these headwinds, growth companies with high insider ownership can offer unique advantages as they often align management interests with shareholders and demonstrate confidence in their long-term prospects.

Top 10 Growth Companies With High Insider Ownership Globally

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 23.3% | 26% |

| Arctech Solar Holding (SHSE:688408) | 37.9% | 24.7% |

| Pharma Mar (BME:PHM) | 11.8% | 40.8% |

| Vow (OB:VOW) | 13.1% | 111.2% |

| Laopu Gold (SEHK:6181) | 36.4% | 38.9% |

| Global Tax Free (KOSDAQ:A204620) | 20.8% | 35.1% |

| CD Projekt (WSE:CDR) | 29.7% | 36.8% |

| Elliptic Laboratories (OB:ELABS) | 22.6% | 88.2% |

| Nordic Halibut (OB:NOHAL) | 29.8% | 56.3% |

| Synspective (TSE:290A) | 13.2% | 44.5% |

Let's take a closer look at a couple of our picks from the screened companies.

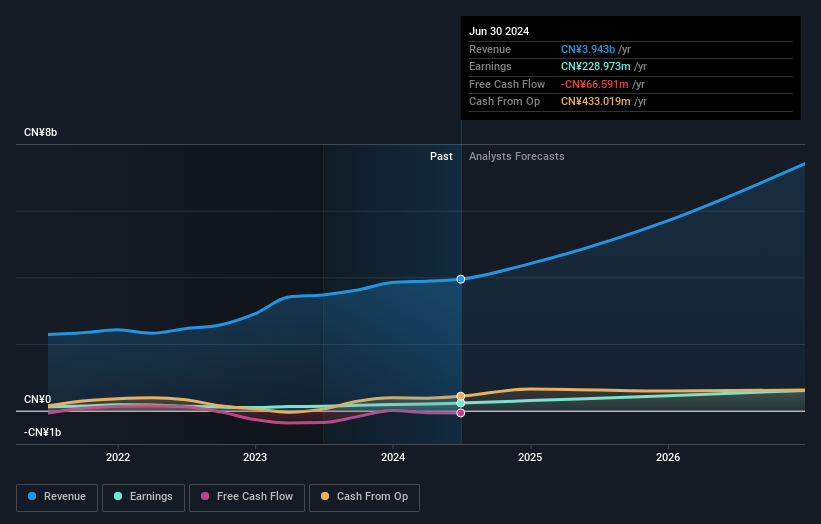

JiangSu Zhenjiang New Energy Equipment (SHSE:603507)

Simply Wall St Growth Rating: ★★★★★☆

Overview: JiangSu Zhenjiang New Energy Equipment Co., Ltd. operates in the renewable energy sector, focusing on the manufacturing of equipment for new energy applications, with a market cap of CN¥4.85 billion.

Operations: Unfortunately, the Business operations text provided does not contain specific revenue segment information for JiangSu Zhenjiang New Energy Equipment Co., Ltd.

Insider Ownership: 22.5%

Revenue Growth Forecast: 24.7% p.a.

JiangSu Zhenjiang New Energy Equipment is trading at a favorable price-to-earnings ratio of 24x, below the CN market average. Its revenue is expected to grow significantly at 24.7% annually, outpacing the broader CN market's growth rate. However, its debt coverage by operating cash flow remains a concern. While earnings are projected to rise substantially by 39.54% per year, the dividend yield of 1.03% isn't well-supported by free cash flows.

- Navigate through the intricacies of JiangSu Zhenjiang New Energy Equipment with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that JiangSu Zhenjiang New Energy Equipment's current price could be quite moderate.

3Peak (SHSE:688536)

Simply Wall St Growth Rating: ★★★★★☆

Overview: 3Peak Incorporated focuses on the research, development, and sale of analog integrated circuit products both in China and internationally, with a market capitalization of approximately CN¥16.11 billion.

Operations: The company's revenue is primarily derived from its operations in the Integrated Circuit Industry, amounting to CN¥1.22 billion.

Insider Ownership: 14.4%

Revenue Growth Forecast: 27.2% p.a.

3Peak exhibits strong growth potential with its forecasted revenue increase of 27.2% annually, surpassing the CN market's average growth. Despite high volatility in share price recently, it is expected to achieve profitability within three years, marking above-average market profit growth. However, its return on equity is projected to remain low at 5.9%. There has been no substantial insider trading activity over the past three months.

- Click to explore a detailed breakdown of our findings in 3Peak's earnings growth report.

- Our valuation report unveils the possibility 3Peak's shares may be trading at a premium.

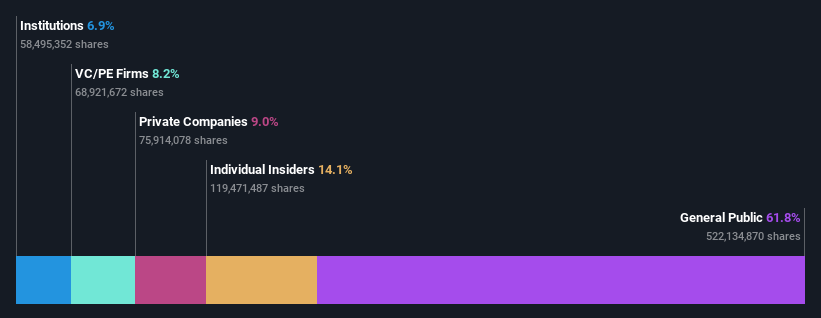

Toread Holdings Group (SZSE:300005)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Toread Holdings Group Co., Ltd. focuses on the research, development, operation, and sales of outdoor products in China with a market cap of CN¥7.25 billion.

Operations: Toread Holdings Group Co., Ltd. generates its revenue primarily through the research, development, and sales of outdoor products within the Chinese market.

Insider Ownership: 14.1%

Revenue Growth Forecast: 13.2% p.a.

Toread Holdings Group demonstrates growth potential with forecasted earnings growth of 25.4% annually, outpacing the CN market's average. Recent board changes may influence strategic direction, as Mao Zhimiao and Meng Xing assume new roles. Despite slower revenue growth at 13.2% per year compared to its earnings, it still surpasses the market's average revenue increase. However, projected return on equity remains low at 9.1%, and there is no recent significant insider trading activity noted.

- Take a closer look at Toread Holdings Group's potential here in our earnings growth report.

- Our valuation report here indicates Toread Holdings Group may be overvalued.

Seize The Opportunity

- Embark on your investment journey to our 903 Fast Growing Global Companies With High Insider Ownership selection here.

- Interested In Other Possibilities? The end of cancer? These 21 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Toread Holdings Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300005

Toread Holdings Group

Engages in the research, development, operation, and sales of outdoor products in China.

Excellent balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Quality Assets, Cautious Expansion and Commodity Super-cycle To Deliver Steady Revenue Growth

Fair Value US$20.44|5.0% undervalued

ST

Equity Analyst and Writer

Tullow Oil's Share Price Could Soar Up to 135% if Oil Holds at $70

Fair Value UK£0.45|63.8% undervalued

OI

Community Contributor