- China

- /

- Electrical

- /

- SHSE:603366

What Solareast Holdings Co., Ltd.'s (SHSE:603366) 206% Share Price Gain Is Not Telling You

Despite an already strong run, Solareast Holdings Co., Ltd. (SHSE:603366) shares have been powering on, with a gain of 206% in the last thirty days. The last month tops off a massive increase of 117% in the last year.

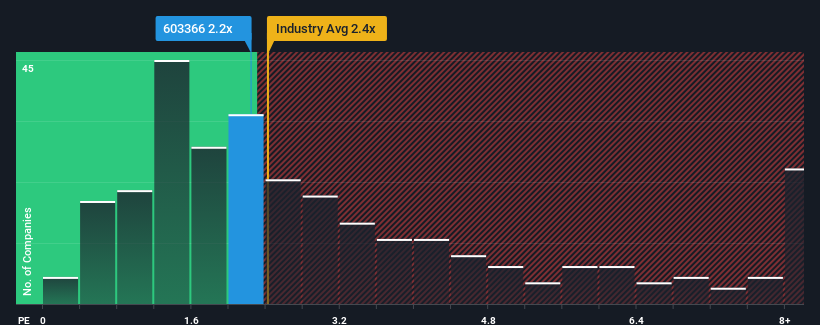

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Solareast Holdings' P/S ratio of 2.2x, since the median price-to-sales (or "P/S") ratio for the Electrical industry in China is also close to 2.4x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Solareast Holdings

How Solareast Holdings Has Been Performing

As an illustration, revenue has deteriorated at Solareast Holdings over the last year, which is not ideal at all. One possibility is that the P/S is moderate because investors think the company might still do enough to be in line with the broader industry in the near future. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Solareast Holdings will help you shine a light on its historical performance.Is There Some Revenue Growth Forecasted For Solareast Holdings?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Solareast Holdings' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 1.4% decrease to the company's top line. Regardless, revenue has managed to lift by a handy 14% in aggregate from three years ago, thanks to the earlier period of growth. So we can start by confirming that the company has generally done a good job of growing revenue over that time, even though it had some hiccups along the way.

Comparing the recent medium-term revenue trends against the industry's one-year growth forecast of 25% shows it's noticeably less attractive.

In light of this, it's curious that Solareast Holdings' P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than recent times would indicate and aren't willing to let go of their stock right now. They may be setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

What We Can Learn From Solareast Holdings' P/S?

Its shares have lifted substantially and now Solareast Holdings' P/S is back within range of the industry median. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

Our examination of Solareast Holdings revealed its poor three-year revenue trends aren't resulting in a lower P/S as per our expectations, given they look worse than current industry outlook. When we see weak revenue with slower than industry growth, we suspect the share price is at risk of declining, bringing the P/S back in line with expectations. If recent medium-term revenue trends continue, the probability of a share price decline will become quite substantial, placing shareholders at risk.

It is also worth noting that we have found 4 warning signs for Solareast Holdings that you need to take into consideration.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

If you're looking to trade Solareast Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603366

Solareast Holdings

Engages in the research and development, production, and sales of water heaters, kitchen appliances, clean energy heating, water purification, and other businesses in China and internationally.

Proven track record with adequate balance sheet.

Market Insights

Community Narratives