Sentiment Still Eluding Shandong Swan CottonIndustrial Machinery Stock Co.,Ltd. (SHSE:603029)

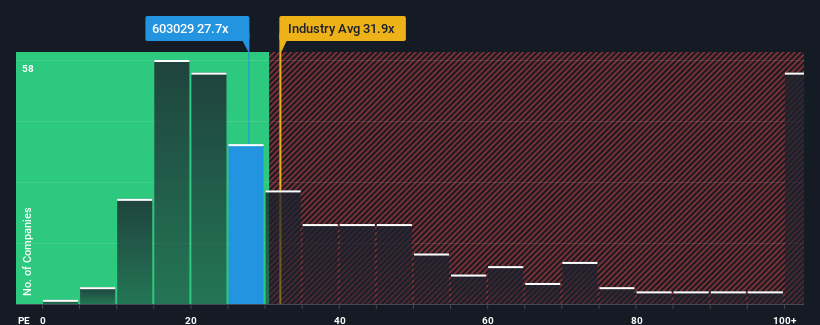

With a price-to-earnings (or "P/E") ratio of 27.7x Shandong Swan CottonIndustrial Machinery Stock Co.,Ltd. (SHSE:603029) may be sending bullish signals at the moment, given that almost half of all companies in China have P/E ratios greater than 34x and even P/E's higher than 65x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

It looks like earnings growth has deserted Shandong Swan CottonIndustrial Machinery StockLtd recently, which is not something to boast about. One possibility is that the P/E is low because investors think this benign earnings growth rate will likely underperform the broader market in the near future. If not, then existing shareholders may be feeling optimistic about the future direction of the share price.

Check out our latest analysis for Shandong Swan CottonIndustrial Machinery StockLtd

Does Growth Match The Low P/E?

Shandong Swan CottonIndustrial Machinery StockLtd's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Still, the latest three year period has seen an excellent 192% overall rise in EPS, in spite of its uninspiring short-term performance. Accordingly, shareholders would have probably welcomed those medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 36% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's peculiar that Shandong Swan CottonIndustrial Machinery StockLtd's P/E sits below the majority of other companies. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Shandong Swan CottonIndustrial Machinery StockLtd currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. There could be some major unobserved threats to earnings preventing the P/E ratio from matching this positive performance. It appears many are indeed anticipating earnings instability, because the persistence of these recent medium-term conditions would normally provide a boost to the share price.

You should always think about risks. Case in point, we've spotted 2 warning signs for Shandong Swan CottonIndustrial Machinery StockLtd you should be aware of.

You might be able to find a better investment than Shandong Swan CottonIndustrial Machinery StockLtd. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603029

Shandong Swan CottonIndustrial Machinery StockLtd

Shandong Swan CottonIndustrial Machinery Stock Co.,Ltd.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives