Discover Haitong Unitrust International Financial Leasing And 2 Other Asian Small Caps With Strong Potential

Reviewed by Simply Wall St

Amidst a backdrop of global economic uncertainty and fluctuating consumer confidence, the Asian markets continue to present unique opportunities for investors, particularly within the small-cap sector. As larger indices face headwinds from policy risks and trade tensions, discerning investors may find potential in smaller companies that exhibit strong fundamentals and resilience. Identifying such stocks often involves looking for those with solid financial health, innovative business models, or strategic positioning in growing industries.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| NOROO PAINT & COATINGS | 12.38% | 4.96% | 8.97% | ★★★★★★ |

| Central Forest Group | NA | 5.93% | 20.71% | ★★★★★★ |

| Tianjin Port Holdings | 18.46% | -3.73% | 11.17% | ★★★★★★ |

| Kyungdong Invest | 6.73% | 1.27% | 7.28% | ★★★★★★ |

| Namuga | 14.66% | -1.45% | 33.57% | ★★★★★★ |

| Neosem | 2.52% | 27.62% | 27.36% | ★★★★★★ |

| Creative & Innovative System | 2.86% | 55.78% | 90.01% | ★★★★★☆ |

| Daewon Cable | 24.09% | 8.60% | 57.94% | ★★★★★☆ |

| ASTERASYSLtd | 6.62% | 16.45% | 6.42% | ★★★★★☆ |

| MNtech | 65.44% | 16.96% | -17.92% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

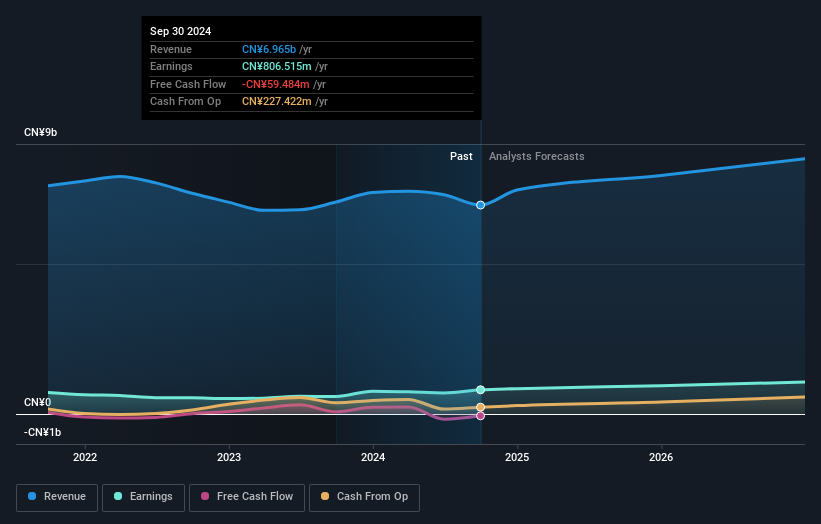

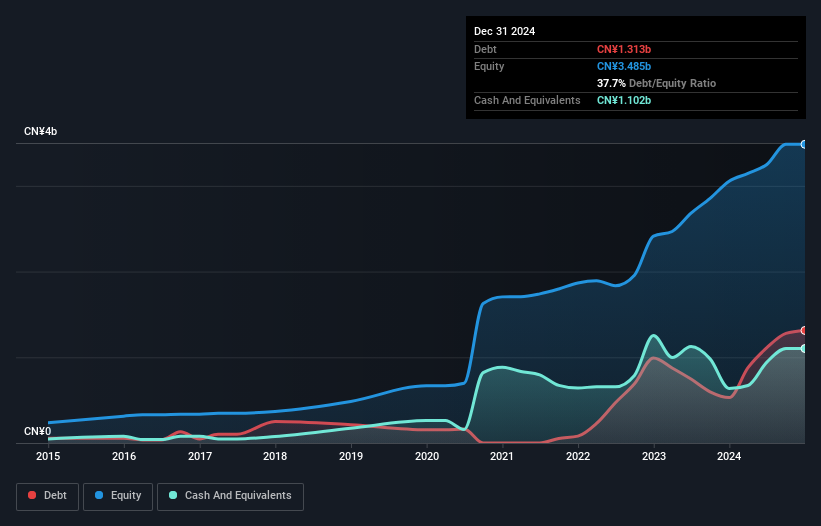

Haitong Unitrust International Financial Leasing (SEHK:1905)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Haitong Unitrust International Financial Leasing Co., Ltd. operates as a financial leasing company in the People’s Republic of China, with a market capitalization of HK$7.49 billion.

Operations: The primary revenue stream for Haitong Unitrust comes from its financial services segment, generating CN¥3.68 billion. The company's net profit margin reflects its profitability dynamics in the competitive leasing market of China.

Haitong Unitrust International Financial Leasing, a smaller player in the financial leasing sector, has shown resilience with its earnings growing by 0.5% over the past year, outpacing the industry average of -6.6%. The company trades at 63.4% below its estimated fair value, suggesting potential undervaluation. Over five years, it reduced its debt to equity ratio from 403.4% to 205.1%, although a net debt to equity ratio of 160% remains high. Recent changes include appointing Deloitte Touche Tohmatsu as auditors for both international and domestic operations, which may enhance financial transparency and credibility moving forward.

Guangzhou Guangri StockLtd (SHSE:600894)

Simply Wall St Value Rating: ★★★★★☆

Overview: Guangzhou Guangri Stock Co., Ltd. is a Chinese company that specializes in the manufacturing and sale of elevators and related parts, with a market capitalization of CN¥10.45 billion.

Operations: Guangri Stock's primary revenue stream is from manufacturing and selling elevators and related parts. The company has a market capitalization of CN¥10.45 billion.

Guangzhou Guangri Stock Ltd. has been making waves with its earnings growth of 38.1% over the past year, outpacing the broader Machinery industry, which saw a 0.06% increase. The company's debt to equity ratio impressively decreased from 1.2% to just 0.2% over five years, signaling strong financial management and stability in a competitive market environment. Trading at approximately 20.8% below estimated fair value, it presents an attractive opportunity for investors seeking value in this sector. Furthermore, recent share buybacks totaling CNY161 million underscore confidence in its future prospects and commitment to enhancing shareholder value.

Shanghai GenTech (SHSE:688596)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shanghai GenTech Co., Ltd. offers process critical system solutions to China's hi-tech and advanced manufacturing sectors, with a market cap of CN¥11.20 billion.

Operations: Shanghai GenTech generates revenue primarily from providing system solutions to hi-tech and advanced manufacturing industries in China. The company's gross profit margin is 45%, reflecting its pricing strategy and cost management.

Shanghai GenTech has shown impressive growth, with earnings climbing 31.6% over the past year, outpacing the Semiconductor industry's 15.5%. The company reported a net income increase to CNY 528 million from CNY 401 million last year, while sales rose to CNY 5.47 billion from CNY 3.83 billion. Trading at a price-to-earnings ratio of 21.2x, it offers good value compared to the CN market's average of 37.2x. Despite an increased debt-to-equity ratio from 27% to nearly 37% over five years, its interest payments are comfortably covered by EBIT at a robust multiple of approximately 44 times.

- Navigate through the intricacies of Shanghai GenTech with our comprehensive health report here.

Explore historical data to track Shanghai GenTech's performance over time in our Past section.

Seize The Opportunity

- Click here to access our complete index of 2576 Asian Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Guangzhou Guangri StockLtd, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:600894

Guangzhou Guangri StockLtd

Manufactures and sells elevators and related parts in China.

Proven track record with adequate balance sheet.

Market Insights

Community Narratives