- China

- /

- Electrical

- /

- SHSE:600516

Market Participants Recognise FangDa Carbon New Material Co.,Ltd's (SHSE:600516) Earnings Pushing Shares 37% Higher

FangDa Carbon New Material Co.,Ltd (SHSE:600516) shareholders would be excited to see that the share price has had a great month, posting a 37% gain and recovering from prior weakness. The bad news is that even after the stocks recovery in the last 30 days, shareholders are still underwater by about 8.0% over the last year.

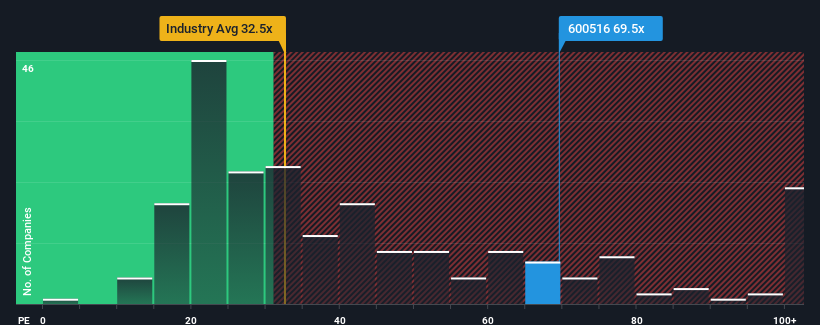

After such a large jump in price, FangDa Carbon New MaterialLtd may be sending very bearish signals at the moment with a price-to-earnings (or "P/E") ratio of 69.5x, since almost half of all companies in China have P/E ratios under 33x and even P/E's lower than 20x are not unusual. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

With earnings that are retreating more than the market's of late, FangDa Carbon New MaterialLtd has been very sluggish. It might be that many expect the dismal earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

View our latest analysis for FangDa Carbon New MaterialLtd

Is There Enough Growth For FangDa Carbon New MaterialLtd?

In order to justify its P/E ratio, FangDa Carbon New MaterialLtd would need to produce outstanding growth well in excess of the market.

Retrospectively, the last year delivered a frustrating 60% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 64% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing earnings over that time.

Shifting to the future, estimates from the four analysts covering the company suggest earnings should grow by 31% per annum over the next three years. That's shaping up to be materially higher than the 19% each year growth forecast for the broader market.

In light of this, it's understandable that FangDa Carbon New MaterialLtd's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Bottom Line On FangDa Carbon New MaterialLtd's P/E

FangDa Carbon New MaterialLtd's P/E is flying high just like its stock has during the last month. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that FangDa Carbon New MaterialLtd maintains its high P/E on the strength of its forecast growth being higher than the wider market, as expected. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 2 warning signs for FangDa Carbon New MaterialLtd you should know about.

If these risks are making you reconsider your opinion on FangDa Carbon New MaterialLtd, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:600516

FangDa Carbon New MaterialLtd

Engages in the research and development, production, supply, and sale of carbon products in China and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Community Narratives