Advertisement

Zhejiang Taotao Vehicles Co., Ltd. (SZSE:301345) Looks Inexpensive After Falling 28% But Perhaps Not Attractive Enough

Zhejiang Taotao Vehicles Co., Ltd. (SZSE:301345) shareholders won't be pleased to see that the share price has had a very rough month, dropping 28% and undoing the prior period's positive performance. Indeed, the recent drop has reduced its annual gain to a relatively sedate 2.8% over the last twelve months.

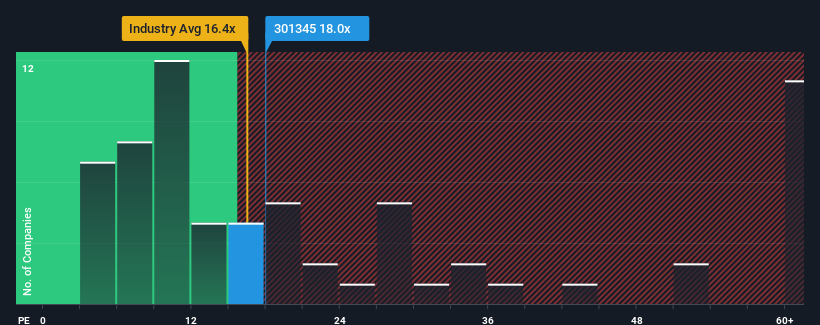

In spite of the heavy fall in price, given about half the companies in China have price-to-earnings ratios (or "P/E's") above 29x, you may still consider Zhejiang Taotao Vehicles as an attractive investment with its 18x P/E ratio. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

Zhejiang Taotao Vehicles certainly has been doing a good job lately as it's been growing earnings more than most other companies. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Zhejiang Taotao Vehicles

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Zhejiang Taotao Vehicles' to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 4.8% last year. However, due to its less than impressive performance prior to this period, EPS growth is practically non-existent over the last three years overall. So it appears to us that the company has had a mixed result in terms of growing earnings over that time.

Turning to the outlook, the next three years should generate growth of 21% each year as estimated by the three analysts watching the company. Meanwhile, the rest of the market is forecast to expand by 25% per year, which is noticeably more attractive.

In light of this, it's understandable that Zhejiang Taotao Vehicles' P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Zhejiang Taotao Vehicles' recently weak share price has pulled its P/E below most other companies. We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Zhejiang Taotao Vehicles' analyst forecasts revealed that its inferior earnings outlook is contributing to its low P/E. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 2 warning signs for Zhejiang Taotao Vehicles that you should be aware of.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Taotao Vehicles might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:301345

Zhejiang Taotao Vehicles

Engages in the research and development, production, and sale of motorcycles, electric vehicles, and ATVs in China.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor