Advertisement

- China

- /

- Auto Components

- /

- SZSE:002126

Asian Market Insights: Three Stocks That May Be Trading Below Fair Value

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate through a landscape marked by trade uncertainties and policy shifts, the Asian market has shown resilience with some indices advancing amidst expectations of economic stimulus. In this context, identifying stocks that may be trading below their fair value can present opportunities for investors seeking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Auras Technology (TPEX:3324) | NT$454.50 | NT$903.14 | 49.7% |

| Pegasus (TSE:6262) | ¥465.00 | ¥920.79 | 49.5% |

| RACCOON HOLDINGS (TSE:3031) | ¥881.00 | ¥1722.56 | 48.9% |

| Members (TSE:2130) | ¥1125.00 | ¥2244.23 | 49.9% |

| Rakus (TSE:3923) | ¥2189.00 | ¥4351.81 | 49.7% |

| AeroEdge (TSE:7409) | ¥1897.00 | ¥3725.41 | 49.1% |

| Rise Consulting Group (TSE:9168) | ¥930.00 | ¥1825.84 | 49.1% |

| Aozora Bank (TSE:8304) | ¥1855.50 | ¥3690.71 | 49.7% |

| World Fitness Services (TWSE:2762) | NT$79.90 | NT$156.18 | 48.8% |

| SAMG Entertainment (KOSDAQ:A419530) | ₩36100.00 | ₩70589.14 | 48.9% |

We're going to check out a few of the best picks from our screener tool.

Xiamen Amoytop Biotech (SHSE:688278)

Overview: Xiamen Amoytop Biotech Co., Ltd. focuses on the research, development, production, and sale of recombinant protein drugs in China with a market cap of CN¥32.22 billion.

Operations: The company generates revenue through its activities in the research, development, production, and sale of recombinant protein drugs within China.

Estimated Discount To Fair Value: 46%

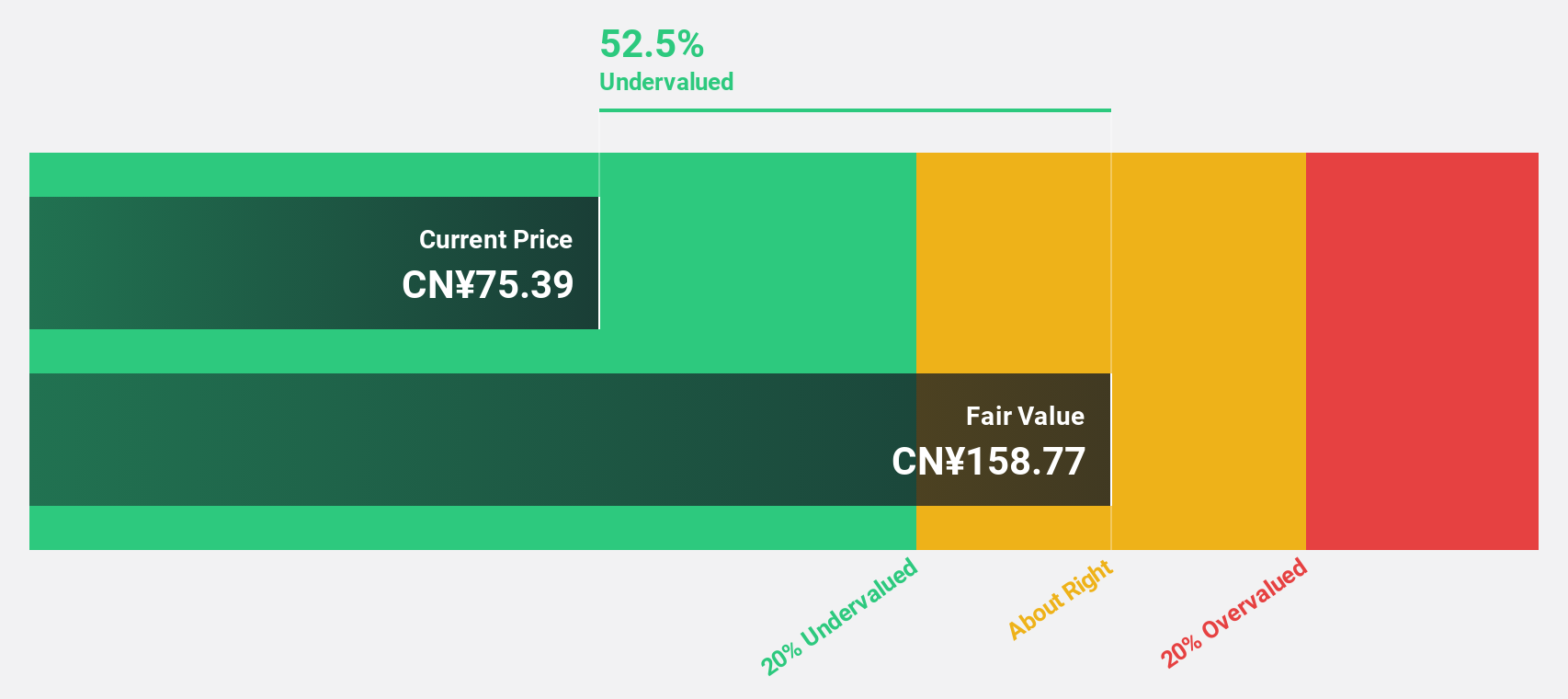

Xiamen Amoytop Biotech appears undervalued based on cash flows, trading at CN¥79.2, significantly below its estimated fair value of CN¥146.62. The company reported strong financial performance with a net income of CN¥827.6 million for 2024, up from the previous year. Earnings and revenue are forecast to grow rapidly at rates exceeding the Chinese market averages, supported by high-quality earnings and robust return on equity projections reaching 31.9%.

- Insights from our recent growth report point to a promising forecast for Xiamen Amoytop Biotech's business outlook.

- Unlock comprehensive insights into our analysis of Xiamen Amoytop Biotech stock in this financial health report.

Zhejiang Yinlun MachineryLtd (SZSE:002126)

Overview: Zhejiang Yinlun Machinery Co., Ltd. focuses on the research, development, manufacturing, and sale of thermal management and exhaust gas post-treatment products, with a market cap of CN¥20.68 billion.

Operations: The company generates revenue through its involvement in the research, development, manufacturing, and sale of thermal management and exhaust gas post-treatment products.

Estimated Discount To Fair Value: 36%

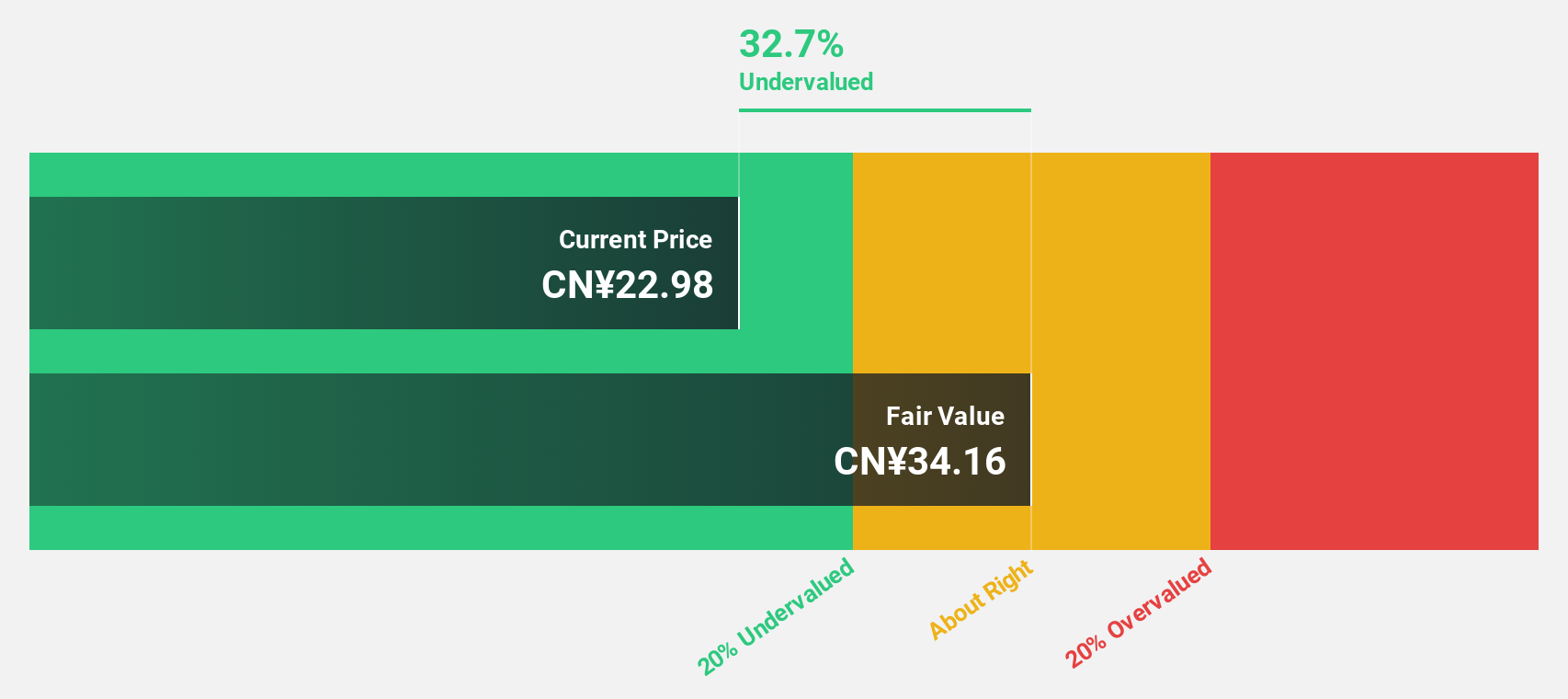

Zhejiang Yinlun Machinery is trading at CN¥24.95, well below its estimated fair value of CN¥38.99, highlighting its undervaluation based on cash flows. The company reported a net income of CNY 783.53 million for 2024, up from CNY 612.14 million the previous year, with earnings expected to grow significantly over the next three years at a rate surpassing market averages. Despite high share price volatility recently, it offers good relative value within its industry context.

- The analysis detailed in our Zhejiang Yinlun MachineryLtd growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of Zhejiang Yinlun MachineryLtd.

Anhui Jinhe IndustrialLtd (SZSE:002597)

Overview: Anhui Jinhe Industrial Co., Ltd. operates in the chemicals sector in China and has a market cap of CN¥13.58 billion.

Operations: The company's revenue segments include Trade at CN¥19.04 million, Food Manufacturing at CN¥2.75 billion, and Basic Chemical Industry at CN¥2.05 billion.

Estimated Discount To Fair Value: 19.6%

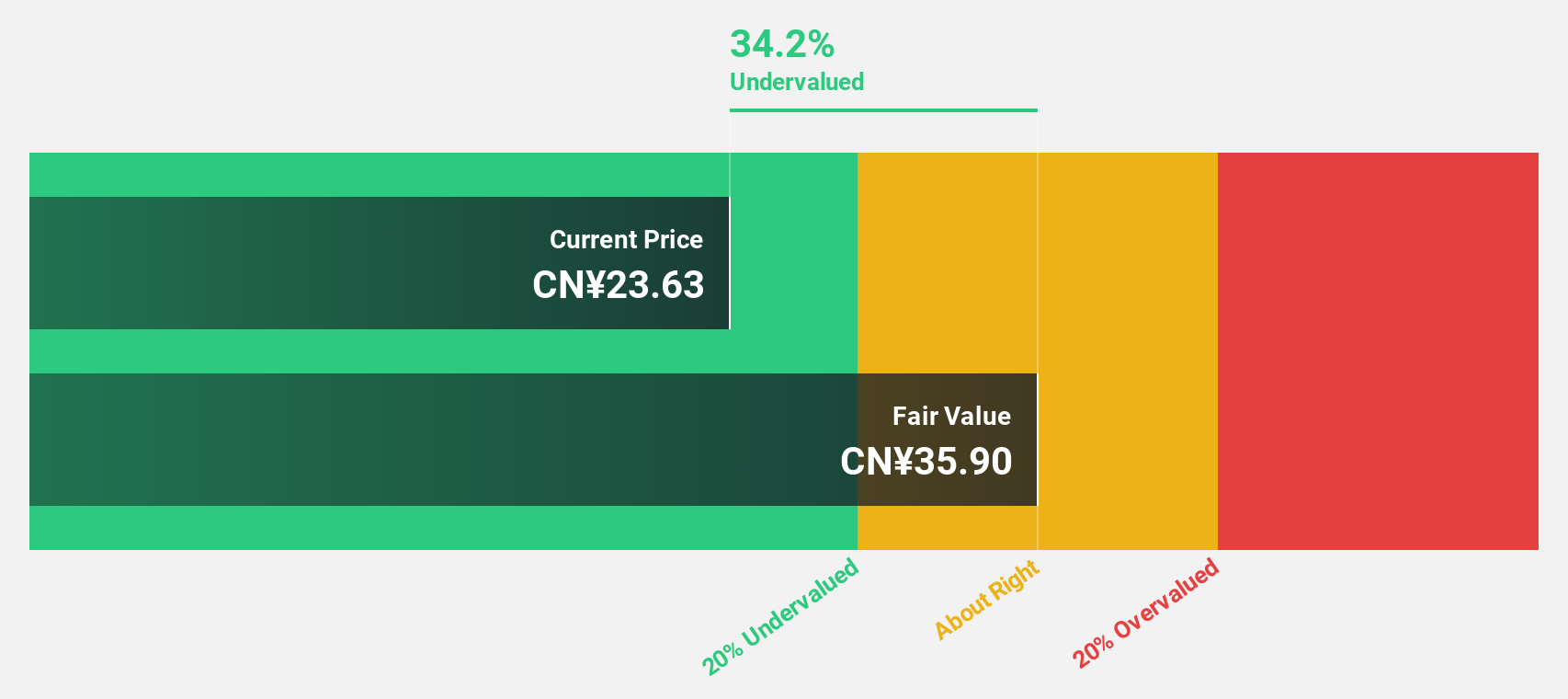

Anhui Jinhe Industrial is trading at CN¥24.74, below its fair value estimate of CN¥30.76, suggesting undervaluation based on cash flows. While revenue is forecast to grow at 15% annually, earnings are expected to increase significantly over the next three years, outpacing market averages. However, current dividends aren't well-covered by free cash flows and the return on equity remains modestly low at a projected 16% in three years.

- The growth report we've compiled suggests that Anhui Jinhe IndustrialLtd's future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in Anhui Jinhe IndustrialLtd's balance sheet health report.

Make It Happen

- Investigate our full lineup of 272 Undervalued Asian Stocks Based On Cash Flows right here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Yinlun MachineryLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:002126

Zhejiang Yinlun MachineryLtd

Engages in the research and development, manufacturing, and sale of various thermal management and exhaust gas post-treatment products.

Very undervalued with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor