Advertisement

- China

- /

- Auto Components

- /

- SZSE:002085

Zhejiang Wanfeng Auto Wheel Co., Ltd. (SZSE:002085) Shares Fly 35% But Investors Aren't Buying For Growth

The Zhejiang Wanfeng Auto Wheel Co., Ltd. (SZSE:002085) share price has done very well over the last month, posting an excellent gain of 35%. Notwithstanding the latest gain, the annual share price return of 9.5% isn't as impressive.

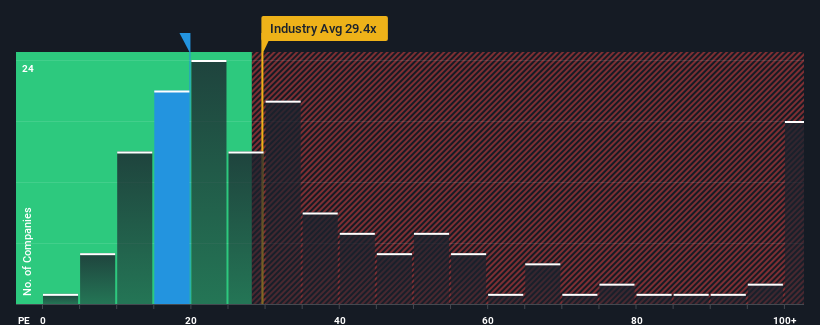

Although its price has surged higher, Zhejiang Wanfeng Auto Wheel may still be sending bullish signals at the moment with its price-to-earnings (or "P/E") ratio of 19.7x, since almost half of all companies in China have P/E ratios greater than 29x and even P/E's higher than 53x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/E.

Zhejiang Wanfeng Auto Wheel has been doing a good job lately as it's been growing earnings at a solid pace. It might be that many expect the respectable earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

See our latest analysis for Zhejiang Wanfeng Auto Wheel

Does Growth Match The Low P/E?

There's an inherent assumption that a company should underperform the market for P/E ratios like Zhejiang Wanfeng Auto Wheel's to be considered reasonable.

Taking a look back first, we see that the company managed to grow earnings per share by a handy 12% last year. The latest three year period has also seen a 28% overall rise in EPS, aided somewhat by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of earnings growth.

This is in contrast to the rest of the market, which is expected to grow by 41% over the next year, materially higher than the company's recent medium-term annualised growth rates.

In light of this, it's understandable that Zhejiang Wanfeng Auto Wheel's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on to something they believe will continue to trail the bourse.

The Key Takeaway

Zhejiang Wanfeng Auto Wheel's stock might have been given a solid boost, but its P/E certainly hasn't reached any great heights. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Zhejiang Wanfeng Auto Wheel maintains its low P/E on the weakness of its recent three-year growth being lower than the wider market forecast, as expected. At this stage investors feel the potential for an improvement in earnings isn't great enough to justify a higher P/E ratio. If recent medium-term earnings trends continue, it's hard to see the share price rising strongly in the near future under these circumstances.

Plus, you should also learn about these 4 warning signs we've spotted with Zhejiang Wanfeng Auto Wheel (including 1 which makes us a bit uncomfortable).

If you're unsure about the strength of Zhejiang Wanfeng Auto Wheel's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Wanfeng Auto Wheel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002085

Zhejiang Wanfeng Auto Wheel

Engages in the manufacture and sale of automotive parts and aircrafts in China.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor