- Chile

- /

- Healthcare Services

- /

- SNSE:LAS CONDES

Does Clínica Las Condes (SNSE:LAS CONDES) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Clínica Las Condes S.A. (SNSE:LAS CONDES) makes use of debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Clínica Las Condes

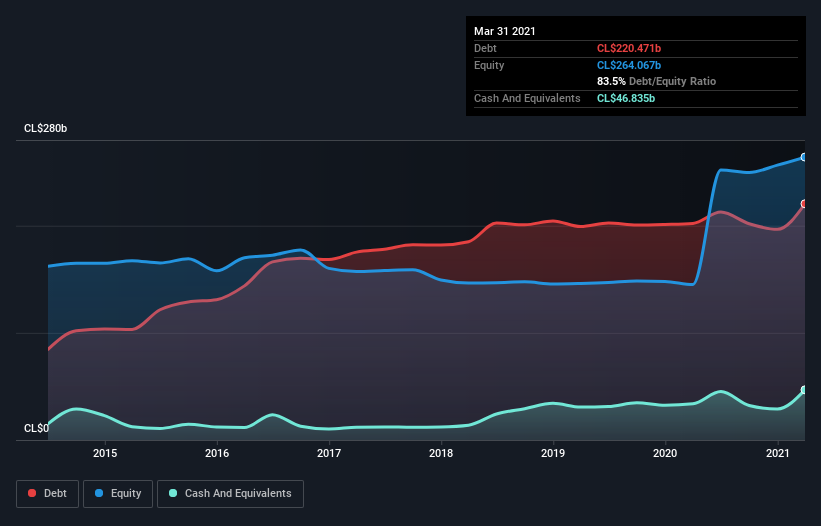

How Much Debt Does Clínica Las Condes Carry?

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Clínica Las Condes had CL$220.5b of debt, an increase on CL$202.2b, over one year. However, it also had CL$46.8b in cash, and so its net debt is CL$173.6b.

How Strong Is Clínica Las Condes' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Clínica Las Condes had liabilities of CL$83.4b due within 12 months and liabilities of CL$255.8b due beyond that. On the other hand, it had cash of CL$46.8b and CL$133.7b worth of receivables due within a year. So its liabilities total CL$158.6b more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of CL$237.0b, so it does suggest shareholders should keep an eye on Clínica Las Condes' use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Clínica Las Condes has a rather high debt to EBITDA ratio of 5.0 which suggests a meaningful debt load. However, its interest coverage of 3.3 is reasonably strong, which is a good sign. The good news is that Clínica Las Condes grew its EBIT a smooth 34% over the last twelve months. Like the milk of human kindness that sort of growth increases resilience, making the company more capable of managing debt. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Clínica Las Condes will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Clínica Las Condes produced sturdy free cash flow equating to 61% of its EBIT, about what we'd expect. This free cash flow puts the company in a good position to pay down debt, when appropriate.

Our View

When it comes to the balance sheet, the standout positive for Clínica Las Condes was the fact that it seems able to grow its EBIT confidently. But the other factors we noted above weren't so encouraging. To be specific, it seems about as good at managing its debt, based on its EBITDA, as wet socks are at keeping your feet warm. It's also worth noting that Clínica Las Condes is in the Healthcare industry, which is often considered to be quite defensive. When we consider all the elements mentioned above, it seems to us that Clínica Las Condes is managing its debt quite well. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with Clínica Las Condes (including 2 which are potentially serious) .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SNSE:LAS CONDES

Low and slightly overvalued.

Market Insights

Community Narratives