Advertisement

- Chile

- /

- Capital Markets

- /

- SNSE:TRICAHUE

Inversiones Tricahue (SNSE:TRICAHUE) Is Paying Out Less In Dividends Than Last Year

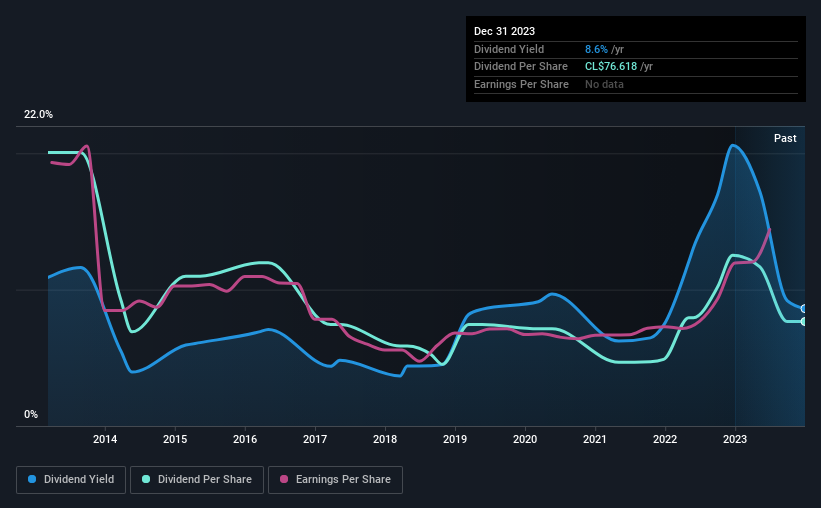

Inversiones Tricahue S.A.'s (SNSE:TRICAHUE) dividend is being reduced from last year's payment covering the same period to CLP27.10 on the 22nd of January. This means that the dividend yield is 8.6%, which is a bit low when comparing to other companies in the industry.

Check out our latest analysis for Inversiones Tricahue

Inversiones Tricahue's Dividend Is Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. Before this announcement, Inversiones Tricahue was paying out 78% of earnings, but a comparatively small 49% of free cash flows. This leaves plenty of cash for reinvestment into the business.

If the trend of the last few years continues, EPS will grow by 20.1% over the next 12 months. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 69% which brings it into quite a comfortable range.

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The dividend has gone from an annual total of CLP200.60 in 2013 to the most recent total annual payment of CLP76.62. This works out to be a decline of approximately 9.2% per year over that time. Declining dividends isn't generally what we look for as they can indicate that the company is running into some challenges.

Dividend Growth Could Be Constrained

Given that dividend payments have been shrinking like a glacier in a warming world, we need to check if there are some bright spots on the horizon. It's encouraging to see that Inversiones Tricahue has been growing its earnings per share at 20% a year over the past five years. Fast growing earnings are great, but this can rarely be sustained without some reinvestment into the business, which Inversiones Tricahue hasn't been doing.

In Summary

In summary, dividends being cut isn't ideal, however it can bring the payment into a more sustainable range. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. This company is not in the top tier of income providing stocks.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 2 warning signs for Inversiones Tricahue that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SNSE:TRICAHUE

Excellent balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 86.87|32.1% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|34.7% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|29.9% undervalued

EV

Community Contributor