Banco de Crédito e Inversiones' (SNSE:BCI) Shareholders Will Receive A Smaller Dividend Than Last Year

Banco de Crédito e Inversiones' (SNSE:BCI) dividend is being reduced from last year's payment covering the same period to CLP1000.00 on the 9th of April. Based on this payment, the dividend yield will be 4.7%, which is lower than the average for the industry.

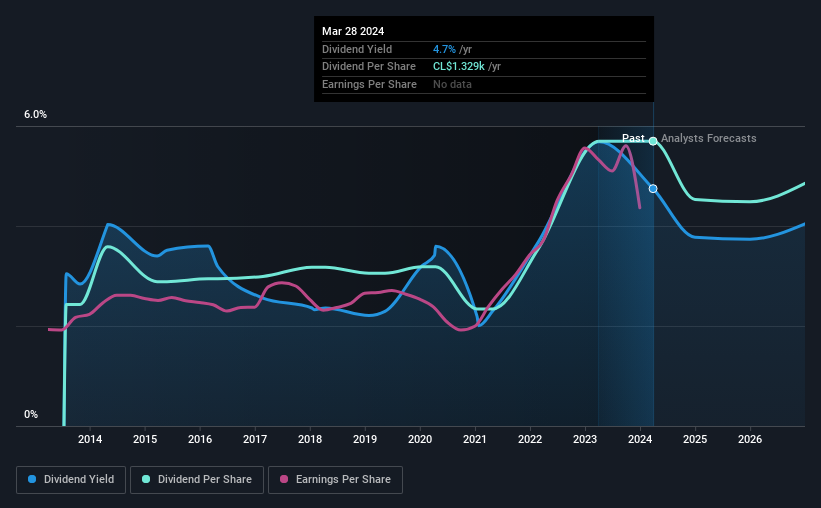

View our latest analysis for Banco de Crédito e Inversiones

Banco de Crédito e Inversiones' Earnings Will Easily Cover The Distributions

If it is predictable over a long period, even low dividend yields can be attractive.

Having distributed dividends for at least 10 years, Banco de Crédito e Inversiones has a long history of paying out a part of its earnings to shareholders. Taking data from its last earnings report, calculating for the company's payout ratio shows 28%, which means that Banco de Crédito e Inversiones would be able to pay its last dividend without pressure on the balance sheet.

The next 3 years are set to see EPS grow by 4.8%. The future payout ratio could be 31% over that time period, according to analyst estimates, which is a good look for the future of the dividend.

Dividend Volatility

The company has a long dividend track record, but it doesn't look great with cuts in the past. Since 2014, the dividend has gone from CLP567.45 total annually to CLP1329.16. This means that it has been growing its distributions at 8.9% per annum over that time. We like to see dividends have grown at a reasonable rate, but with at least one substantial cut in the payments, we're not certain this dividend stock would be ideal for someone intending to live on the income.

The Dividend Has Growth Potential

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. We are encouraged to see that Banco de Crédito e Inversiones has grown earnings per share at 7.1% per year over the past five years. Growth in EPS bodes well for the dividend, as does the low payout ratio that the company is currently reporting.

An additional note is that the company has been raising capital by issuing stock equal to 15% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

In Summary

Even though the dividend was cut this year, we think Banco de Crédito e Inversiones has the ability to make consistent payments in the future. While the payout ratios are a good sign, we are less enthusiastic about the company's dividend record. This looks like it could be a good dividend stock going forward, but we would note that the payout ratio has been at higher levels in the past so it could happen again.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've picked out 2 warning signs for Banco de Crédito e Inversiones that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Banco de Crédito e Inversiones might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SNSE:BCI

Banco de Crédito e Inversiones

Provides various banking products and services in Chile, United States, and Peru.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives