Stock Analysis

- Switzerland

- /

- Software

- /

- SWX:TEMN

High Insider Ownership Growth Stocks On SIX Swiss Exchange May 2024

Reviewed by Simply Wall St

Amid a backdrop of recent profit-taking and concerns over rising interest rates highlighted by the U.K.'s inflation data, the Swiss market has shown signs of volatility. As investors navigate these uncertain waters, stocks with high insider ownership in growth companies on the SIX Swiss Exchange may offer a unique appeal, potentially indicating strong confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In Switzerland

| Name | Insider Ownership | Earnings Growth |

| Stadler Rail (SWX:SRAIL) | 14.5% | 23.4% |

| VAT Group (SWX:VACN) | 10.2% | 21.2% |

| Straumann Holding (SWX:STMN) | 32.7% | 21% |

| Swissquote Group Holding (SWX:SQN) | 11.4% | 14.3% |

| Temenos (SWX:TEMN) | 17.4% | 14.7% |

| LEM Holding (SWX:LEHN) | 34.5% | 9.9% |

| Sonova Holding (SWX:SOON) | 17.7% | 10.4% |

| Arbonia (SWX:ARBN) | 28.8% | 80% |

| SHL Telemedicine (SWX:SHLTN) | 17.9% | 96.2% |

| Sensirion Holding (SWX:SENS) | 20.7% | 78.8% |

We'll examine a selection from our screener results.

INFICON Holding (SWX:IFCN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: INFICON Holding AG specializes in developing instruments for gas analysis, measurement, and control, operating both in Switzerland and globally, with a market capitalization of approximately CHF 3.48 billion.

Operations: The company's revenue primarily stems from its global instrumentation segment for gas analysis, measurement, and control, generating $673.71 million.

Insider Ownership: 10.3%

INFICON Holding AG, a Swiss company with high insider ownership, shows promising growth metrics. The company's revenue and earnings are forecasted to grow at 7.2% and 9.85% per year respectively, outpacing the Swiss market averages of 4.3% and 8.1%. This performance is bolstered by a strong projected return on equity of 27.6%. However, recent financial results highlight substantial growth with last year's sales reaching US$673.71 million and net income at US$105.68 million, marking significant year-over-year increases.

- Take a closer look at INFICON Holding's potential here in our earnings growth report.

- Our comprehensive valuation report raises the possibility that INFICON Holding is priced higher than what may be justified by its financials.

Sensirion Holding (SWX:SENS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sensirion Holding AG operates globally, specializing in the development, production, sale, and servicing of sensor systems, modules, and components with a market capitalization of approximately CHF 1.16 billion.

Operations: The company generates CHF 233.17 million from its sensor systems, modules, and components segment.

Insider Ownership: 20.7%

Sensirion Holding AG, despite a challenging financial year with a net loss of CHF 6.58 million from sales of CHF 233.17 million, is positioned for recovery with expected revenue growth outpacing the Swiss market average. The company's focus has shifted towards methane emission monitoring, aiming to leverage its technological expertise in environmental sensing. Forecasted earnings growth is robust at 78.82% annually, although current profitability is delayed, with positive returns anticipated within three years amidst high share price volatility.

- Click to explore a detailed breakdown of our findings in Sensirion Holding's earnings growth report.

- Our valuation report here indicates Sensirion Holding may be overvalued.

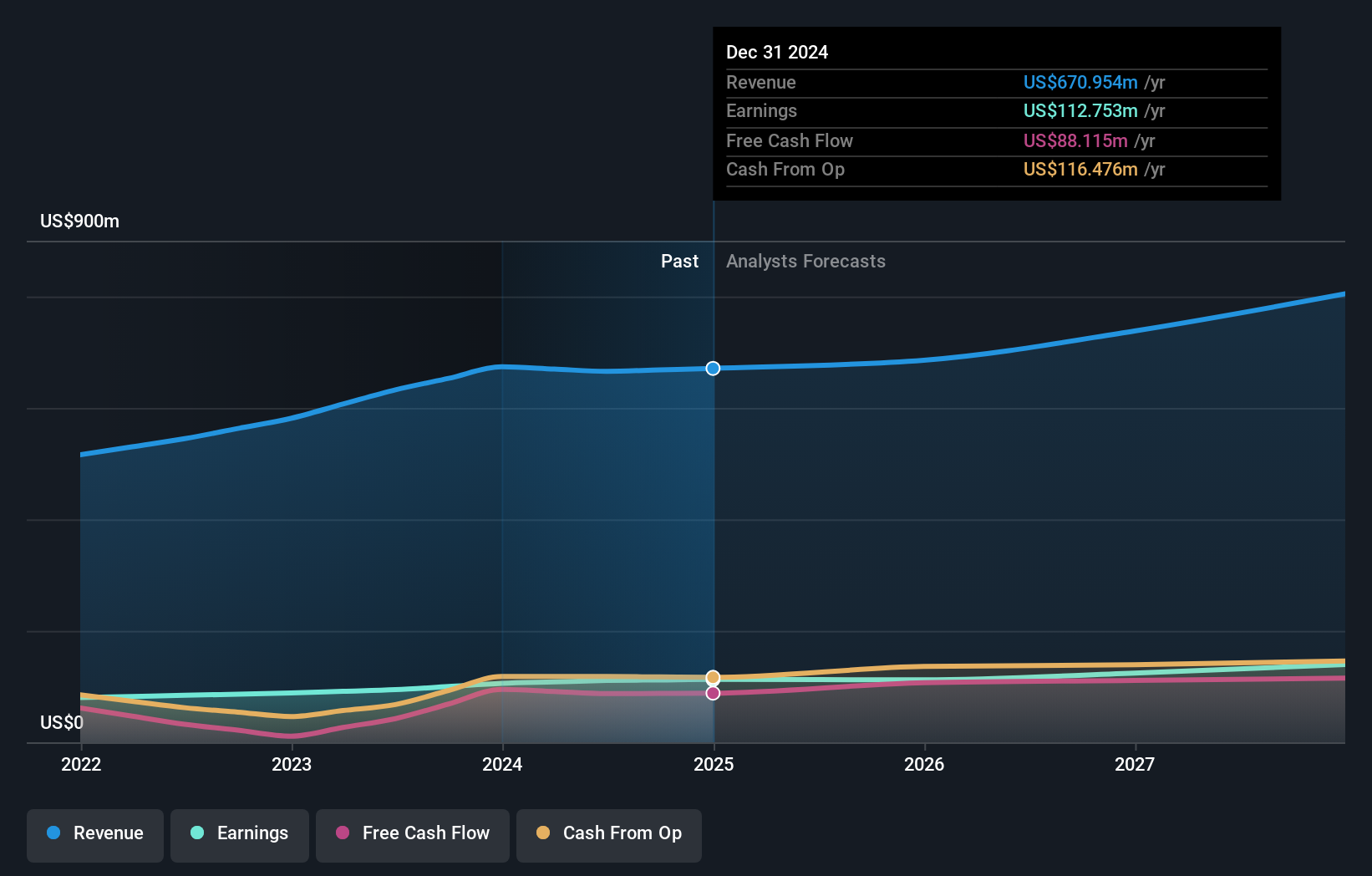

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG is a global provider of integrated banking software systems to financial institutions, with a market capitalization of CHF 4.20 billion.

Operations: The company generates its revenue by selling integrated banking software systems to financial institutions globally.

Insider Ownership: 17.4%

Temenos, trading at 31.3% below its estimated fair value, shows promising growth with earnings expected to increase by 14.7% annually, outperforming the Swiss market's 8.1%. Although its revenue growth is moderate at 7.7% per year, it remains above the market average of 4.3%. The company maintains a high return on equity forecast at 26%, despite a volatile share price and substantial debt levels. Recent advancements include significant efficiency improvements in its cloud-native banking platform and a new client acquisition with PC Financial® for expanded Canadian operations.

- Navigate through the intricacies of Temenos with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Temenos' shares may be trading at a discount.

Seize The Opportunity

- Dive into all 17 of the Fast Growing SIX Swiss Exchange Companies With High Insider Ownership we have identified here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're helping make it simple.

Find out whether Temenos is potentially over or undervalued by checking out our comprehensive analysis, which includes fair value estimates, risks and warnings, dividends, insider transactions and financial health.

View the Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:TEMN

Temenos

Develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide.

Reasonable growth potential with proven track record and pays a dividend.