- Switzerland

- /

- Real Estate

- /

- SWX:EPIC

EPIC Suisse (SWX:EPIC): Valuation Check After CHF 70m Follow-On Equity Offering

Reviewed by Simply Wall St

EPIC Suisse (SWX:EPIC) has just raised CHF 70 million through a follow on equity offering at CHF 80 per share, a move that directly affects both its growth options and shareholder dilution.

See our latest analysis for EPIC Suisse.

The fresh capital raise comes on the back of a steady share price return so far this year and a much stronger 1 year total shareholder return of 11.57 percent, suggesting confidence in EPIC Suisse’s long term real estate strategy.

If this equity deal has you rethinking where growth and conviction might show up next, it could be worth exploring fast growing stocks with high insider ownership for other ideas with aligned management incentives.

With the share price edging above the offer level and fundamentals still improving, the key question now is whether EPIC Suisse trades at a discount to its long term prospects or if the market already prices in that future growth.

Price-to-Earnings of 15.8x: Is it justified?

On a trailing basis EPIC Suisse trades at a price to earnings ratio of 15.8 times, a level that looks slightly expensive relative to close peers and the wider European real estate group.

The price to earnings ratio compares the current share price to the company’s earnings per share, offering a shorthand view of how much investors are paying for each unit of profit. For a real estate owner and developer with moderate forecast earnings growth of about 9.9 percent per year and a recent boost from one off gains, a richer multiple usually signals that the market expects earnings to remain resilient and largely repeatable once those non recurring items fade.

Relative comparisons underline that premium. EPIC Suisse changes hands at 15.8 times earnings, higher than both the European real estate industry average of 14.4 times and the immediate peer group on 13.7 times, yet still below the broader Swiss market multiple of 20.2 times. Our fair ratio work points in the opposite direction however, indicating that a multiple closer to 21.4 times would be justified if profits track current expectations, which leaves room for the valuation to migrate higher over time even after the recent equity raise.

Explore the SWS fair ratio for EPIC Suisse

Result: Price-to-Earnings of 15.8x (ABOUT RIGHT)

However, sustained rate pressures or weaker tenant demand could squeeze rental yields, undermining earnings resilience and limiting any further upside from today’s valuation.

Find out about the key risks to this EPIC Suisse narrative.

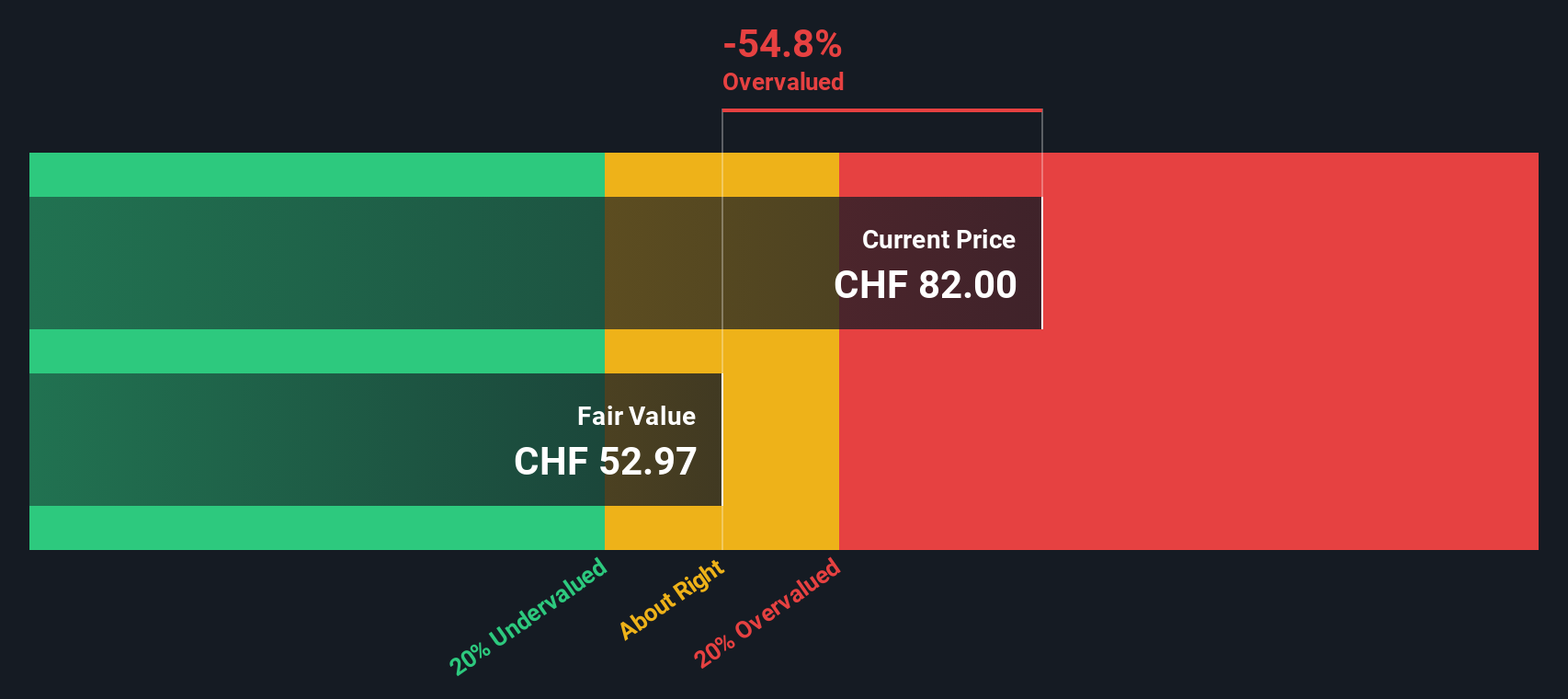

Another View: DCF Flags a Very Different Story

While the earnings multiple hints at reasonable value, our DCF model paints EPIC Suisse as clearly overvalued, with the CHF 83 share price sitting well above an estimated fair value of around CHF 53. That gap suggests less of a margin of safety than the P/E implies. Which signal do you trust when markets turn choppy?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out EPIC Suisse for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 908 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own EPIC Suisse Narrative

If you see the numbers differently or want to dig into the assumptions yourself, you can build a personalised view of EPIC Suisse in just a few minutes: Do it your way.

A great starting point for your EPIC Suisse research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next investment edge?

Capitalize on your momentum now, and use the Simply Wall St Screener to uncover focused opportunities that many investors overlook and position your portfolio ahead of the crowd.

- Capture potential mispricings by targeting these 908 undervalued stocks based on cash flows that the market has not fully appreciated yet.

- Harness structural growth trends with these 30 healthcare AI stocks transforming how medicine, diagnostics, and patient care evolve.

- Tap into the digital asset ecosystem through these 80 cryptocurrency and blockchain stocks riding long term adoption of blockchain infrastructure and applications.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if EPIC Suisse might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:EPIC

Second-rate dividend payer with questionable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)